This time last year, I kicked off my forecast for the 2021 market by proclaiming that, in the prevailing conditions, “prophesy is a mug’s game”. The Big Names went on to prove the point, as Savills, Knight Frank, Rightmove, Zoopla, et al, scrambled their way through the year increasing the numbers as they went.

For my part, I dodged the bullet by setting out three possible outcomes for the year, dependent on how the pandemic might play out. I am relieved to report, my ‘Option 3’ was on the money, suggesting that if there was a successful vaccine roll-out and the ‘R rate’ (remember that?) fell, then the market would flourish and the year would end up around 10% ahead of 2020. (That forecast is still up there as a matter of record if you want to check on me… https://afoliver.agency/insights/the-residential-market-in-2021/ )

You might argue it was a cop out to offer three possible outcomes, but I disagree, I think it was the only responsible strategy. It was impossible to predict last year’s market with any certainty because none of us knew where the pandemic was headed. If the vaccines hadn’t broken the link between infections and deaths, you can be sure things would look very different right now. And some of those organisations whose critical mass and share of voice are sometimes powerful enough to deliver self-fulfilling prophesies, should have known better than to confidently set out detailed predictions – without the odd caveat at least.

While there are still lots of unanswered questions about Covid, the latest variant appears to be less severe than its predecessors, and we do have a much better idea of how the home-buying public have tended to react to the challenges and the consequences of programmes like the furlough scheme and the ‘working from home’ initiative. The Stamp Duty holiday has come and gone, leaving many of us breathless in its wake. Help To Buy is in its final iteration before it disappears altogether in 2023 and furlough has finished without the predicted surge in unemployment.

So, we have a slightly more settled backdrop against which to consider where the market is headed next year. Notwithstanding that, the forecast I set out below is based on us being able to manage Omicron and no new variants emerging.

While we are not walking into the teeth of a storm as we enter the new year, there are undoubtedly headwinds. Last week, the Bank of England announced a 0.15% increase in interest rates. Hardly a titanic rise, but we all know how upward pressure on rates affects Consumer Confidence, and, sure as night follows day, the market. It was interesting to see the Bank of England’s figures for interest rates in November (see the chart below). They were published before the rate rise, and you can see that on fixed rates up to five years, for a typical 75% LTV mortgage, there was a substantial jump. This is one to watch, both for the next steps and consumer reaction.

Source: Bank of England

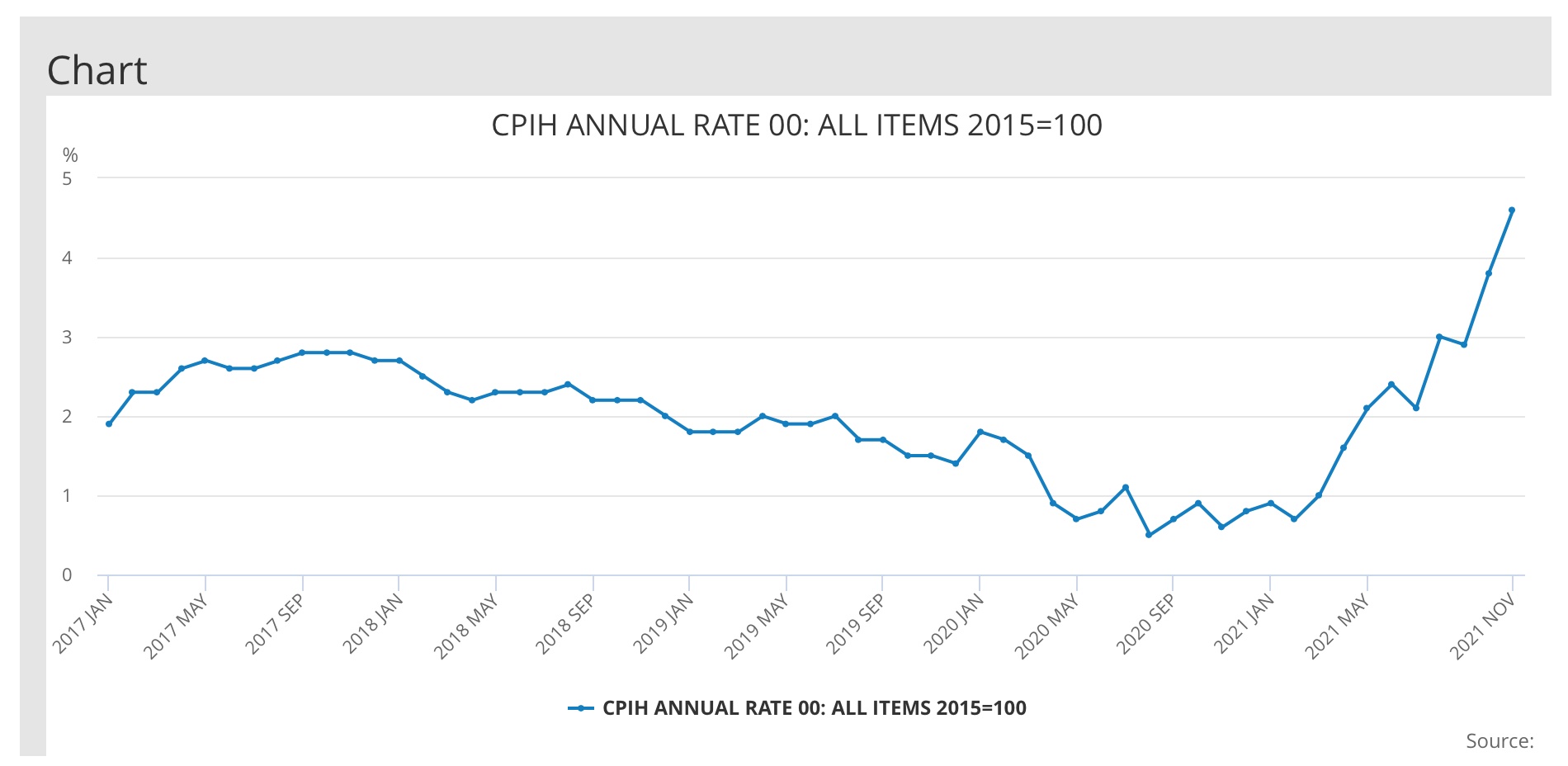

To be honest, interest rates are not the biggest financial factors that are bothering me. Interest rates are still at historic lows and seem certain to stay that way for quite a while yet. But last week the Government published the November inflation figures, and they were a shock to the system. The Consumer Price Index (CPI), the preferred measure, touched 5.1%, its highest for over ten years. Admittedly, the index including owner occupiers’ housing costs (CPIH) was lower at 4.6%, (see the chart below) but that number would have sent shock waves through the treasury and they will undoubtedly be considering measures they might take to rein it in. It is also worth noting the Retail Price Index (RPI) came in at over 7%!

Source: ONS

Raising interest rates does influence the market, undoubtedly, but nothing like a shortage in the availability of mortgages. If the chancellor starts to put pressure on lenders to strengthen their lending criteria (having only just relaxed them last month) or simply to reduce the products on offer, then that really will impact the market. To paraphrase “Shoeless” Joe Jackson in Field of Dreams; “If you lend it, they will borrow.” And the opposite is equally true; if buyers can’t get a mortgage, they’re not buyers anymore. Inflation matters, and fast-rising inflation is a genuine worry and a headwind we need to be aware of.

Regardless of the concerns about interest rates and the availability of mortgages, there is still a whole raft of factors underpinning the market. In my last market report, I listed the key factors behind the unexpected boom of 2020/2021 as; low mortgage rates, Stamp Duty incentives, high consumer confidence, lifestyle changes and demand exceeding supply. Many of these still apply. The drivers behind the demands of homebuyers in the ‘work from home’ era for example, buyers still want more space, a garden, an office, good wi-fi, etc.

We are still seeing property sold in an average of under 40 days on Rightmove and Zoopla (although this is creeping up), asking prices are still being achieved in many cases (although not quite so many) and you still need to be the agent’s best mate to have a chance when something exceptional comes on the market.

Another potential spanner in the works is the desperate shortage of stock on the market.

In most consumer markets, supply and demand is a simple mechanic. The more people that want something that is in short supply, the more they’ll pay. The shorter the supply, the higher the price. But property only works like that up to a point, and then there is a danger of market stasis creeping in. When purchasers look at the meagre number of available properties and say to themselves, “there’s nothing decent to choose from, and what there is, is so expensive”, it becomes easy for them to say, “do you know what, I think we’ll leave it for now until there’s a better choice”. If enough buyers do that, the market stalls, and that can be disastrous.

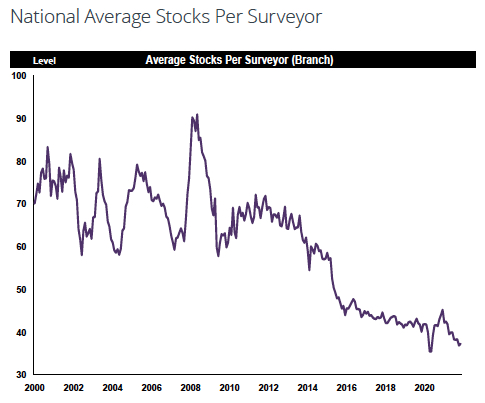

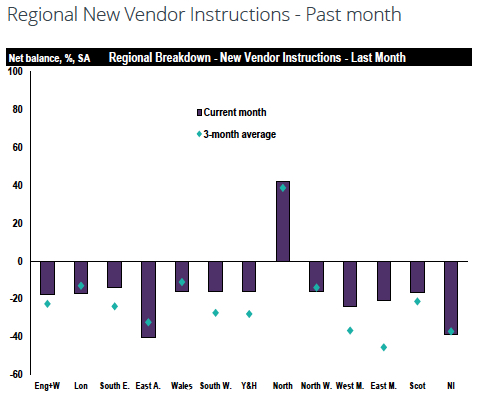

Look at the RICS chart on the left below showing current agents’ average stocks across the UK, it’s frightening. Next to it is what I consider one of my ‘canary’ charts, a real bellwether for short-term market movements, New Vendor Instructions, the source of new stock to invigorate the market. The charts tell their own story.

Source: RICS

Let’s hope that January sees the traditional influx of new instructions from people who have set one of their New Year’s resolutions as moving home. If it doesn’t, then the shortage of stock remains a major threat to the market. In these conditions, new homes developers need to manage their portfolios carefully. It’s the perfect time to offer prospects the chance to genuinely benefit by engaging early and giving them first dibs when properties are released. It can lead to great customer relations and long-term loyalty.

On the basis that we don’t see a complete drying up of stock and lenders stay lending, then we have enough underlying factors in play to see positive inflation stay with us throughout the whole of 2022. Not to the same level that we saw in 2021, but that’s not necessarily a bad thing. Double-digit inflation is unsustainable over the mid-term and it does nobody any good. Not buyers – nor sellers, unless they’re selling up and going round the world on a boat, not the bankers nor the builders, and certainly not the Government. There are too many powerful vested interests ranged against seeing that state of affairs endure for too long and I’m convinced that we’re at the top, or close to the top, of this current boom.

Those positive underlying factors I mentioned make it highly unlikely we’ll see a ‘cliff-edge’ transition from this over-heated market to one more in line with expectations; it’ll be more a gentle slope in the reduction in the rate of inflation. The first quarter of the new year will be a very important one. If we see the hoped-for sharp increase in new instructions for the agents early in the year, then we may well go through the winter season with prices barely moving. In that case, I forecast inflation will still be running at over 7.5% as we move into April.

The spring quarter will be more difficult to call. There are so many things that might have happened by then, any of which would have its own effect. But I still believe the Government’s desire to support the economy in its fight to recover from Covid will have beneficial effects for the property market too. And, on that basis, while I think we will see the market move back as it moves from spring into summer, it won’t be by much. I forecast UK inflation, according to the Nationwide Index, to be between 6% and 6.5% at the half year.

As I always say at this point in my annual forecasts, I reserve the right to reforecast at the half-year, so much could have changed. However, if the main factors in play remain broadly similar in terms of their extent and effect, then I anticipate a further slight softening in H2. I forecast ending the year with positive inflation running at between 4.5% and 5.5%.

And what about volumes?

The number of UK transactions, with a value over £40K as measured by the HMRC, took everyone by surprise this year, including me; until I updated my forecast at the half-year, in any case. We won’t see the confirmed November numbers for a while yet, but all the signs are that we’ll end up with around 1.5m for the 12 months to December 2021. The highest 12 months total since 2007. The Stamp Duty holiday, with all its extensions and taper, played havoc with the normal patterns of transactions in the year (see the chart below).

Source: HMRC

People hate paying Stamp Duty, and the opportunity to avoid it was a massive incentive for people to rush through transactions, forestalling the tax, even though the creation of that ‘rush’ led to price increases greater than the savings they would make on the Stamp Duty. It does appear however, that things have returned to normal, or at least, close to it, now those deals have fed through the system. In the years up to 2020 the market had been its most stable state in living memory. Give or take the odd thousand here and there, we’ve been running at 1.2m transactions per annum since 2014. It became the easiest possible statistic to forecast.

The post-lockdown reaction, the tax savings, the new lifestyle choices, working from home, moving out of – and subsequently back into – London; all these things added to the rise and rise of volumes through the year. So, where will it go next year?

I still think there will be enough of these factors in play to maintain volumes above the ‘new normal’ of the last six or seven years. I believe we’ll see around 1.3m to 1.35m transactions in the 2022 calendar year.

As far as new build is concerned, developers face a raft of other issues as we head into the new year – materials costs and shortages, skills shortages, planning delays, etc. etc. However, I still believe the momentum created by the comeback after lockdown, and the opportunities provided by the changing market and low availability, will be the wind in their sails, particularly for the smarter and more agile amongst them. I believe their market share in 2022 will be well above the long-run average at around 12% – depending on which measure you use!

So, there you have it. After an extraordinary year, one where the country’s estate agents went from distraught to euphoric in the space of a few months, we are moving back to the more prosaic and predictable market of the pre-pandemic years – provided Covid, Brexit, inflation, et al don’t play a part, of course. ‘From the sublime to the slightly worrying’ you could say.

Matt Fleming is executive chairman at AF OLIVER, advising housebuilders throughout the UK.

For the next 3-4 months it will be much much quieter – a blessing for conveyancers – and then it will start to rise, but nowhere near the last 2 years and not quite back to ‘normal’. I’m usually spot on with my predictions, but we shall see.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

A measured and well researched article, thank you

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register