While higher mortgage rates and increased competition among sellers has dampened typical spring growth, the housing market has shown resilience in the face of global uncertainty, Rightmove reports.

While higher mortgage rates and increased competition among sellers has dampened typical spring growth, the housing market has shown resilience in the face of global uncertainty, Rightmove reports.

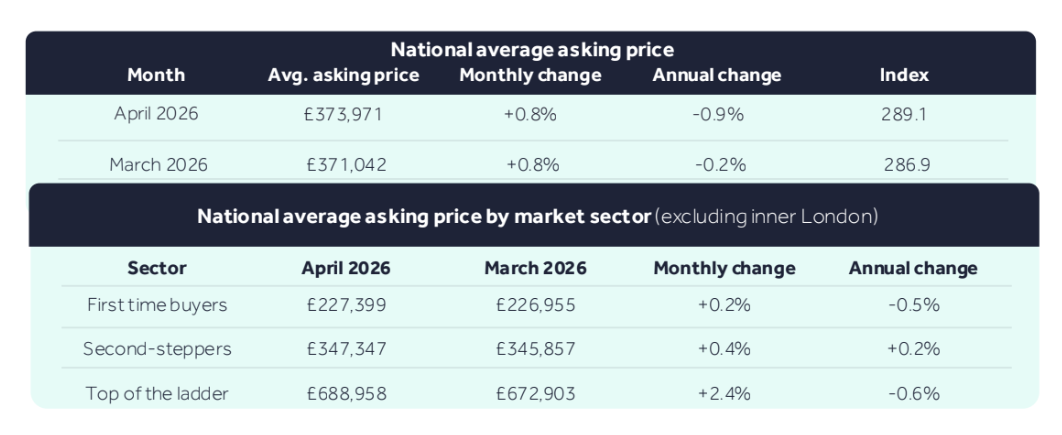

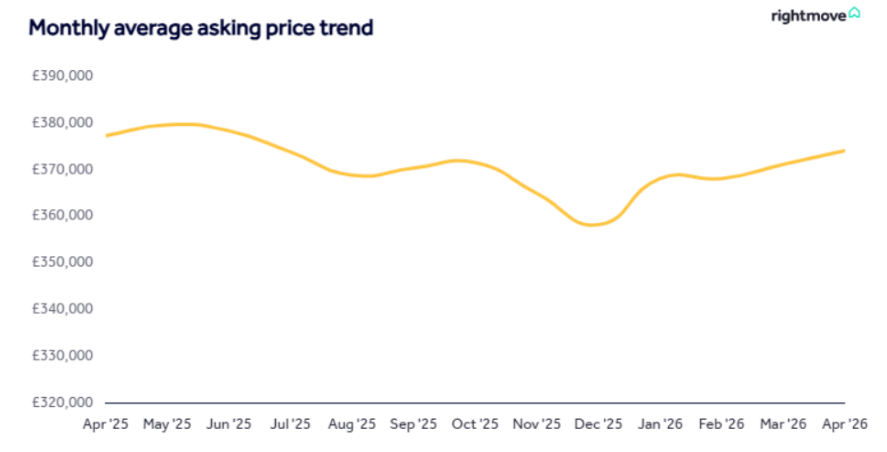

Data from the platform shows the average price of a newly listed home increased by 0.8% (+£2,929) this month to £373,971 – below the long-term April average rise of 1.2%. The more subdued growth comes as borrowing costs remain elevated and the number of homes for sale sits at its highest level for this time of year in 11 years.

Despite these pressures, market activity has held up relatively well. Buyer demand in April to date is 7% lower than the same period last year, but broadly in line with trends seen earlier in 2026. The number of sales agreed is just 3% behind last year, while new listings are only 1% lower and remain 13% higher than in 2024.

Price growth has been strongest at the top end of the market, particularly among larger homes where buyers are less reliant on mortgages. Scotland also outperformed, with asking prices rising by 4.3%.

Colleen Babcock, property expert at Rightmove, said: “With mortgage rates remaining elevated due to the war in Iran, it’s not a surprise that price growth is proving strongest in parts of the market less exposed to higher borrowing costs, such as top-of-the-ladder homes, while sectors more exposed to interest rates are seeing slower momentum.

“Across Great Britain, Scotland stands out as an example of resilience, with average prices rising by over 4%. Lower average asking prices and a faster home-buying process continue to support price growth in the Scottish market.

“However, for most of the market, the combination of rising mortgage rates and the number of homes for sale being at its highest level for the time of year over a decade means that competitive pricing is crucial for sellers looking to attract buyer interest and secure a sale this spring.”

Higher borrowing costs have been driven by global instability, with Rightmove’s mortgage tracker showing the average two-year fixed rate has risen to 5.42%, up from 4.25% before the onset of the Middle East conflict. This adds around £235 to a typical monthly mortgage payment.

However, several factors are helping to support activity. Average earnings are up 3.9% year-on-year, outpacing asking prices, which are down 0.9% annually, while recent changes to loan-to-income lending rules mean buyers can typically borrow more. Demand among first-time buyers has also remained relatively robust, down just 6% compared with last year.

Matt Smith, Rightmove’s mortgage expert, said: “At the start of the year there was growing optimism that the base rate would continue to fall, but that picture has shifted following the conflict in Iran. Financial markets are now largely pricing in further Bank of England base rate increases this year rather than cuts, which has fed through into higher mortgage rates compared with earlier in 2026 and this time last year.

“The initial shock appears to have passed, with mortgage rates stabilising over the past couple of weeks, but they remain elevated. The next moves will depend on upcoming UK inflation data and how the Bank of England responds. If policy decisions align with current market expectations, a period of relative stability is more likely than meaningful falls.”

Smith added: “Even if external pressures ease, including improved conditions in the Middle East, history suggests mortgage rates are unlikely to come down quickly, meaning higher borrowing costs are set to remain in place for the foreseeable future.”

I am not having a go at Rightmove here. It is doing exactly what any listed business would do, which is present the market in the best possible light.

But this kind of language does not stand up when you look at the underlying facts in England and Wales.

Agents are paid on completed transactions, not listings, not traffic, and not asking prices.

Since 2021, transaction volumes in England and Wales have fallen from around 1.08 million to about 0.70 million. With roughly 16,000 branches, that means the average office has gone from completing about 68 deals a year to around 44. That is a reduction of roughly 35 percent in activity per branch.

Even allowing for slightly higher average prices, that equates to around £80,000 less revenue per office.

But the idea that prices are holding up also needs proper scrutiny.

When you look at transaction price movement by segment, the picture is not one of strength. The top end has been under the most pressure, with clear reductions in achieved values, while the middle and lower bands have been flatter or only marginally positive.

That matters, because the top 20 percent disproportionately drives fee income. When that segment weakens, total fee pool falls faster than headline averages suggest.

So this is not a stable pricing environment. It is a market where value is being eroded at the top and activity is constrained across the board.

At the same time, the cost of money has moved from around one percent to nearer five percent. That fundamentally changes affordability and removes a significant number of buyers from the market.

You can also see it in behaviour. Every property still on the market is a property that has not sold. Every listing is an unsold outcome. Every click is someone who looked and decided not to proceed.

So strong traffic is not a sign of strength. It is a sign of hesitation.

If demand were truly resilient, properties would clear. They would not sit.

At the same time, Rightmove’s average revenue per advertiser has risen from around £1,077 per month in 2020 to about £1,621 today. That is roughly £6,500 more per branch per year, with little change in the number of advertisers.

So agents in England and Wales are doing fewer deals, earning materially less, taking longer to get paid, and paying more to access the market.

That is the hard economics.

I am fully aware that pointing this out will not be universally welcomed. There are plenty of voices in the industry whose business models depend on staying close to the portals, and it is easier to repeat the narrative than challenge it.

But none of that changes the underlying reality.

The market may look busy, but it is less productive, more price sensitive, and more fragile than it was in a low interest rate environment.

That is why describing it as “resilient” does not reflect what is actually happening at branch level.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register