![]() When the Chancellor announced in July last year that he would offer homebuyers savings of up to £15,000 by cutting the stamp duty payable the first £500,000 of any purchase for a year, it acted as a boost to the market.

When the Chancellor announced in July last year that he would offer homebuyers savings of up to £15,000 by cutting the stamp duty payable the first £500,000 of any purchase for a year, it acted as a boost to the market.

Buyer demand had already started building as a result of pent-up demand during the first lockdown. But sustained higher levels of buyer demand after the initial re-opening of the market in May last year indicated there was a more fundamental ‘reassessment of home’ happening after many households were confined indoors. Movers were looking for homes with more space, inside and outside, with increased levels of activity in rural and coastal areas.

The chancellor’s announcement in July underpinned this demand.

As the chart below shows, buyer demand reached a peak in April this year – the date at which buyers had to commit if they stood a chance of completing a sale before June 30th, when the main stamp duty holiday ended.

After this point, demand levels fell, indicating that the stamp duty savings of up to £15,000 had been a key driver in that very busy market. Those who missed the deadline could console themselves with savings of up to £2,500 on their purchase, under the Chancellor’s ‘tapered’ stamp duty holiday which ran to the end of September.

There are two key factors to consider when looking at buyer trends after the end of June however. The first is that even though demand moderated, the new level it reached was still above average levels for the time of year.

The second is that demand could have moderated further after the end of June, as this was the latest date when buyers would have had to agree a purchase in order to complete by the end of September, and take advantage of the tapered holiday.

However, as the crunch date passed, demand remained largely steady. At the end of September, demand is still running 35% ahead of the five-year average.

So when it comes to answering whether the stamp duty holiday has impacted demand, the answer is ‘yes and no’.

Was it a driver for the market over the last 18 months? Undoubtedly.

But there are other factors at play too. The ‘search for space’ and ‘reassessment of home’ have further to run, especially as office-based workers receive confirmation from their employers about the level of flexibility with which they will be able to work, opening the way for more households to move further from the office.

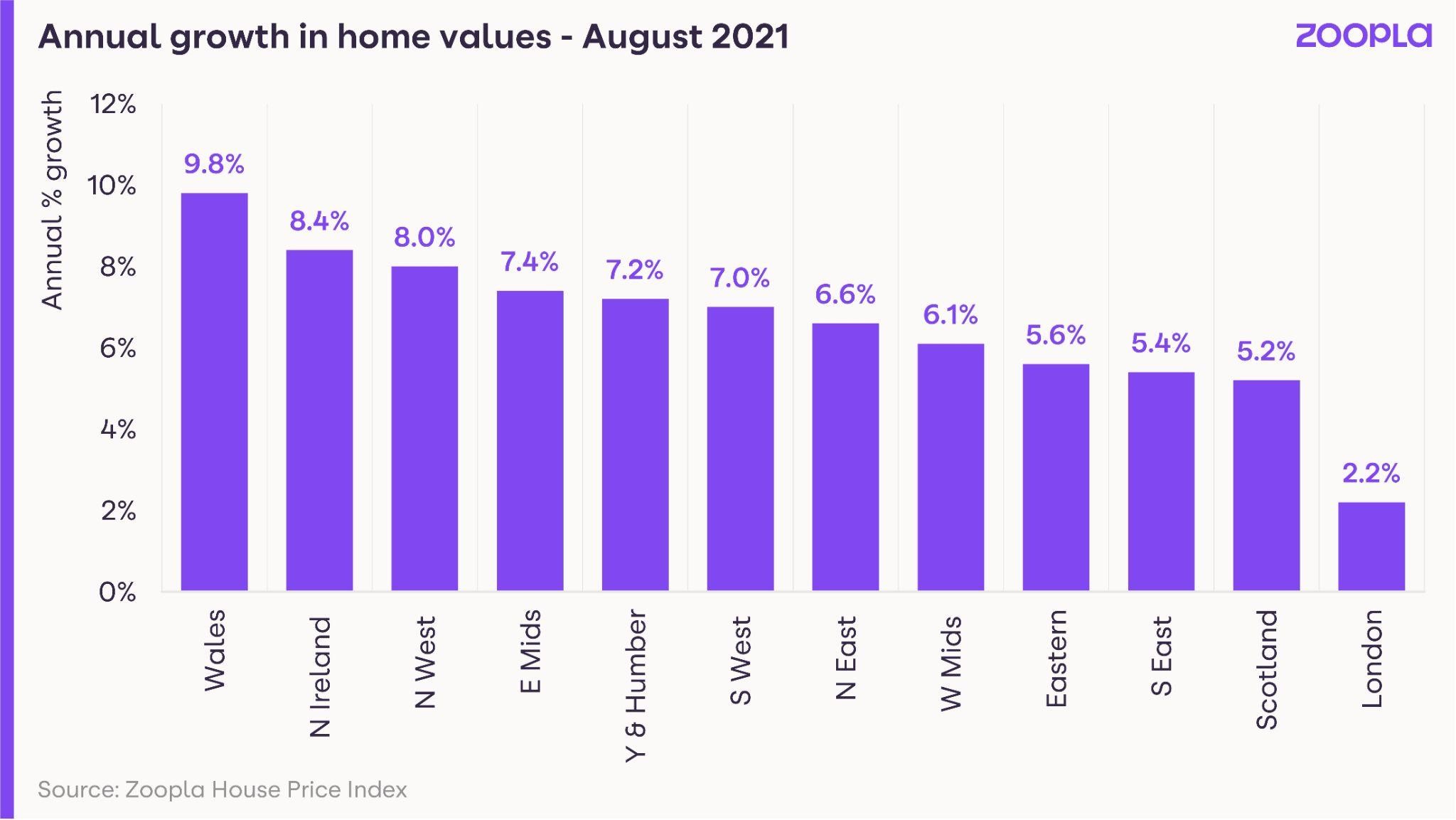

This increased demand will continue to underpin price growth, which is running highest in the most affordable areas of the country.

Amid higher demand, supply is still nearly 30% in the year to date compared to 2020 levels, which will continue to put upwards pressure on pricing. However, as we move into Q4, and a more challenging economic landscape, the level of growth will start to moderate, although price growth will still be firmly in positive territory by December.

Gráinne Gilmore is head of research at Zoopla.

The usual quality commentary from Zoopla. Gilmore points out that the SDLT holiday is only one factor that has increased demand and with demand in September being 35% ahead of the 5 year average.

Stock issues aside, unusually high demand and low mortgage rates means we are going to have another year of balancing low stock against high demand which is not great news for online-only agents or bottom feeders.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register