The house price growth seen over the last 12 months (UK prices are up +6.0% on the year), in the teeth of the pandemic, has largely been due to the imbalance between higher levels of buyer demand and a more limited supply of homes for sale.

The rise in buyer demand was evident from last April, and was boosted further by the stamp duty holiday. Ultra-low mortgage rates have also played a part in making home ownership more affordable for those who have access to a deposit or who have higher levels of equity.

But with many homeowners making a move, why has there been so much pressure on the stock of homes for sale? And when will stock levels start to repair?

This is something we have examined in detail in our latest House Price Index report .

To put the issue in context, the number of homes being listed for sale, or ‘new supply’, is around 5% down on typical levels, and this has been the case since the start of the year.

Even if the flow of new homes being listed for sale was back up at usual levels, this would not be enough to replenish the total stock of homes for sale, which is down 26% compared to last year.

If we look further back for comparisons, to check against more ‘normal’ market conditions, total stock is down 25% compared to 2016 and 2017, and 33% below levels seen in the slightly slower markets of 2018 and 2019. All in all – stock levels are running below levels usually seen during quiet Christmas periods.

There are several factors feeding into the lower levels of stock.

The first is the level of activity in the market. Completed sales jumped by 25% in the 12 months to June, compared to the same period in 2019, according to HMRC data. The number of sales has fallen back in July, but even so, it means 1 in 20 homes changed hands over the last year, compared to one in 25 in 2019.

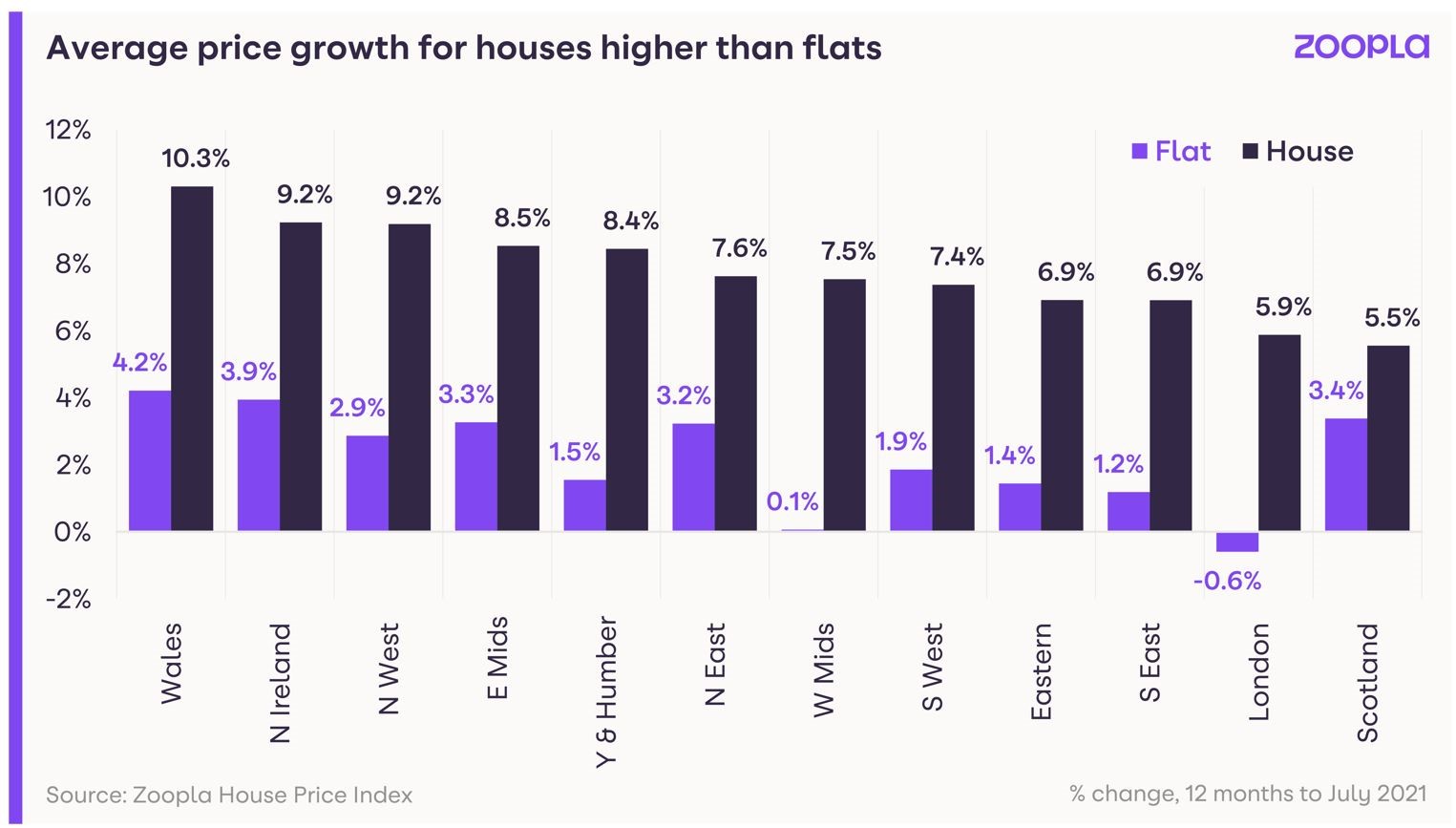

The ‘search for space’ among buyers put the focus on larger family houses, and this type of stock has become particularly stretched, reflected in price movements: the average price for a house has risen 7.6% over the last 12 months. The supply squeeze for flats is more muted, and price growth for this type of home is up 1.2% on the year.

Another reason for the supply squeeze is the increased levels of activity among first-time buyers and investors – buyers that represent net new demand, as the majority have no property to sell.

First-time buyers (FTBs) account for around a third of all buyers, and they have been increasingly active in 2021, with demand up 15% compared to 2020, according to Zoopla data. This increased activity comes as lenders, have reversed tighter criteria imposed during the outbreak of the pandemic during 2020, and supported more FTBs into the market. The activity seen so far this year is likely to be a continued release pent-up demand from 2020, and so levels of activity will begin to return to more normal levels as we move through the rest of 2021.

Investors were also able to take advantage of the lower purchase tax charges as a result of the stamp duty holiday, resulting in a 21% rise in demand among this buyer group compared to 2020. Strong demand for rental properties is likely to be a continued draw for investors, even as tax changes have caused some landlords to review their portfolios. However, the ending of the stamp duty holiday will likely impact investor demand.

Another factor worth consideration is the slowdown in the supply of new homes over the last 12 months, due to the shut-down of the construction industry last year during the first lockdown. New homes completions fell by 11% in England in the year to March. While supply has already started to pick up again, this dip will have had an impact on the total number of homes available to buy. Another factor here is the small, but increasing, number of homes which are going directly to the rental market, without hitting the sales market first.

The post-pandemic ‘search for space’ has further to run, especially as businesses confirm working practices, with more flexible working in many cases allowing more scope to live further from the office. However, the lack of supply – particularly for family houses, means the market will start to naturally slow during the rest of this year and into next year.

While we forecast a strong start to 2022, in line with seasonal trends, a return to more usual levels of activity among first-time buyers, the ending of the stamp duty holiday, and some potential movers waiting for more stock to become available before making a move, will result in a slow repairing of stock levels through H1.

Gráinne Gilmore is head of research at Zoopla.

A helpful and informative article from the numbers crunchers at ZPG. “We forecast a strong start to 2022 and a return to more usual levels of activity among first time buyers ..”

That should silence some of the doom-mongers who have been shouting “crash, crash” for most of this year.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

25 / 33% More like 55 / 65% down in North Yorkshire.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Good luck to Grainne assimilating her research from the data appearing on ZPL.

Yesterday appeared on ZPL a property from Purplebricks identifying as FRESHLY LISTED

2 bed terrace Stanhope Road Northampton NN2 £200k.

Not only that arrives Sold STC

Impressive work by Bricks.?Oveheated market?

Not quite according to RM Bricks had listed the property on the 15th June

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

65% to 75% down in my area… seriously nada coming on. (Valuation this morning and another one where I am saying Zero available stock in a 200k price range with 3 to 5 bedrooms included – Scary)

and I think Easter 2022 before any return to more normal level of new instructions… but still then, the Pandemic may just have changed the moving cycle to longer stays between moves.

This is quite possible the most testing market now and ahead (Having stock you can’t sell always has a solution, whereas making people move, ain’t that easy)

The pressure on increasing fees to make up for lack of stock and making sure you are working smart with which service providers you NEED to give money to is now key for many I think. Q1 and Q2 of 2022 may be a tad awkward for some.

But surely this is the property markets way of giving EAs the LAST CHANCE to take back some control over the way we sell property. This last chance has given us the unique scenario in a digital age where buyers are bypassing the national portals to plead with EAs to let them know first about the next new house…

The supermarket shelves are empty and what we have suspected for years is happening, as buyers turn to the corner shops in the hunt for stock… WE as distributors to the supermarket, should be seriously considering it being time to ask the supermarkets to pay us for delivering what they need to survive! OR better still just feed the corner shops. (Sorry **** analogy haha)

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I think you are right, people are now more likely to stay put longer.

It was a great shot in the arm stamp duty holiday but it has effectively broken the market.

Less properties to sell will be the norm, agents will have to charge more to survive, this will probably co-inside with a regulated industry and the removal of a number of firms.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Here’s one for you – I both agree and disagree with you, SP!

People are taking more time between moves than they were – there is no doubt about that. Back in the day – and not really THAT long ago, but many of today’s Agents will not have worked in the market – youngsters were encouraged to buy a doer-upper to get a foot on the ladder. They would then trade up (maybe take on another, larger house in need of some TLC)… and up… to the point that they were able to buy what they thought would be their “forever home”. Now – ironically when factors and logic indicate it should be the other way round – the kids want a shiny brand-new mansionette… and moan that they can’t afford one (and that’s all the fault of my – and your – generations!). In that respect, the market isn’t broken – it’s the people that need fixing.

With regard to your point “Less properties to sell will be the norm” – this is where I feel I have to disagree. Properties need to be sold at some point. A “forever home” is less likely now than it ever was, for which I would suggest a number of factors will dictate throughout a homeowner’s lifespan. There are also more properties, and that will continue. They can’t all be bought by investors and second-homers, so the cycle will continue. Numbers, I believe will increase – but it will take many months for the numbers to approach those of what are considered ‘the norm’.

Unless, that is, something is around the corner that you, I, nor the Zoopla soothsayers can see…

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register