House prices are expected to record modest growth over the coming years, rising by 2.5% across Great Britain by the fourth quarter of 2026 as cooling inflation and easing interest rates support the market, according to the latest housing market outlook from Hamptons.

House prices are expected to record modest growth over the coming years, rising by 2.5% across Great Britain by the fourth quarter of 2026 as cooling inflation and easing interest rates support the market, according to the latest housing market outlook from Hamptons.

The estate agency forecasts that transaction volumes are likely to hold steady at around 1.15 million in 2026, with improving affordability balancing ongoing economic and tax pressures.

From 2027, however, political uncertainty and higher borrowing costs are set to weigh more heavily on the market, slowing price growth to 2.0% in late 2027 and 1.5% by the end of 2028. Prime markets are likely to remain subdued, with tax policy and broader uncertainty limiting mobility and delaying recovery.

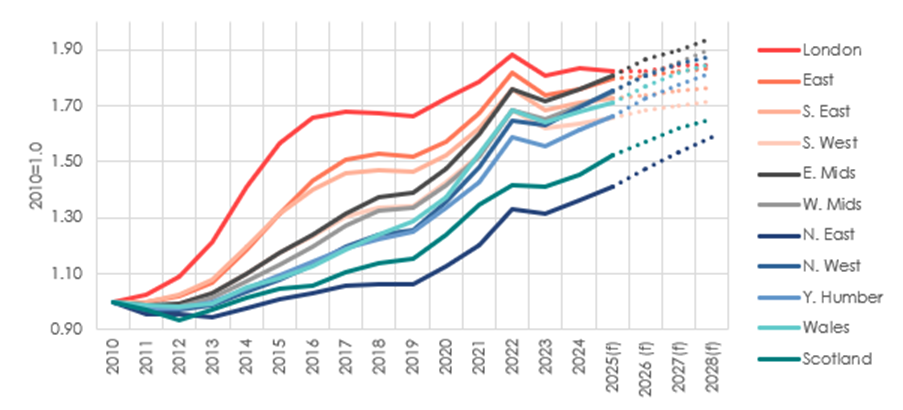

Notably, by next year the East Midlands is projected to have seen greater price growth since the 2009 market bottom than London, with the North West and West Midlands expected to follow by the end of 2027 – signalling a significant shift in the regional house price cycle.

Annual house price growth forecast

| Q4 2024 | Q4 2025 (f) | Q4 2026 (f) | Q4 2027 (f) | Q4 2028 (f) | 4

year total (2024-28) |

|

| London | 1.5% | -0.5% | 0.0% | 1.0% | 0.0% | 0.5% |

| East of England | 1.2% | 2.0% | 0.5% | 1.0% | 0.5% | 4.1% |

| South East | 1.6% | 1.0% | 0.5% | 1.0% | 0.5% | 3.0% |

| South West | 1.0% | 1.5% | 1.5% | 1.0% | 1.0% | 5.1% |

| East Midlands | 2.3% | 3.0% | 3.0% | 2.0% | 2.0% | 10.4% |

| West Midlands | 2.9% | 3.0% | 3.5% | 2.5% | 2.5% | 12.0% |

| North East | 3.9% | 3.5% | 4.5% | 4.0% | 3.5% | 16.4% |

| North West | 3.9% | 3.5% | 3.0% | 2.5% | 1.5% | 10.9% |

| Yorkshire & Humber | 3.8% | 3.0% | 4.0% | 2.5% | 2.5% | 12.5% |

| Wales | 2.1% | 2.0% | 3.5% | 2.5% | 2.0% | 10.4% |

| Scotland | 3.1% | 5.0% | 3.0% | 3.0% | 2.0% | 13.6% |

| Great Britain | 2.4% | 2.0% | 2.5% | 2.0% | 1.5% | 8.2% |

Source: ONS & Hamptons

Hamptons predicts that inflation is likely to fall faster than anticipated next year, allowing for two or three base rate cuts. It also expects the Bank Rate to settle at around 3.25% by the end of 2026, with typical mortgage rates stabilising at around 4%. This should improve the availability of sub-4% mortgage deals, even for borrowers with smaller deposits, helping to support price growth and activity.

Affordability is improving on paper, with earnings growth running ahead of inflation. While some households rolling off shorter fixed-rate deals are seeing lower monthly payments, others are still adjusting to higher costs. There are around 600,000 borrowers on ultra-low sub-3% five-year fixes who’ll be rolling off in 2026 and 2027.

London & prime markets – a recovery delayed

At this stage in the cycle, Hamptons would typically expect the London market to regain momentum. Historically, the capital leads recoveries once affordability improves, but this time the rebound looks muted.

Since 2016, London has consistently underperformed the rest of Great Britain, and our forecasts suggest that trend will continue – a reversal of what we previously expected. The agency anticipate flat growth (0%) across Greater London in 2026 as the market digests recent tax changes.

While small price falls are expected in the £1.9m+ segment, this is likely to be offset by growth in the mainstream market, where improving affordability and easing mortgage rates are starting to support buyer confidence.

One growing challenge is the lack of price growth for higher-value homes. Declining prices – particularly in Prime Central London – mean a rising share of households are selling for less than they paid. In 2025, 14% of London sellers sold at a loss, up from 6% in 2016. This disincentivises moves and encourages owners to stay put, especially when faced with the high cost of Stamp Duty Land Tax on their next purchase.

As a result, the London market is increasingly being driven by first-time buyers, who accounted for 50% of homes sold in the capital this year.

The decision to raise stamp duty earlier this year – combined with wider tax concerns, including changes to non-dom status and speculation around capital gains and inheritance tax – has created a challenging backdrop for high-value markets. The new council tax surcharge on homes worth over £2m adds another layer of cost, further dampening sentiment and therefore values.

Prime Country markets, where council tax bills are already significantly higher than in London, could come under even greater pressure from this surcharge. These areas saw strong growth post-Covid, but political uncertainty and tax burdens are now prompting many households to delay moving.

Properties above the £2m mark could see around a 5% price correction, but this is expected to be a one-off adjustment rather than a prolonged decline, as markets absorb the change and stabilise. Tax rates remain below European and US equivalents.

2027–2028: A higher inflation era and political risk

It looks increasingly likely that 2026 will mark the end of the rate-cut cycle, and the years ahead look more uncertain too, according to Hamptons. Inflation is expected to remain above the 2% target, and mortgage rates could begin to edge higher in 2027 as markets begin to factor in future interest rate increases. Against this backdrop, house price growth across Great Britain is forecast to slow to around 2.0% in Q4 2027 and 1.5% in Q4 2028.

Political uncertainty will become a more prominent driver of sentiment, particularly in prime markets in 2028 – the year before the planned election. Tax policy is increasingly acting as a levelling-up mechanism, limiting recovery in higher-value markets in London and the South.

London is forecast to see around 1.0% growth in 2027, before stalling again in 2028. The growing burden of stamp duty and other levies will continue to dampen activity.

In real terms (i.e. inflation-adjusted), house prices are likely to continue underperforming, with affordability stretched and uneven earnings growth. While headline wage growth may remain strong – driven in part by fewer entry-level roles – the benefits will not be evenly distributed. This will particularly impact first-time buyers and renters.

Over the four-year forecast period, the North East is set to see the strongest growth (16.4%), followed by Scotland (13.6%) and Yorkshire & The Humber (12.5%). These regions have seen some of the weakest growth since 2010, so this acceleration marks a catch-up phase.

Cumulative house price growth across the regions since 2010

Source: ONS & Hamptons

While London has historically been the safe bet for long-term price growth, the picture is changing. Since Q4 2010, when house prices bottomed out, prices in London have risen by 84%, outperforming every other region and the Great Britain average of 74%. But next year could mark a turning point: the East Midlands is forecast to overtake London in cumulative growth, with the North West and West Midlands following by the end of 2027.

By 2028, Hamptons expect prices across Great Britain to have risen by 84% since 2010. The East Midlands will be the top performer over the period (94%), followed by the West Midlands (90%) and the North West (88%). London will fall to fourth place and will be the only region where average prices remain below their 2022 peak. This shift reflects stronger affordability and economic resilience in these regions compared with the capital.

Transaction volumes are forecast to rise slightly to 1.2 million across Great Britain in 2027, before dipping back to 1.15 million in 2028 as political uncertainty ahead of the 2029 election leads to a pause, particularly in prime markets. Overall, the market is expected to become increasingly sentiment-driven, with volatility around key political events.

Transactions forecast

| 2024 | 2025(f) | 2026(f) | 2027(f) | 2028(f) |

| 1,076,970 | 1,150,000 | 1,150,000 | 1,200,000 | 1,150,000 |

Source: HMRC & Hamptons

Property transactions versus growth in the total number of households

Source: HMRC & Hamptons

At the same time, people are moving less often – and making bigger, more “future-proofed” moves when they do. Despite there being 10% more owner-occupied households in England since 2008, transaction numbers remain around 19% below the average level seen in the three years before the 2008 financial crash.

Without today’s significant tax barriers, Hamptons adds that it would expect around an extra 100,000 moves each year. If stamp duty were eradicated entirely, transaction volumes could regularly surpass 1.4 million annually, similar to the post-pandemic peak in 2021.

Comments are closed.