Gráinne Gilmore, head of research at Zoopla, has provided EYE with her view of the pandemic-led market and what may be coming down the line as Covid restrictions begin to ease.

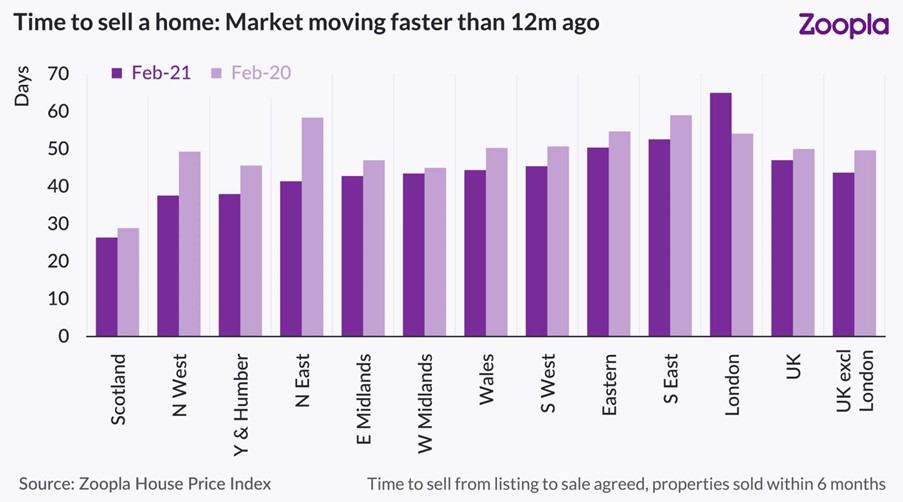

One of the most striking themes to emerge from the market data a year on from the first lockdown is the rise in speed at which the sales market is moving. The time between listing a property and agreeing a sale has fallen by nearly a week to 44 days outside London over the last 12 months.

As we know however, the sheer level of activity in the market means that more pressure is being put on the process from the sale agreed stage onwards. The time taken to get to sale complete has stretched out by weeks since last year.

The shorter timeframes in which homes are being snapped up once listed, however, reflects the increased competition in the housing market at present, as rising buyer demand is not matched by the flow of new stock. The Chancellor’s Budget announcement resulted in an immediate 28% spike in buyer demand, and, if we look at average buyer demand levels over the last 11 weeks, it is still running 13% higher than the average levels seen across the whole of 2020.

The biggest jump in demand after Mr Sunak announced the stamp duty extension in early March was for three-bed homes, and this type of home remains the most ‘in-demand’. However, the biggest post-Budget bounce in demand in the South East and London was for flats, suggesting increased interest from first-time buyers or those looking to take advantage of the stamp duty extension.

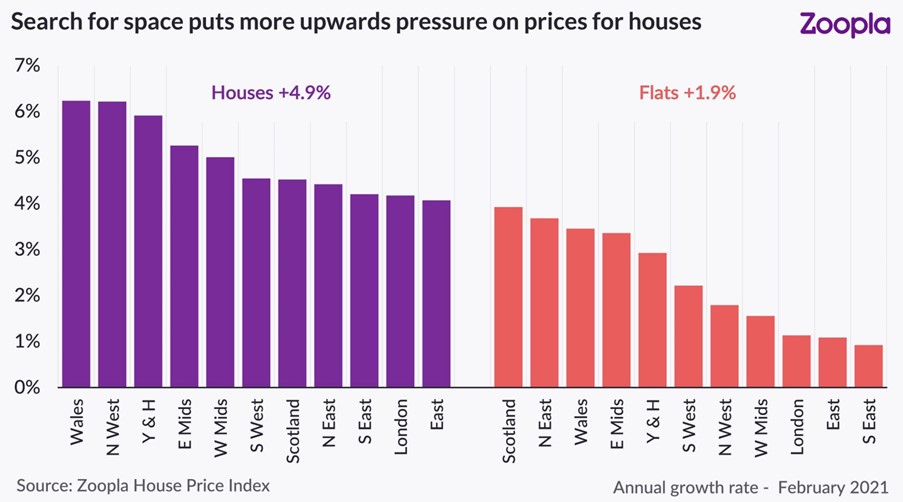

The continued demand for houses across the country, as buyers ‘search for space’ following multiple lockdowns, is putting more upwards pressure on this type of property – and we can see that over the last year, the average price for a house has risen by 4.9%, compared to 1.9% for flats, as shown in the chart below.

The difference between houses and flats is evident when it comes to how quickly homes are selling. This time last year, flats took an average of 55 days to reach a sale agreed from listing, while houses took 49 days. Since then, the average time to sale agreed for houses has shrunk to 42 days, while for flats it has expanded to 62 days, meaning houses are now selling nearly three weeks faster than flats.

What next?

As lockdowns start to ease, and COVID-19 cases recede, we expect the constraints on supply to ease as sellers feel more comfortable inviting potential buyers into their home. This in turn will lead to more activity in the market. This could put increased pressure on the post ‘sale agreed’ sales completion process, something buyers and agents will be monitoring as we move through the summer and approach the September cut-off for the tapered stamp duty extension.

The continued levels of demand, boosted by the stamp duty extension and the increased availability of mortgages for first-time buyers under the new mortgage guarantee will support activity levels and headline house price growth up to the end of Q2 2021.

While market prospects have been supported by the Chancellor’s announcements at the Budget, the re-opening of the economy amid the unwinding of wider support measures is unlikely to be a smooth process.

Overall transactions are set to get an additional boost from the stamp duty measures, but price growth will ease from current levels during the course of 2021.

Comments are closed.