The UK Property Market for the week ending Sunday 14th April 2024 (Week 15) saw the expected bounce back in listings and sales after the normal Easter slowdown

The UK Property Market for the week ending Sunday 14th April 2024 (Week 15) saw the expected bounce back in listings and sales after the normal Easter slowdown

In this week’s UK Property Market Stats Show with Steph Walker from TAUK, the headlines are as follows:

· House Prices on the 62k Sale Agreed homes in April stands at £344/sq.ft (March ’24 & Feb ’24 both at £339/sq.ft & Jan ’24 to £331/sq.ft)

· Listings for last week (Week 15) bounced back 24.3% from last week’s figure (because of Easter)

· Total Gross Sales YTD are 10.5% higher than 2023 YTD levels and 6.7% higher than 2017/18/19 levels. The best week for sales in the Uk since May 2023

· Net Sales last week 33.1% higher than Week 15 2023, and 13.4% higher the 2024 weekly average

· Sale fall-throughs still at just over 1 in 5 sales.

Chris’s In-Depth Analysis (Week 15) :

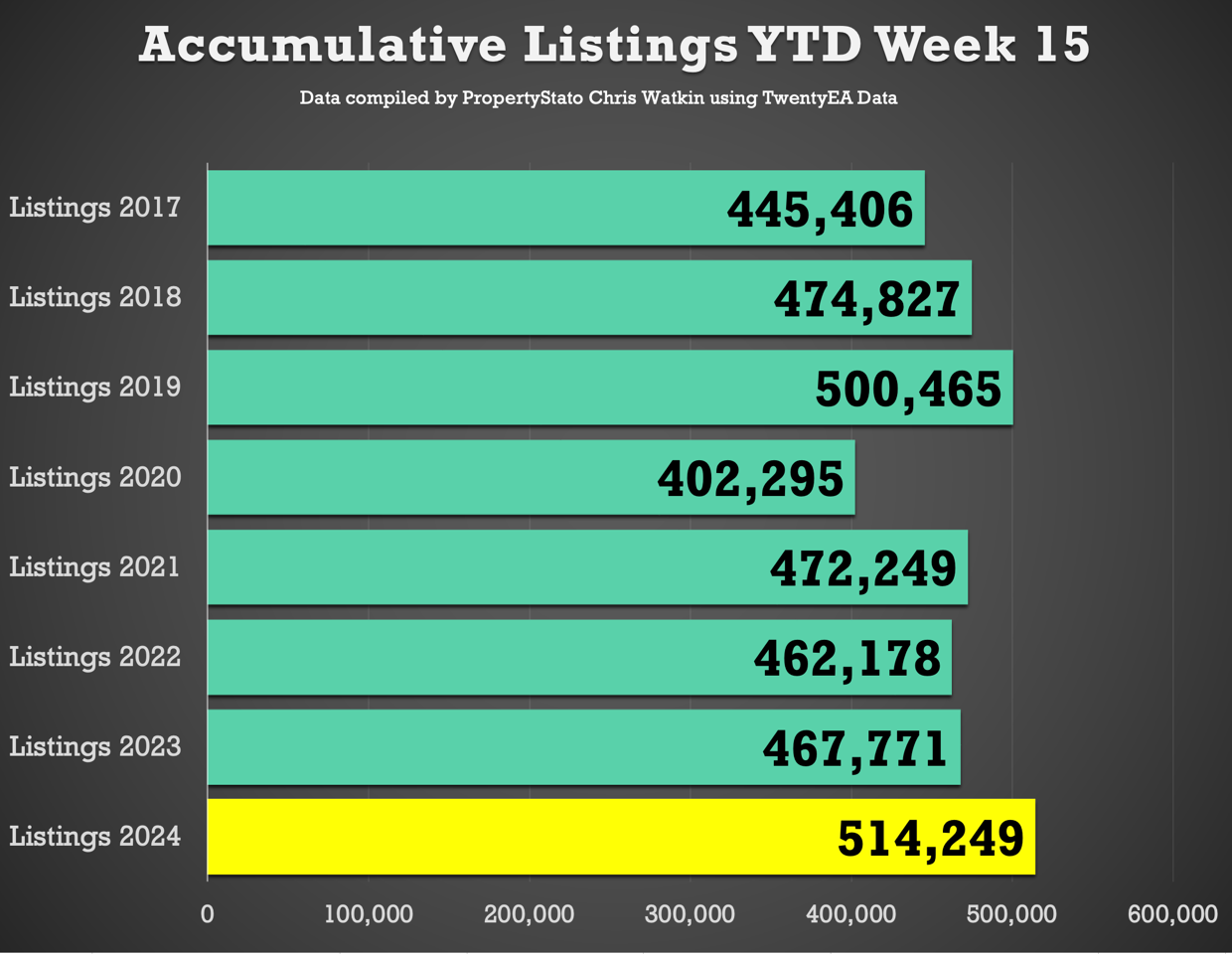

New Properties to Market: The UK saw 37,663 new listings. This year’s YTD listings stand at 514,249, 9.9% higher than the historical 8 year YTD average of 467,430 and 9.9% higher YTD 2023.

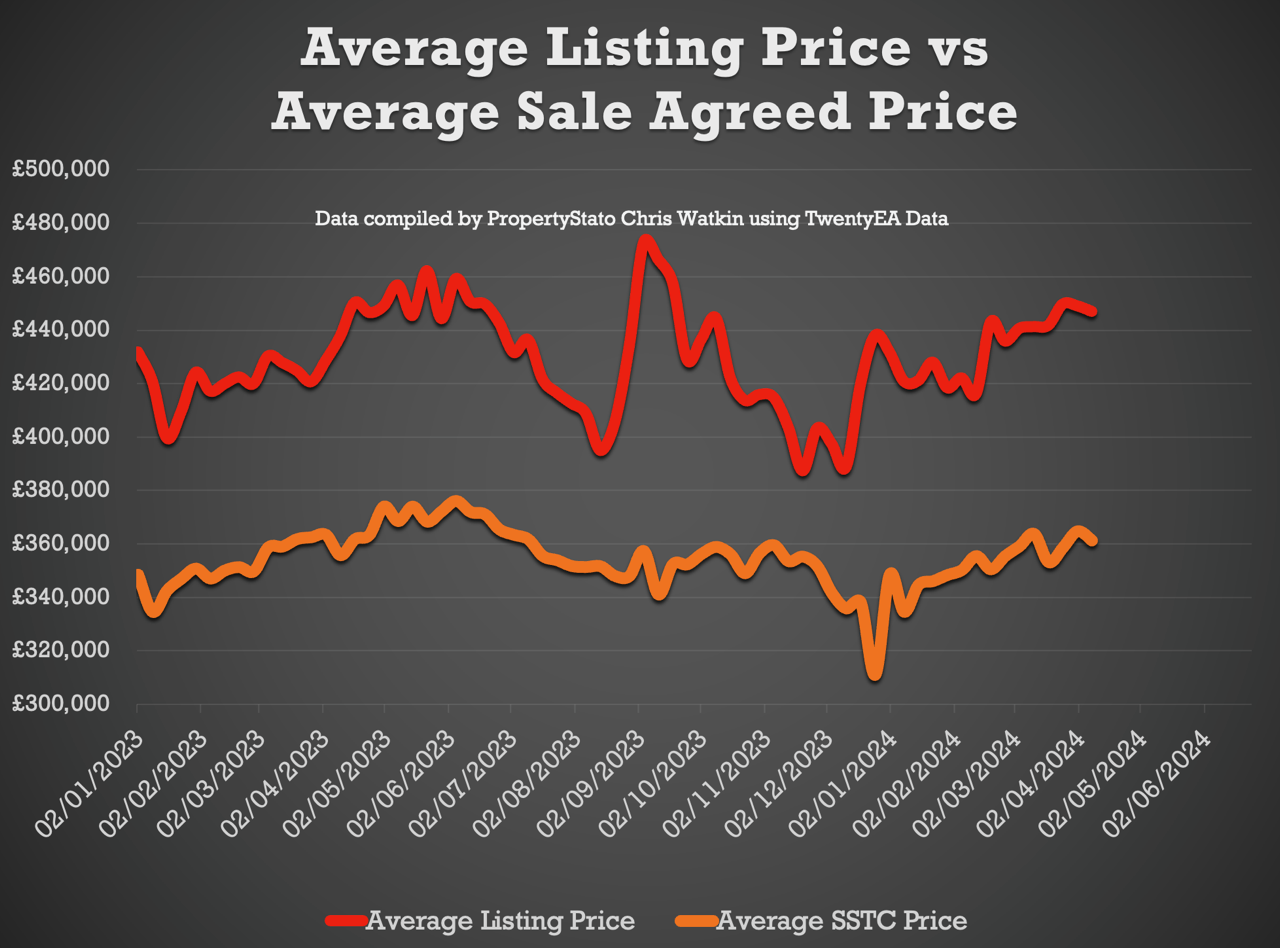

Average Listing Price: £446,989 .

Average Asking Price of this week’s Listings vs Average Asking Price of the Properties that Sale Agreed this week: 23.7%. The long-term average is between 16% and 17%. Over valuing in the whole of the UK, higher valuing properties for sale (downsizing) and a lower propensity of London & SE properties to sell causing this.

Price Reductions: Last week, 21,330 properties saw price reductions, a significant number compared to the 8-year Week 15 average of 12,352. This means 1 in 6.95 properties each month are being reduced (Long term average 1 in 9.9 per month)

Average Asking Price for Reduced Properties: £394,203.

Gross Sales: 26,529 properties were sold stc last week (a 24.9% increase from last week’s Gross Sales figures). Yet we had the Easter Weekend week before last.

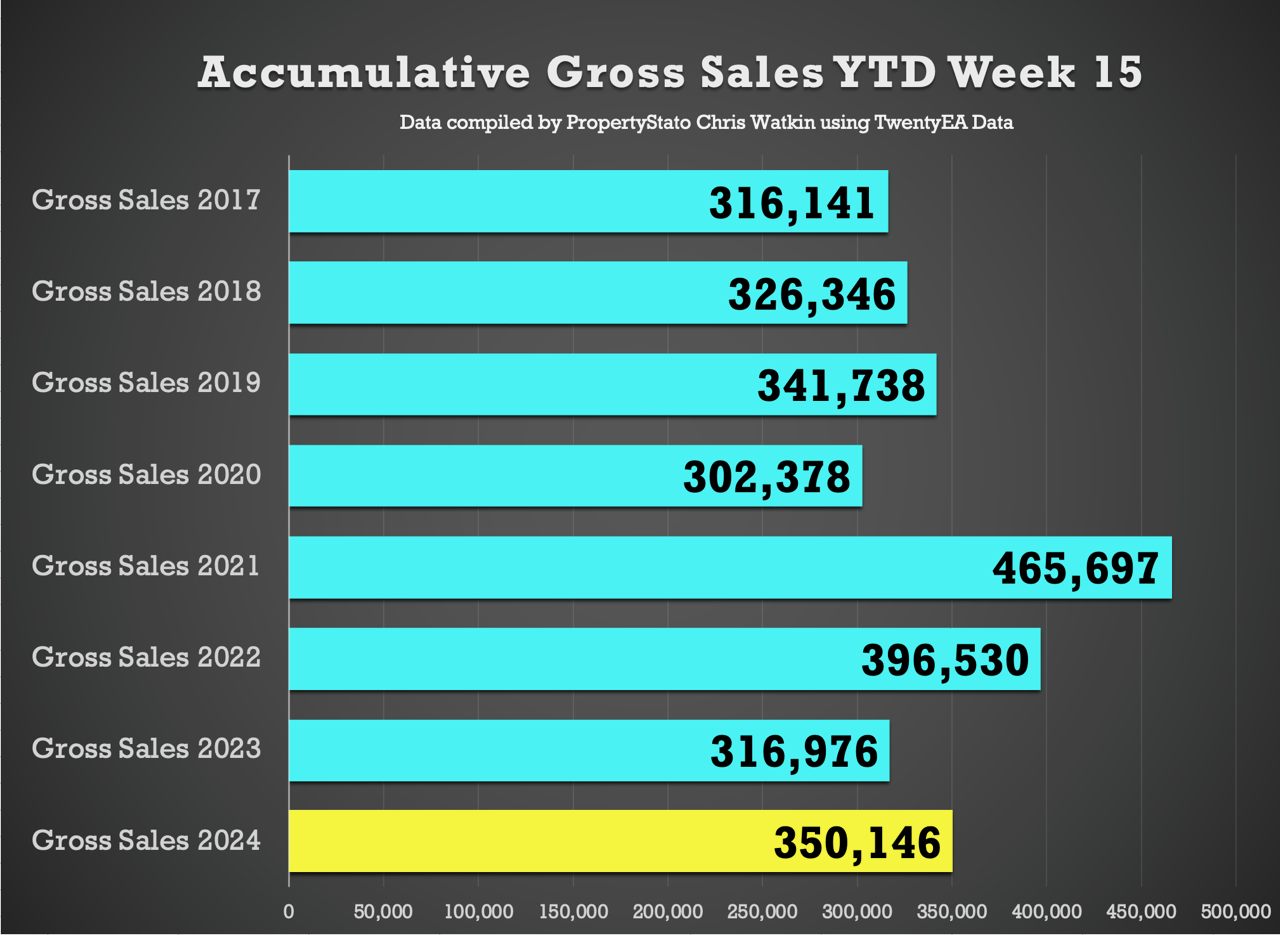

Accumulative Gross Sales YTD: The total stands at 350,146, exceeding the average of 328,075 from 17/18/19 and 316,976 in the same week 15 in 2023.

Average Asking Price of Sold STC Properties: Still staying in the £350k/£360k range at £361,211

Sale Fall Throughs: Slight increase this to 5,747 Always have a jump after the easter holidays). For comparison, 5,022 YTD ’24 average weekly figure & 7,590 weekly sale fall thrus in two months after Truss Budget in Q4 2022.

Sale Fall Through Rate: Decreased from last week, to 21.66% for the week (8 years average is 24.8%)

Net Sales increase from last week’s figure to 20,782. YTD ’24 average 18,322

Accumulative Net Sales YTD: The total stands at 274,823, 4% higher the 17/18/19 YTD Net sales average and 12.9% higher than the YTD figure for 2023 for Net Sales (2023 YTD : 243,441).

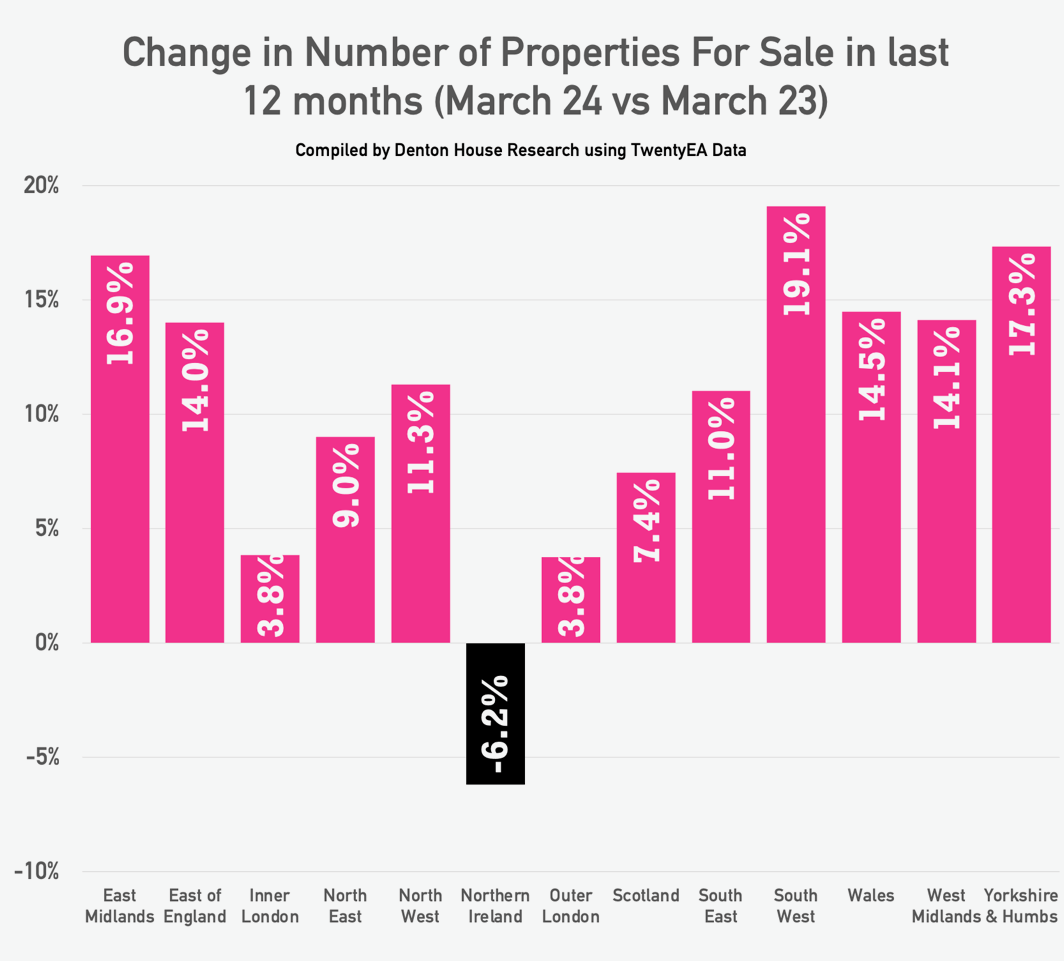

Change in Resi Sales Stock levels by Region

· East Midlands 16.9% Growth

· East of England 14.0% Growth

· Inner London 3.8% Growth

· North East 9.0% Growth

· North West 11.3% Growth

· Northern Ireland 6.2% DROP

· Outer London 3.8% Growth

· Scotland 7.4% Growth

· South East 11.0% Growth

· South West 19.1% Growth

· Wales 14.5% Growth

· West Midlands 14.1% Growth

· Yorkshire & Humbs 17.3% Growth

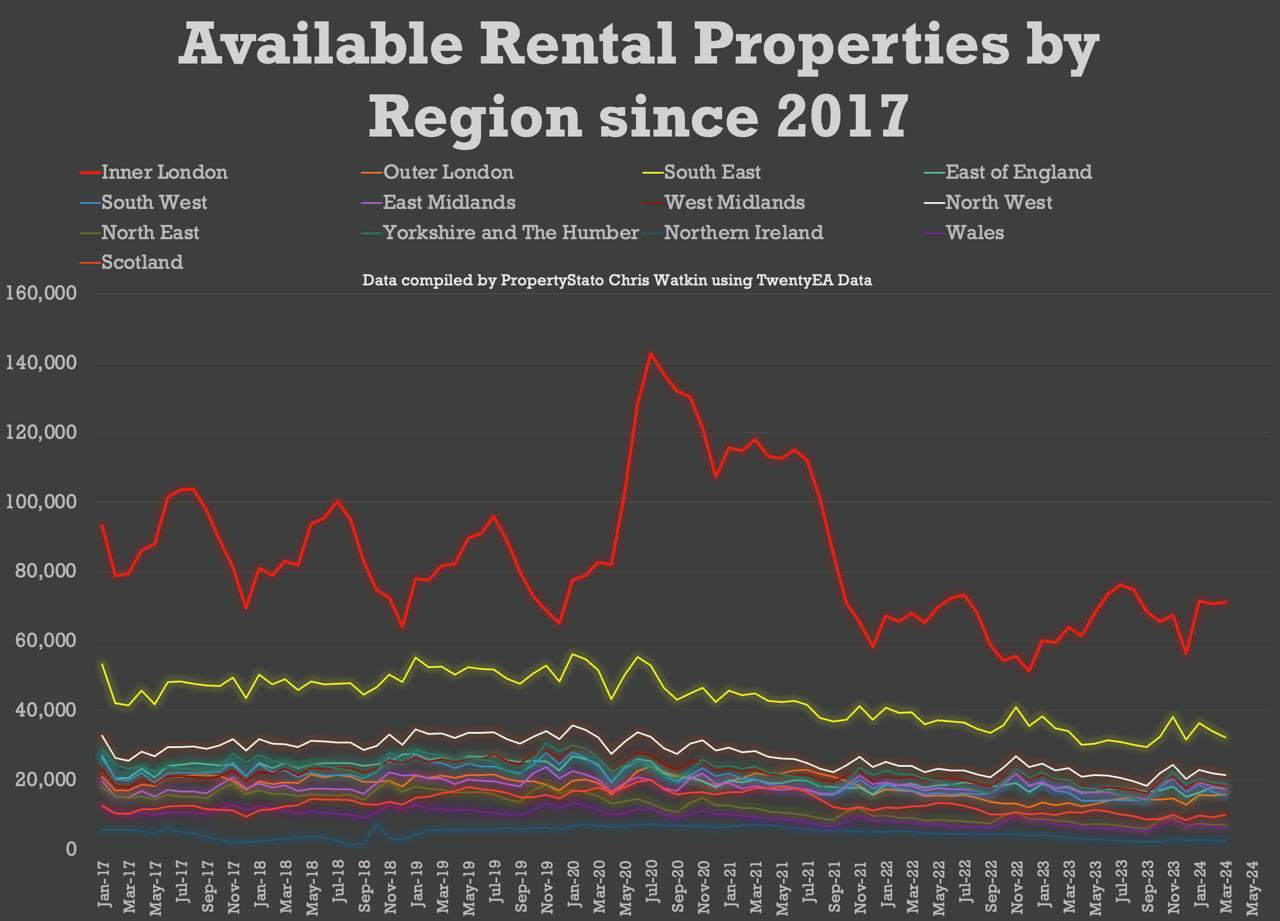

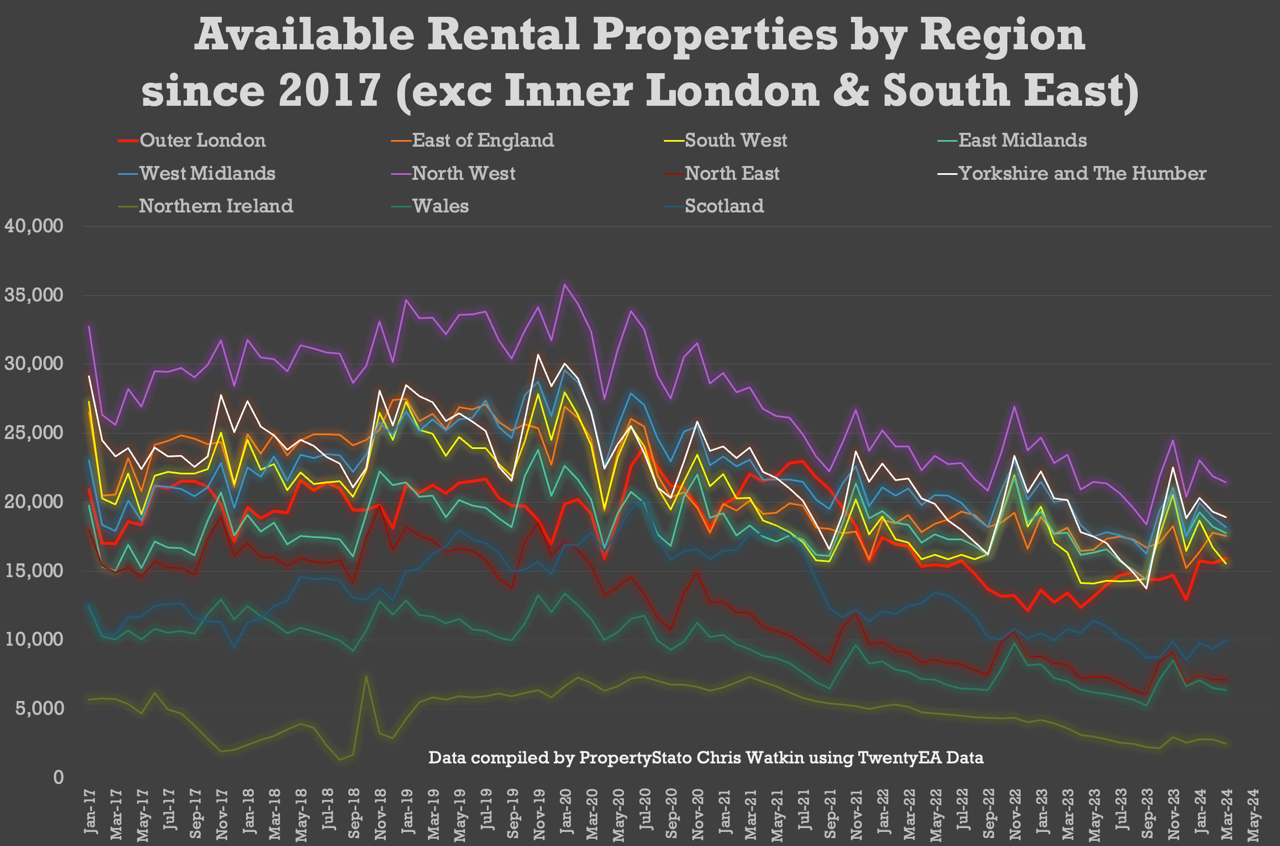

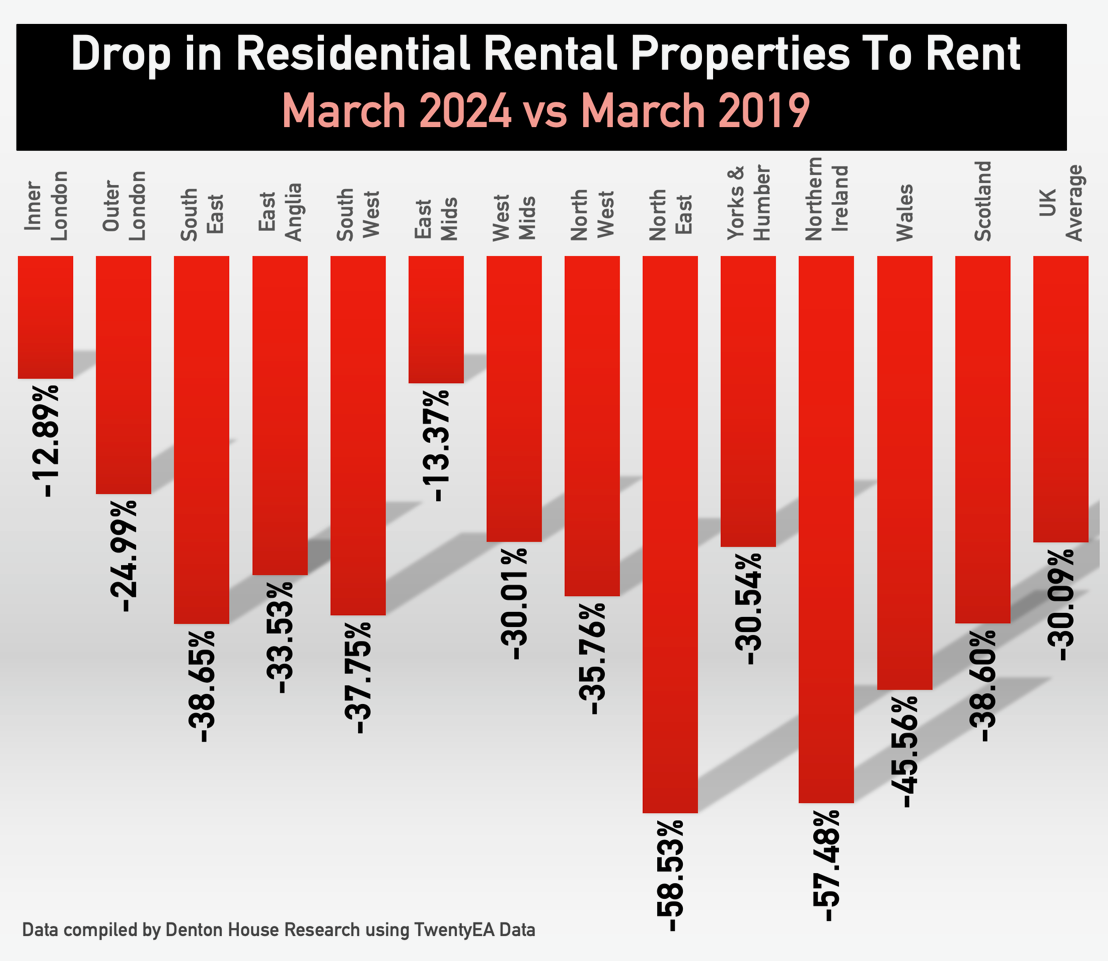

Change in Rental Stock coming on the market – March 2024 vs March 2019.

· Inner London -12.89%

· Outer London -24.99%

· South East -38.65%

· East Anglia -33.53%

· South West -37.75%

· East Mids -13.37%

· West Mids -30.01%

· North West -35.76%

· North East -58.53%

· Yorks & Humber -30.54%

· Northern Ireland -57.48%

· Wales -45.56%

· Scotland -38.60%

· UK Average -30.09%

This week’s local focus is on Sheffield

Comments (1)

We saw a dip in the property market in March – April and also contributed it to Eid al-Fitr, especially with our overseas enquiries. It is very interesting to hear that “Total Gross Sales YTD are 10.5% higher than 2023 YTD” that is quite impressive. Great resource, thanks for sharing.