UK Finance has today published its housing and mortgage market forecasts for 2024 and 2025 together with projections for 2023 full year numbers.

UK Finance has today published its housing and mortgage market forecasts for 2024 and 2025 together with projections for 2023 full year numbers.

Key figures for 2023

In 2023, higher interest rates and household costs limited access to mortgage credit. Affordability constraints have also dampened external remortgaging activity, although there was growth in the internal product transfer market, where affordability tests are not required.

Cost of living and interest rate pressures also pushed more customers into arrears, which were up on the historically low number in 2022, although the total represents only around one per cent of total outstanding mortgages in the UK.

| 2023 | Year on year change | |

| Gross Lending | £226 billion | -28% |

| Lending for house purchase | £130 billion | -23% |

| External remortgaging | £65 billion | -21% |

| Internal product transfer | £219 billion | +11% |

| New buy to let purchase lending | £8 billion | -53% |

| Arrears | 105,600 | +30% |

| Possessions | 4,400 | +13% |

2024 forecast figures

The outlook for 2024 is one of continuing challenges in the mortgage market; however, the main pressures on affordability look to be peaking now. Whilst it will take some time for the pressure on household finances to recede, we expect things to begin to look up in 2025. Meanwhile, prudent lending standards and extensive lender forbearance will minimise the number of customers who struggle with their mortgage payments through this period.

UK Finance is forecasting the following for 2024:

+ Gross lending to fall by a further 5% to £215bn

+ Lending for house purchase to fall by a further 8% to £120bn

+ External remortgaging activity to fall by a further 8% to £60bn

+ Internal product transfers to fall by 8% to £202bn

+ Buy-to-let purchase lending to fall by a further 13% to £7bn

+ Arrears to increase to 128,800 cases by the end of 2024.

+ Possessions to increase by 16% to 5,100 – this would still see possessions lower than in any year from 2019 all the way back to 1981, when the mortgage market was a little over half its current size.

James Tatch, head of analytics at UK Finance, said: “2023 was a challenging year for both prospective and existing mortgage borrowers, facing affordability pressures from higher interest rates and the increased cost-of-living, as well as house prices still at elevated levels relative to income. In the face of these challenges, borrowing for house purchase has been constrained. At the same time most existing customers looking to refinance their loans chose to take a Product Transfer with their current lender, where affordability tests are not required.

“With these pressures unlikely to ease significantly in the short term, we expect lending to remain weak in 2024, with a gradual improvement in affordability reflected in a modest increase in activity levels in 2025.

“The challenging environment has also pushed more households into mortgage arrears. However, the rigorous affordability tests in place since 2014 are now working to ensure that the vast majority of customers can still afford their mortgage payments even with the increased pressure on their finances. Although we forecast more customers will encounter arrears next year, we expect numbers to peak well below levels seen previously.

“As always, any customers who do find themselves in difficulty should speak to their lender at an early stage, as the industry continues to provide help to anyone struggling with a range of tailored support options.”

Market overview: a sharp contraction following post-lockdown strength

Amidst the ongoing squeeze on household finances, 2023 was, as expected, a difficult year for mortgage customers.

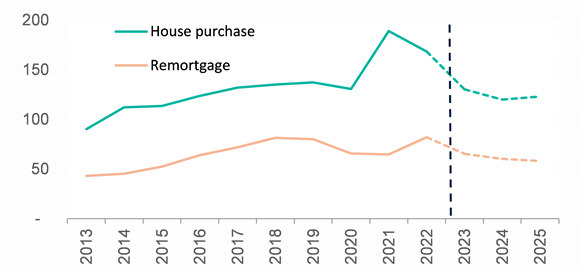

For those looking to enter or move in the housing market, the higher cost-of-living and interest rate rises seen since the start of 2022 significantly raised the bar for consumers to pass affordability tests for mortgages. This led to a fall in lending for house purchase in 2023 of some 23%, to £130bn. In 2024, despite some easing in cost pressures, the level of prices and interest rates will continue to weigh heavily, and we forecast house purchase lending will fall by a more modest eight percent to £120bn.

The same factors have also acted as a brake on activity in the external remortgage market, which fell by 21% in 2023 to £65bn. However, with lenders competing to retain customers against a backdrop of weak new lending volumes, more customers took out a new Product Transfer (PT) deal with their existing lender, which are not subject to affordability tests. The PT market grew by 11 per cent in 2023 to £219 billion. Next year, we anticipate that both external remortgaging and PTs will fall away slightly, following a peak in maturing two-year fixed rate deals in 2023.

Chart 1: Residential lending, £ billions

Source: UK Finance forecasts

Although the outlook for next year is for a modest further contraction, UK Finance see conditions beginning to improve in the following year. By 2025, the combination of wage growth, softer house prices and inflation and interest rates falling back somewhat will see a gradual recovery in lending activity as affordability improves.

Buy-to-let activity constrained on multiple fronts

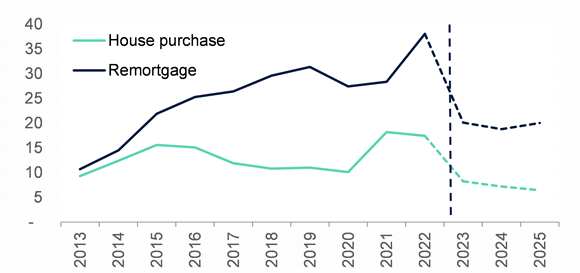

Cost and rate pressures have also depressed buy-to-let (BTL) lending, but this market has also faced taxation and regulatory headwinds through 2023. The cumulative effect of these factors has meant that BTL lending has experienced a sharper contraction than the residential market. New BTL house purchase lending fell by 53% in 2023, and remortgaging by 47%. Next year, UK Finance forecast a smaller contraction but the greater challenges for BTL investors remain, particularly for smaller-scale landlords who are less able to spread costs across their portfolios.

Chart 2: Buy-to-let lending, £ billions

Source: UK Finance forecasts

Arrears increase but set to peak well below previous cycles

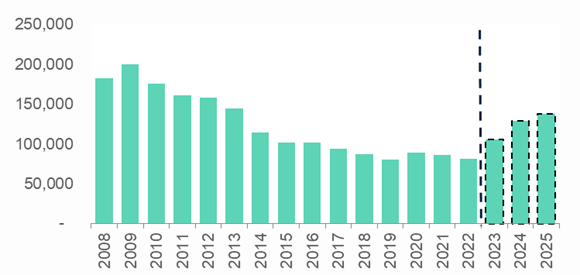

In line with UK Finance’s previous forecasts the pressure on household finances, which had built through 2022, began to feed through into an increase in mortgage arrears by the end of that year. This continued through 2023 and, by the end of the year, reached an estimated 105,600 cases with arrears of over 2.5% of the outstanding mortgage balance – an increase of 30% compared with December 2022. Next year, although no significant increase in Bank Rate is expected, the existing pressure on payments will persist, and we forecast arrears will rise to 128,800 by the end of 2024. In 2025, UK Finance predict arrears will rise more modestly to 137,800 cases, as the pressure on mortgage payments begins to recede.

Chart 3: 1st charge mortgages in arrears

Source: UK Finance

Despite these increases, a number of factors are minimising the extent of payment problems and ensuring that over 99% of the 10.8m mortgages in the UK are not now in arrears. Firstly, the affordability tests for all new lending since 2014 ensure that customers can afford their mortgage payments, even at a higher (stressed) interest rate. Secondly, unemployment – historically the main cause of mortgage arrears – is at very low levels. And where customers are struggling with their mortgage payments, lenders have a range of tailored forbearance options which they can deploy on a case-by-case basis to best help borrowers’ individual circumstances.

These mitigating factors mean that, whilst arrears are increasing, numbers will peak well below levels seen in previous cycles.

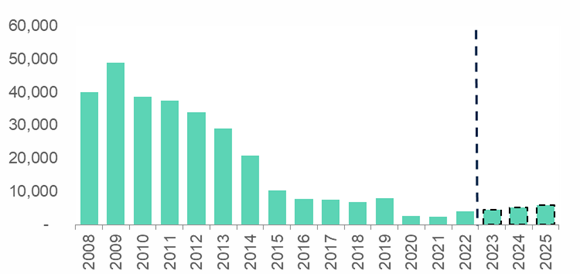

Whilst arrears will continue to rise next year, UK Finance do not anticipate a commensurate increase in mortgage possessions. There were an estimated 4,400 possessions through 2023, an incredibly low number by historic comparisons, excluding the artificially suppressed numbers through 2020 and 2021 during the pandemic.

Next year UK Finance expect only a small increase to 5,100, with this activity still relating to historic cases, most of which pre-date the pandemic. With a continuing favourable labour market, extensive lender forbearance and gradually improving affordability, the vast majority of customers now falling behind will eventually recover their positions. The very small minority of cases where this is not possible will not feed through into any material increase in possessions over our forecast period.

Chart 4: 1st charge mortgage possessions

Source: UK Finance