UK Finance Arrears and Possessions data for Q2 of 2021 shows that total mortgage arrears remain close to historically low levels due to the mitigating effects of payment deferrals and other tailored forbearance, as illustrated in the charts below.

Early trends shows that arrears are moving on twin tracks; Covid-19 related support has helped customers to remain out of arrears but those in pre-pandemic financial difficulty have continued to build up arrears, notwithstanding the application of payment deferrals.

From March 2020 – 31 March 2021, lenders offered payment deferrals of up to 6 months to customers and buy-to-let landlords where Covid-19 had impacted their ability to meet their monthly mortgage payments, with a total of 2.9 million granted while the scheme was active.

For most borrowers who took one, payment deferrals provided a short-term solution to a change in their economic circumstances due to the Covid-19 pandemic, allowing mortgage borrowers to defer payments to meet other financial commitments. While the Covid-19 payment deferral scheme has now ended, lenders are continuing to offer tailored forbearance and support to borrowers who continue to need help meeting their mortgage payments.

It remains the case that mortgage payment deferrals have helped to support customers who were not in financial difficulty at the beginning of the pandemic to remain out of arrears, as borne out in the data.

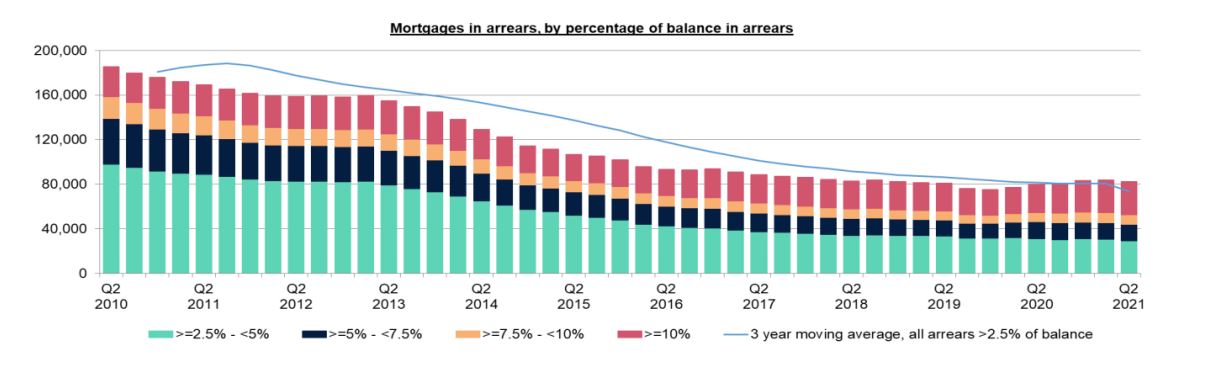

Overall, there was a reduction of 1,370 mortgages in arrears compared to the previous quarter, with a total of 76,270 homeowner mortgages in arrears of 2.5 per cent or more of the outstanding balance.

Within the total, there were 26,560 homeowner mortgages in early arrears (those between 2.5 and 5 per cent of balance in arrears), a decrease of 5 per cent on the previous quarter.

Over the same period in 2020, the number of mortgages in early arrears increased modestly, largely due to payment difficulties caused by the first lockdown prior to payment deferrals being introduced. Since then, payment deferrals provided those borrowers who found themselves in early arrears with the ability to pay these off.

These actions resulted in an overall decline in early homeowner arrears over the course of 2020, with the number of cases in Q2 2021 remaining lower than the number of cases before the Covid-19 pandemic began.

The winding-down of the Job Retention Scheme by end September 2021 may have an impact on this decline. However, as lenders continue to offer forbearance, it is anticipated that the early arrears will increase at a gradual pace as the economic impacts of the pandemic continue to unfold.

Within the overall total, there were 27,910 homeowner mortgages with more significant arrears (representing 10 per cent or more of the outstanding balance), an increase of 630 on the previous quarter.

This figure has slowly increased since Q1 2020, but from a low base. These increases are largely driven by customers with more complex circumstances who had several missed payments before the pandemic. These borrowers may have made use of the full six months of payment deferrals and are most likely receiving or (in need of) the help available through lenders’ tailored forbearance support.

There were a total of 6,020 buy-to-let mortgages in arrears of 2.5 per cent or more of the outstanding balance in the second quarter of 2021, a small increase of 50 on the previous quarter. The continued small increases in buy-to-let arrears from a low base are likely due to the Covid-19 pandemic. Lenders are continuing to support buy-to-let customers with payment difficulties resulting from Covid-19.

Only 210 homeowner mortgaged properties and 230 buy-to-let mortgaged properties were taken into possession in the second quarter of 2021.

It is important to note that year-on-year comparisons will look unusually large due to the Possession Moratorium that was in place from March 2020 – 1 April 2021. No involuntary possessions took place in this period.

There were only 90 more possession cases in Q2 2021 than the quarter before. Government restrictions on evictions were in place until 31 May 2021 in England and 30 June 2021 in Wales. Additionally, lenders continue to prioritise those requiring urgent resolution due to vulnerability or where it is of benefit to the customer.

This means that there is no expectation of significant increases in possessions immediately following the lifting of the Possessions Moratorium and restrictions on evictions.

Instead, possessions are expected to increase slowly as the backlog of cases from 2020 unwind.

Comments (1)

A huge sigh of relief for the market with this news.