The chancellor is said to be considering a number of tax hikes, including capital gains, and that has led to a significant rise in investors exiting the housing market.

Speculation is growing that the chancellor Rishi Sunak will announce changes to capital gains tax rates in the Budget next week, as he looks to find the money required to cover the government’s unprecedented spending and borrowing during the pandemic.

It comes as no surprise that the chancellor is reviewing the structure of UK taxes, with a senior financial analyst yesterday warning that a hike looks inevitable.

“For a Treasury that is looking to pinch some pennies, CGT looks like low hanging fruit,” said Laith Khalaf, financial analyst at AJ Bell.

The government’s tax adviser recently recommended that CGT be overhauled with proposals that could see the number of people hit by the duty increase sharply.

Rishi Sunak, who commissioned the review, is considering proposals by the Office of Tax Simplification (OTS), a Treasury-based body, to reform capital gains tax in the light of the economic and fiscal impact of the Covid-19 crisis.

The move has the potential to bring in an extra £14bn by reducing exemptions and doubling rates, according to the review.

Khalaf commented: “The chancellor asked the Office for Tax Simplification (OTS) to review Capital Gains Tax last year.

“The OTS duly obliged and recommended that CGT rates be raised in line with Income Tax rates, and that the £12,300 annual allowance of tax-free gains be cut to somewhere in the region of £2,000 to £4,000.”

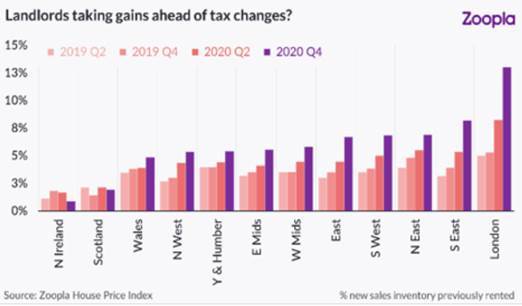

Since the government called for a review of capital gains tax last year, some investors are exiting the housing market, as the proportion of previously rented properties being listed for sale has risen.

The percentage of homes on the market that were previously for let has risen across all English regions, with 7.2% of all new sales inventory across the UK now previously rented, fresh data from Zoopla shows.

This trend is most prominent in London and the South East, with the proportion of previously rented properties now on the sales market standing at 13% and 8% respectively in these regions.

Some investors may be selling in order to beat changes to capital gains tax; or looking to take advantage of higher capital values; while others may be rationalising their portfolios due to changing rental market dynamics.

This goes some way to explain why the supply of property is rising in London, with a higher proportion – 13% – of new supply, made up of formerly rented property, now coming to the market, according to Gráinne Gilmore, head of research at Zoopla.

She commented: “One area of the market where there is more supply coming to the market is among landlords who are bringing their investment properties forward for sale.

“The share of homes listed for sale which were previously rented has risen in nearly every region during 2020, as landlords reassess their portfolios in light of current rental trends, or ahead of possible tax changes for investment property. While the homes for sale account for a very small proportion (less than 1%) of rented stock, it is a noticeable trend emerging in the market.”

Landlords will continue to exit the market due to this now and already onerous and costly regulations, plus legislation after legislation which appears to protect tenants first. Wait until this pandemic is over. The rate of properties let coming to the market for sale will rise again I expect to around 25%. Thousands of Landlords stuck while the government protects bad tenants from eviction who are desperate to sell.

This belief all Landlords are well off is a myth The weight of legislation against Landlords is just too much to bear and this impacts tenants through the back door with high rents in the private sector.

Well done the government and all you left wing lobby groups such as Shelter. *Applause

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Low interest rates have two unintended consequences for the government who for more years than I can recall have been trying to solve the housing crisis.

Low interest rates inflate asset prices not just property, all assets increase in value in line with increased affordability. That makes the capital growth on property consistent and secure. The income yield from property is strong too because a shortage of supply ensures rents a re high too- that is triple bubble advantage for property investment capital growth, secure investment and good income yield.

Because interest rates are low cash in the bank is worthless and annuities are not much better and as personal pensions are less accessible than a nun’s knickers anyone who can is getting hold of or keeping hold of property as an investment, whether to AST or short lets.

With too many people investing in property and too many estates not releasing properties back to the market there has been a consistent contraction of sales that averages about -2% each year.

Through S24 and threats of CGT there is an attempt to discourage small investors from having property, it reduces properties coming to the market and investment cash is better off in property than pensions and annuities.

If properties have no gain there can’t be a tax liability, so this is one of the most easily avoided proposals there is, properties will simply be sold between generations at nill capital gain.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I agree with everything you say Robert except the ‘selling of properties between generations at no gain’. It rarely happens, can not happen after ownership death due to probate laws and MOST people would not be able to lose the income by selling the property (we are talking small private landlords here.)

A greater supply of property would do all levels of society a favour, that may well happen in the next couple of years, but not for the reasons that get discussed on this forum.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I’m not talking about waiting for probate for the portfolio transfer. There comes a point where the lucky folk have enough and start staring down the barrels of 40% tax on assets paid for out of taxed income. There’s a choice of spending or finding a way of passing it on.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

A mass exodus is unlikely to happen in my opinion. However, if it did happen, this would lead to increase in supply of properties, a reduction in value bringing more buyers and particularly first time buyers into the market. I believe George Osbourne was trying to bring the property market to a ‘soft landing’ with the tax changes he made, leveling up the market a little for first time buyers and that is no bad thing. The current stamp duty holiday has just fueled a market bubble which could make life even harder for landlords looking to exit in the future!

I am a landlord and letting agent myself, but it does not seem unreasonable that a landlord does have higher costs over a residential buyer, to reflect the advantages that they have.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I don’t buy into the “max exodus” that’s been bandied around by doom mongers for as long as I can remember. The same people have been forecasting a mass exodus for 15 years, during which tine the BTL market has operated quite effectively for both landlords and tenants.

Some landlords will of course feel the pressure of tougher regulation or higher costs but don’t be fooled, landlords are a resilient and adaptable bunch. I’m an agent and landlord.

Landlords have been buying in the last few months to benefit from the SDLT holiday and fewer have been exiting due to the onerous possession rules as a result of COVID.

I don’t think anyone would argue that there’s a possibility some landlords will sell when possession rules return to “normal” but it’s market driven and as some exit the market others will enter the market.

I’ve seen investors return to my area in the last year. Higher rents mean higher returns.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Depends where you are. Let me assure you where I am in a London suburb rents have reached the too, healthy yields are no longer available especially when you factor in escalating service charges, ground rents and agents fees.

Many Landlords in the SE hanging on by their finger nails and we’re certainly not seeing new investment in the BTL market.

The benefits of being a Landlord are minimal. No rewards for assisting the governments issue of housing demand.

Total chaos is coming and it’s the lower classes that will suffer as a result when legislation was introduced to supposedly assist these types of groups.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Fair point about parts of London as I fully understand that yields vary from area to area, but I don’t buy into the total chaos theory.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Lets reconvene a couple of months after all the government support has been removed. If only we had a crystal ball eh? 😉

Thanks for engaging AAA and have a good day

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Good idea! Thank you my friend and as long as we have plenty of business we’ll both be secretly happy!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

You seem to have a crystal ball?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

If they do not want to remsain a LL they can sell.

They are not skilled people they just rent a flat.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

At the risk of being controversial, I disagreed with the temporary reduction in Stamp Duty. It was unnecessary and always going to create a burst of activity which wasn’t needed.

‘We’d all like to go away to somewhere warm for a week in the winter, but Everyone has to face the reality of returning to the status quo.’

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I could not agree more. We had a £500,000 transaction which was going to go through whether stamp duty was relaxed or not. The buyers made a massive saving and the government is going to have to make that money up from somewhere else. Do not be afraid of a falling value house market. If it happens the world does not have the benefit of reducing interest rates, so there will probably be more repossessions than 10 years ago. Forced sales will mean an active market.

I am not saying I want this, but I can see it happening.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register