This week, I am joined by the experienced agent Toby Martin as we delve into the key property market headlines for 10th week of 2025 ending on the 16th March 2025.

UK Property Market Highlights this week

.

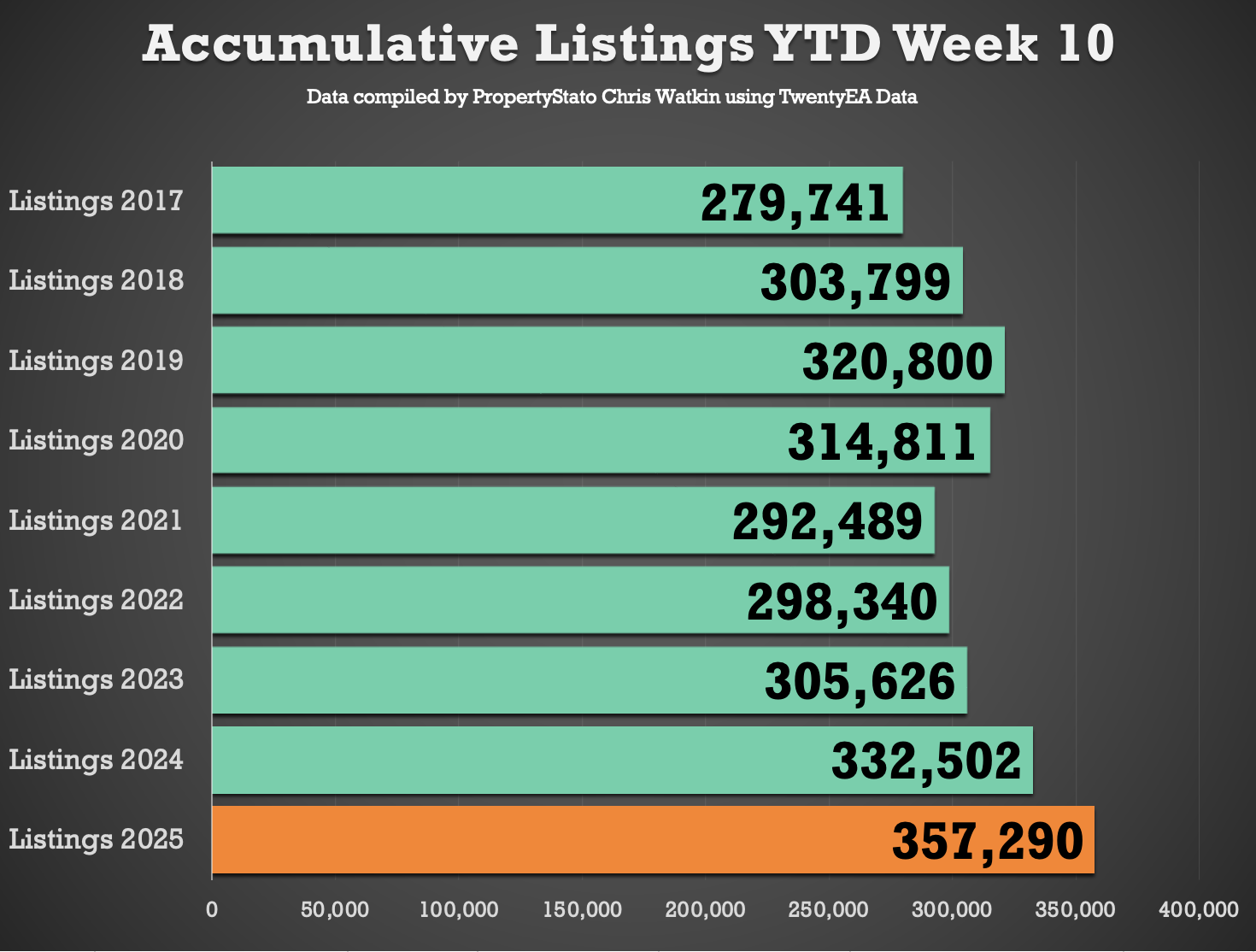

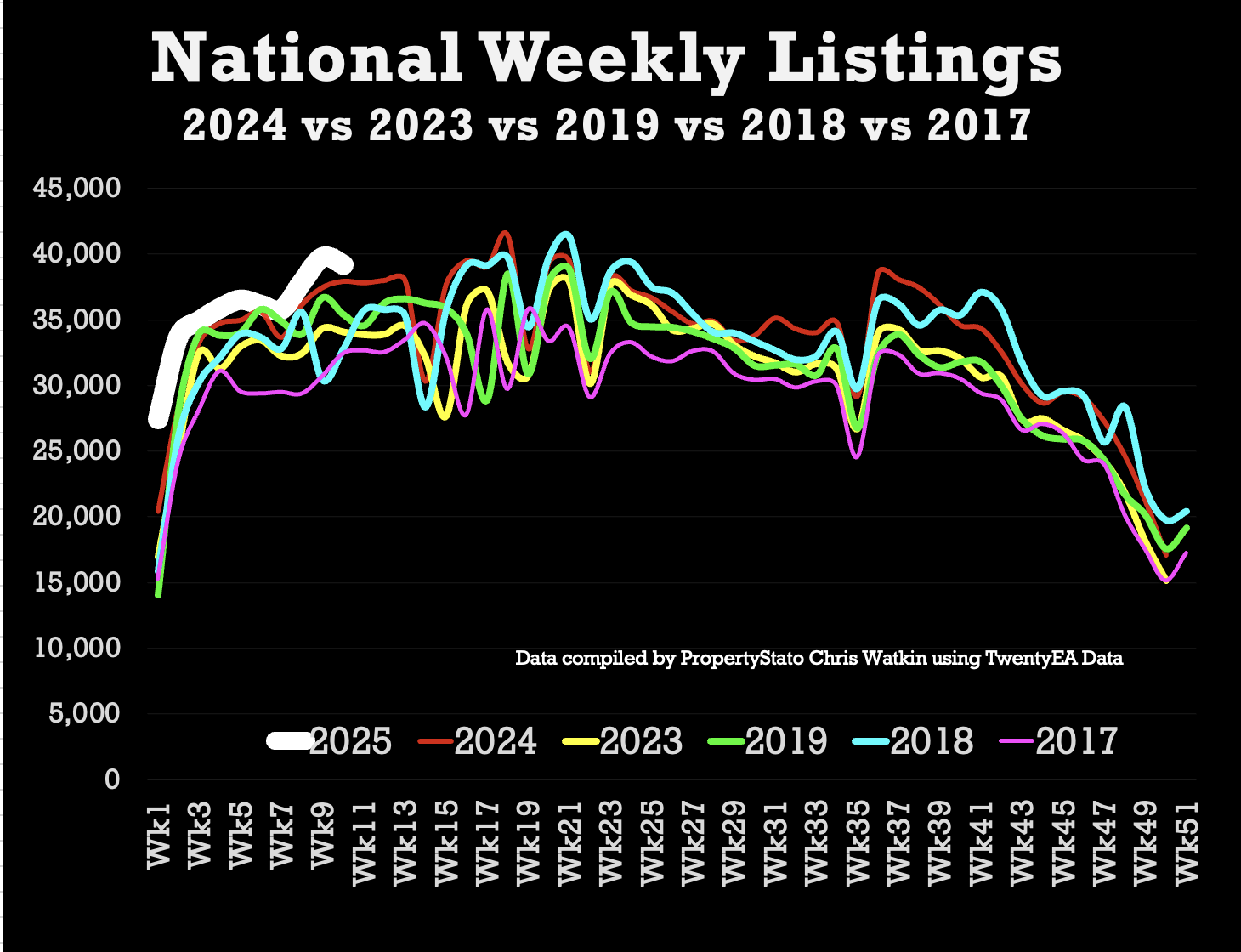

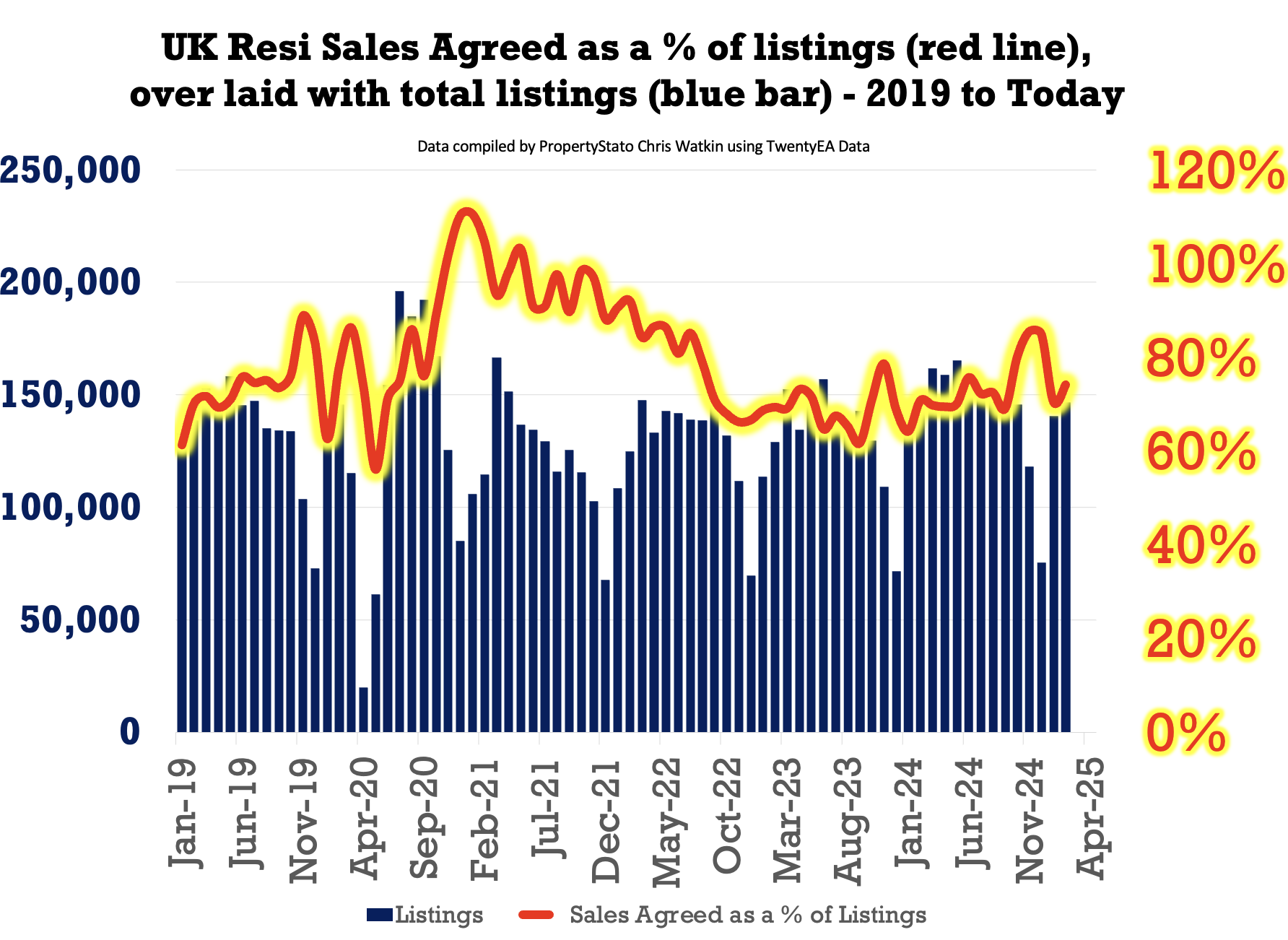

✅ Listings (New Properties on the Market)

39.2k new listings this week (last week 39.8k). That’s 7% higher than Week 10 of 2024 YTD and 10% higher YTD compared to 2017/18/19.

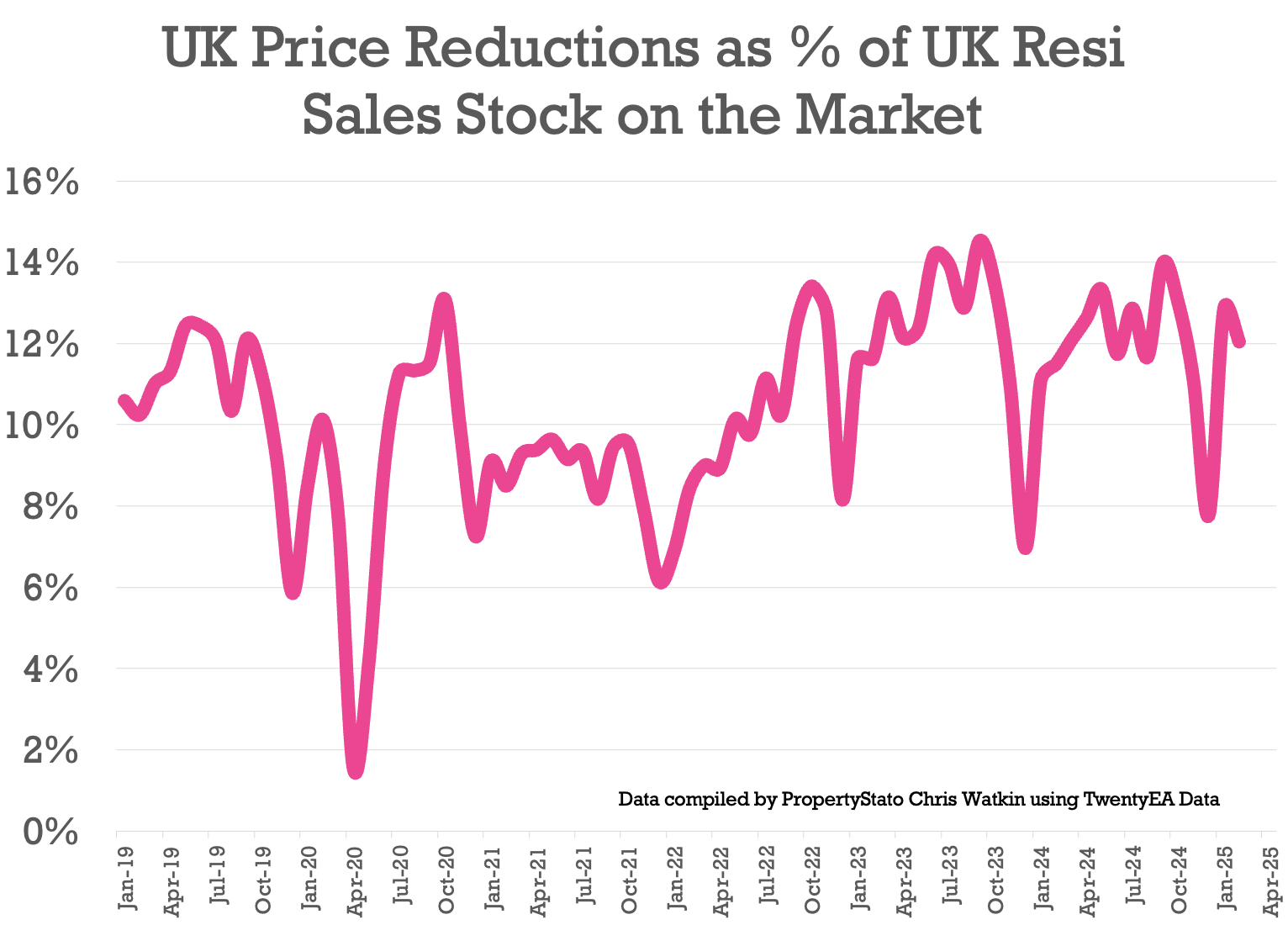

✅ Price Reductions (% of Resi Stock)

24k Price Reductions this week – meaning an approx. run rate of one in eight of residential property sales stock per month is being reduced (12%).

For comparison, 12.1% average in 2024, though the long-term five-year average is 10.6%.

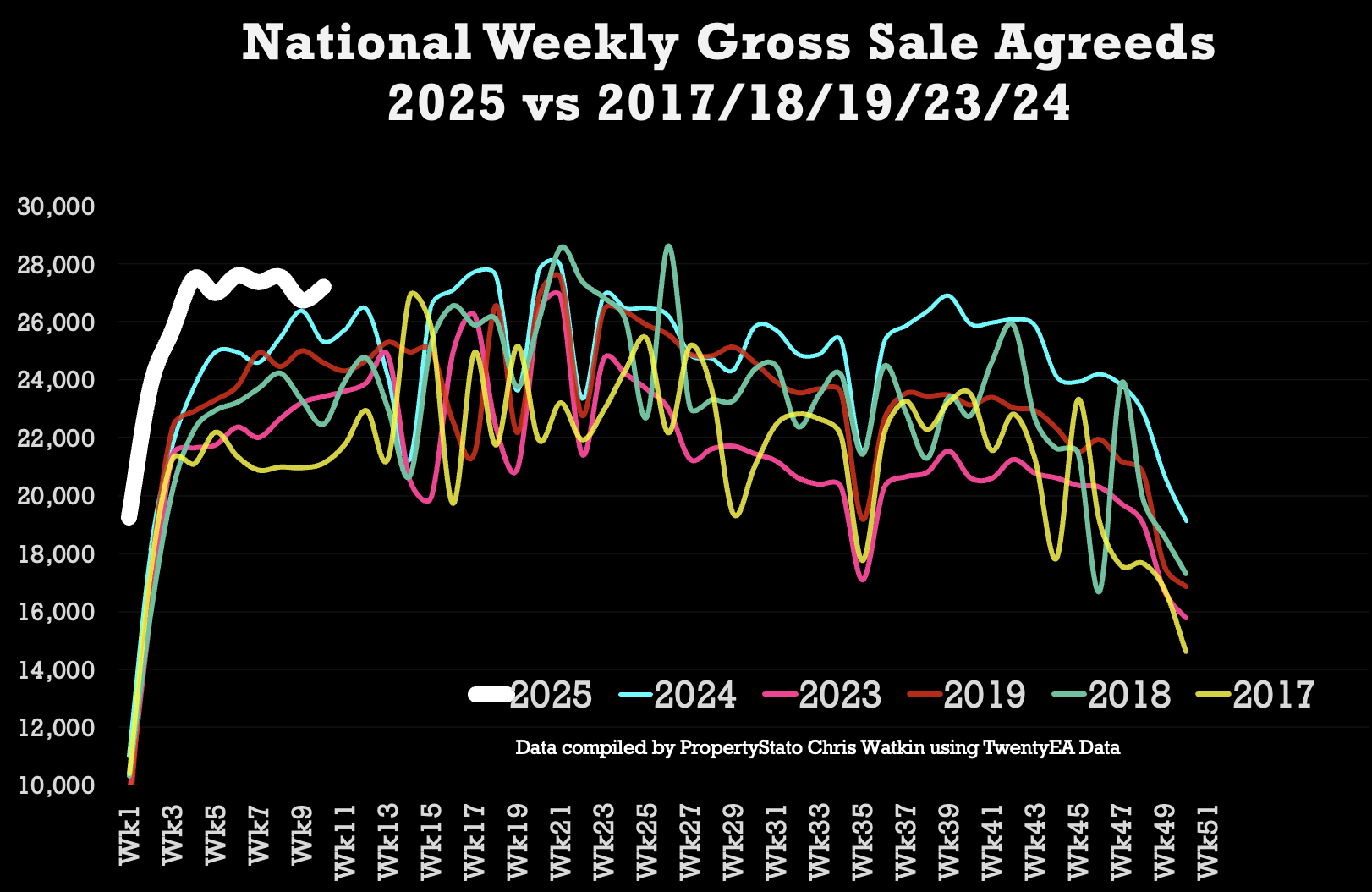

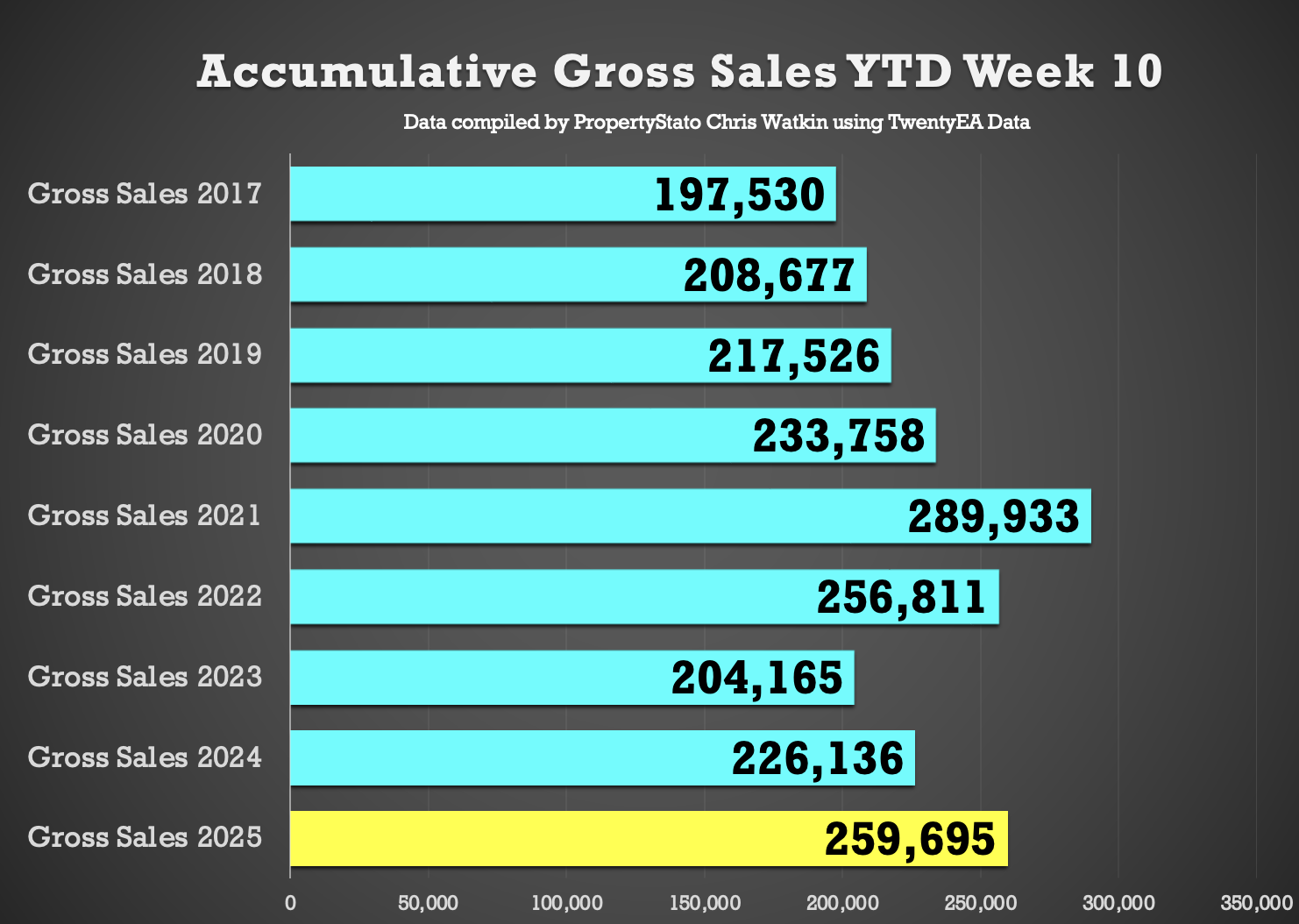

✅ Total Gross Sales (Agreed Sales)

27.2k UK homes sold STC this week, slightly up from 26.7k last week in Week 9. That’s 15% higher YTD compared to 2024 and 25% higher than 2017/18/19 YTD levels.

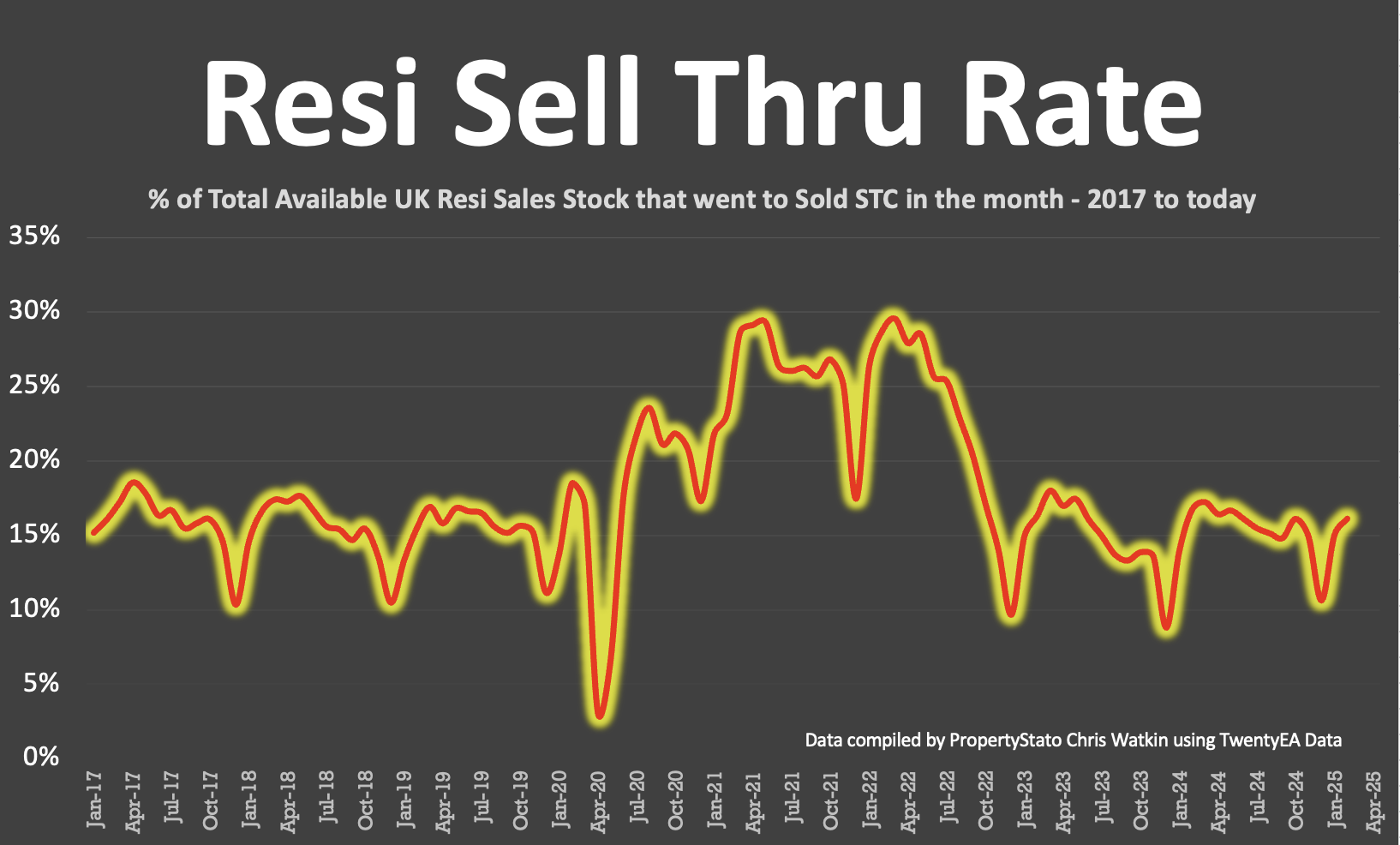

✅ Sell-Through Rate (Monthly in Arrears)

February’s run rate of 16.2% of residential property stock sold STC (i.e. 16.2% of Estate Agents properties on the market went sale agreed in February). For comparison, 16.7% of residential sales stock sold in February 2024. 2024 monthly average: 15.3%. Long-term 8-year average: 17.9%.

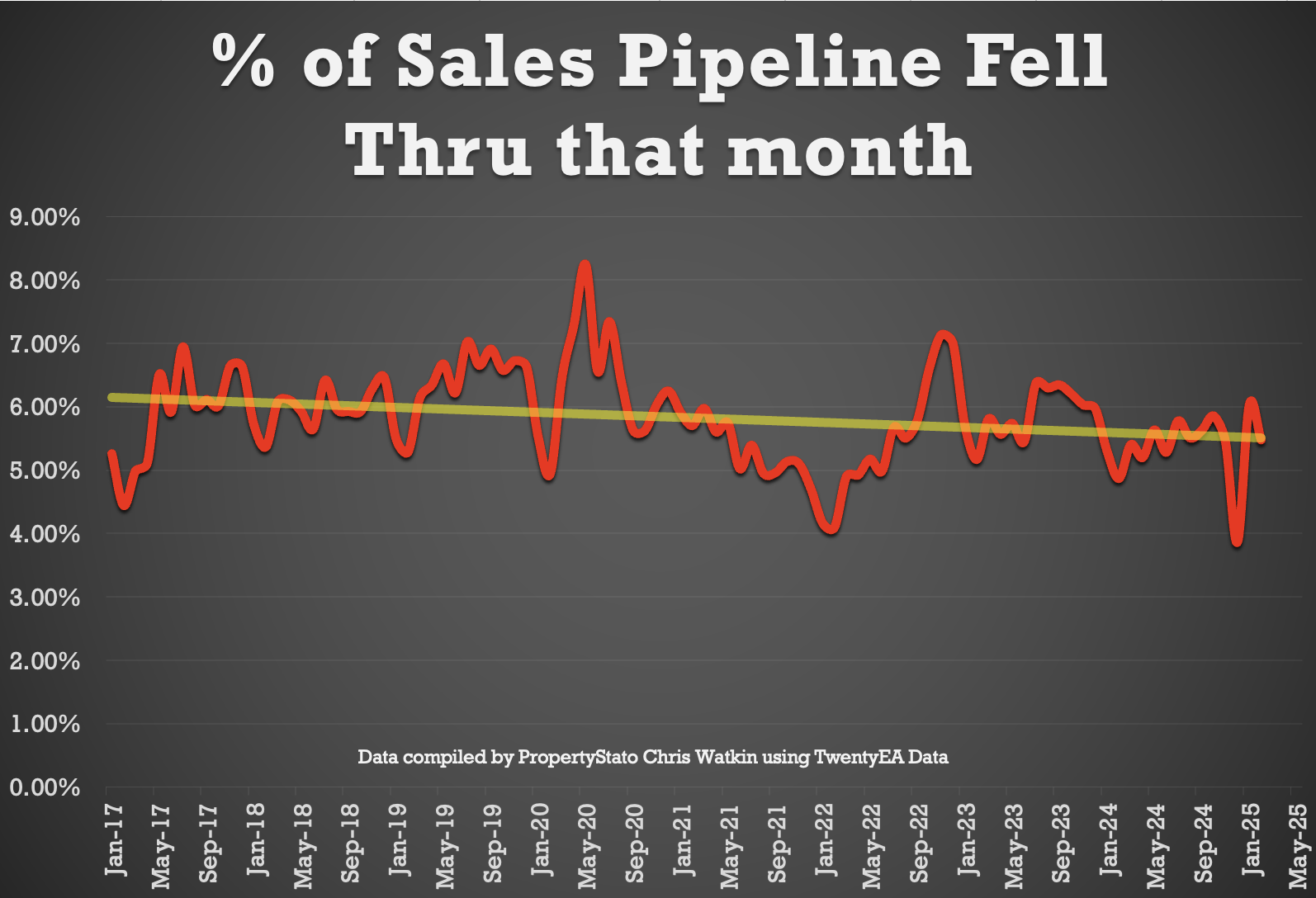

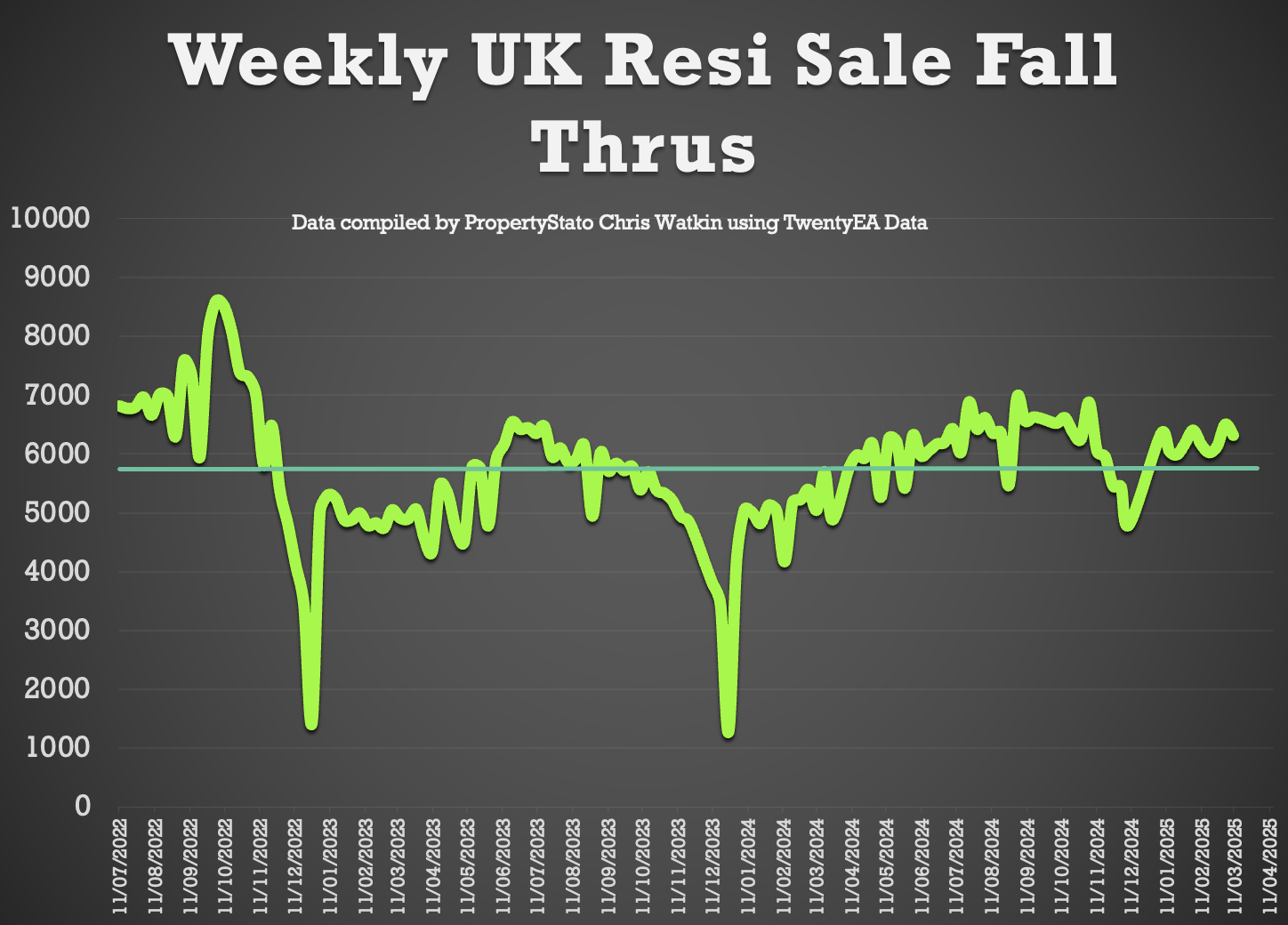

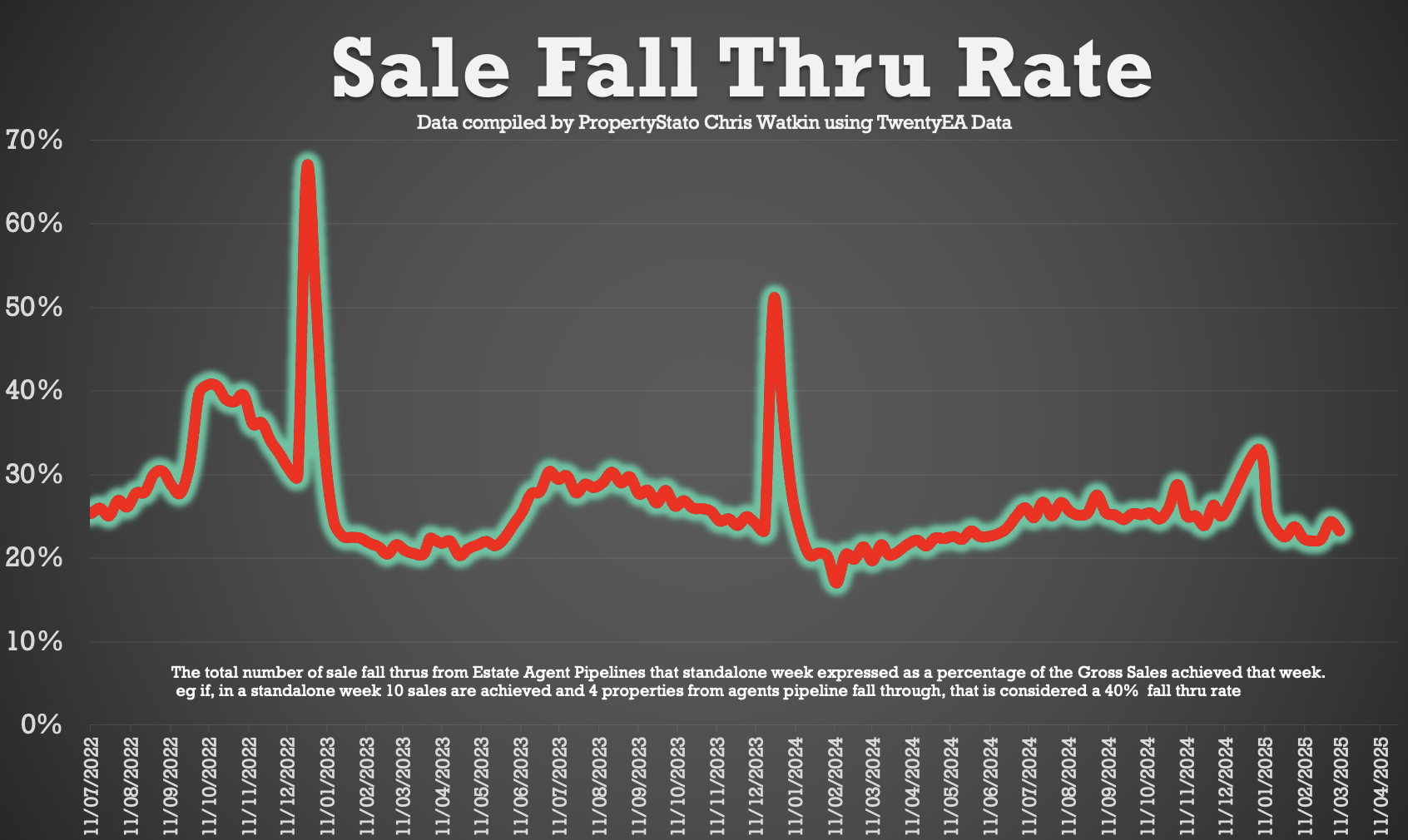

✅ Sale Fall-Throughs

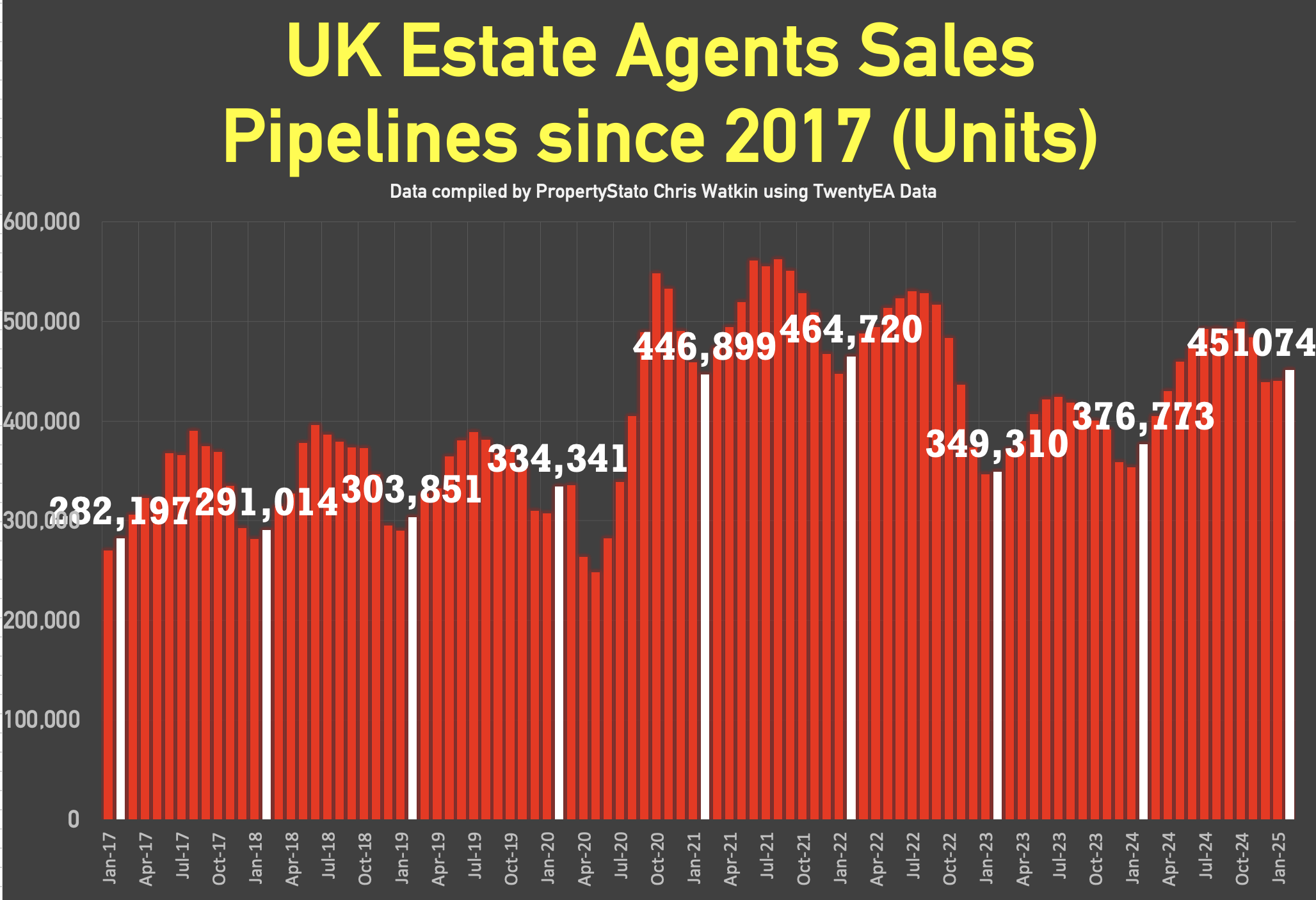

6,319 Sale fall-thrus last week from Resi Sale Sales Pipeline of 451,074 homes sale agreed (sold stc).

Another method is that week’s sale fall thrus as a % of gross sales that week. This week, that is 22.3% (last week 24.3%). Just above the 7-year average of 24.2%, yet well below the 40%+ levels post-Truss Budget (Autumn 2022).

For February ’25 as a whole, 5.48% of sales in the UK agents pipelines fell thru in Feb 25. For comparison, 2024 average: 5.36%.

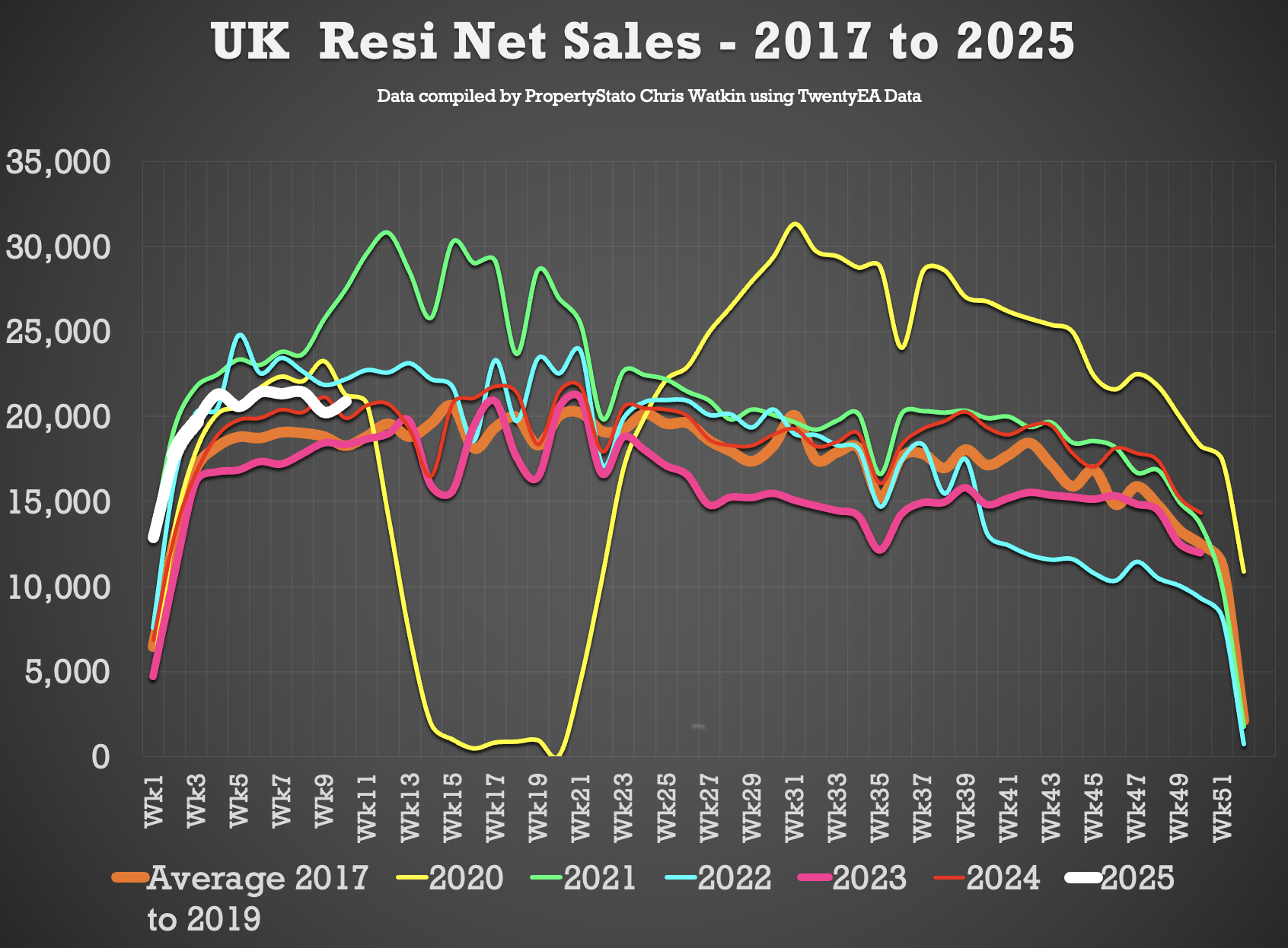

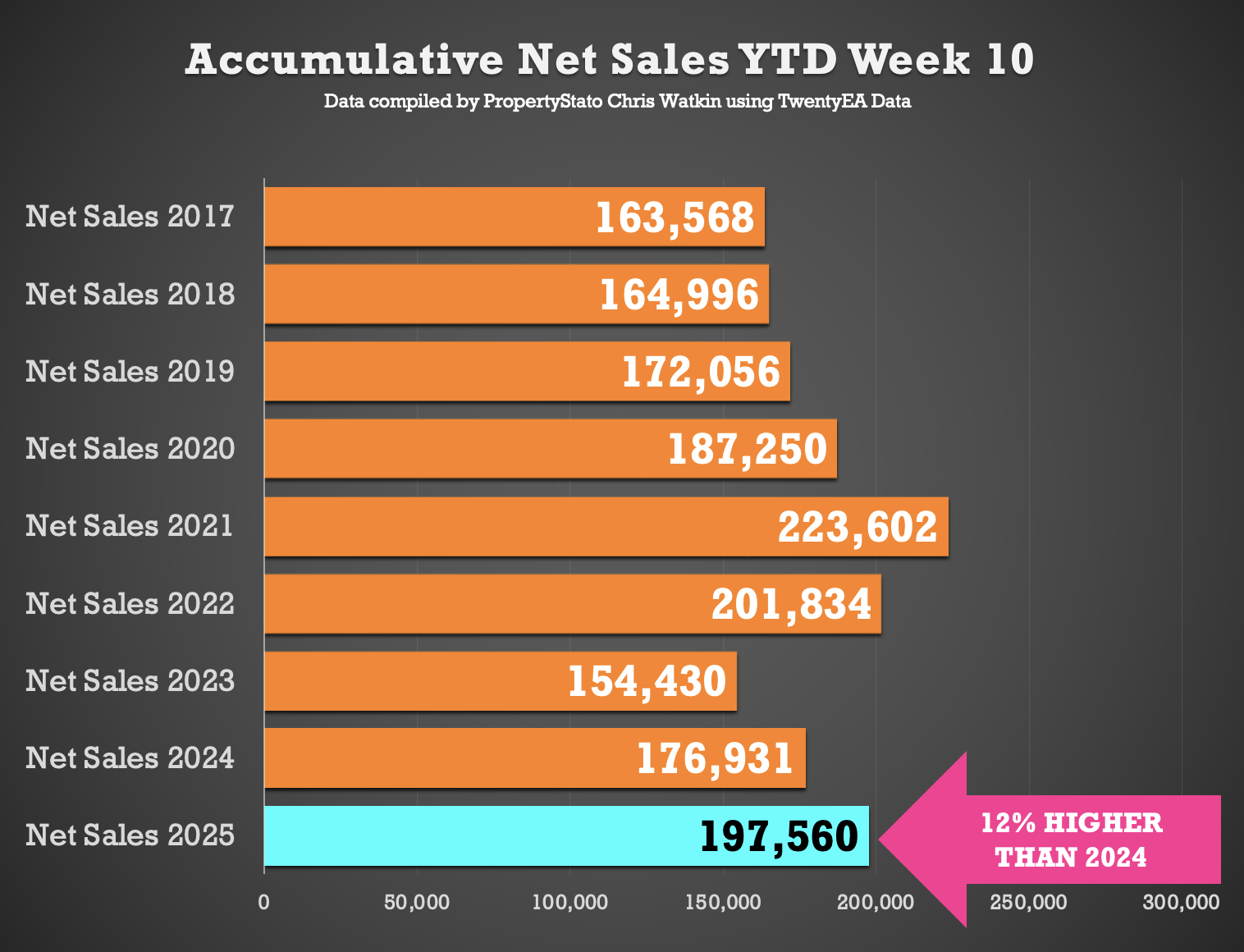

✅ Net Sales (Gross sales for the week less Sale Fall Throughs for the week)

20.9k net sales this week (20.2k last week), compared 2025 weekly average of 19.7k.

2025 YTD is 12% higher than compared to 2024 YTD and 18% higher than YTD 2017/18/19.

✅ Overvaluing

54% of properties that left Estate Agents books in the last 12 months, did the property exchange contracts (and the estate agent got paid and the vendor moved) – the remaining 46% left estate agents books withdrawn. The chart with the UK map shows the regional breakdown in the last 12 months and the with the pink bar chart shows the monthly UK breakdown to 2019

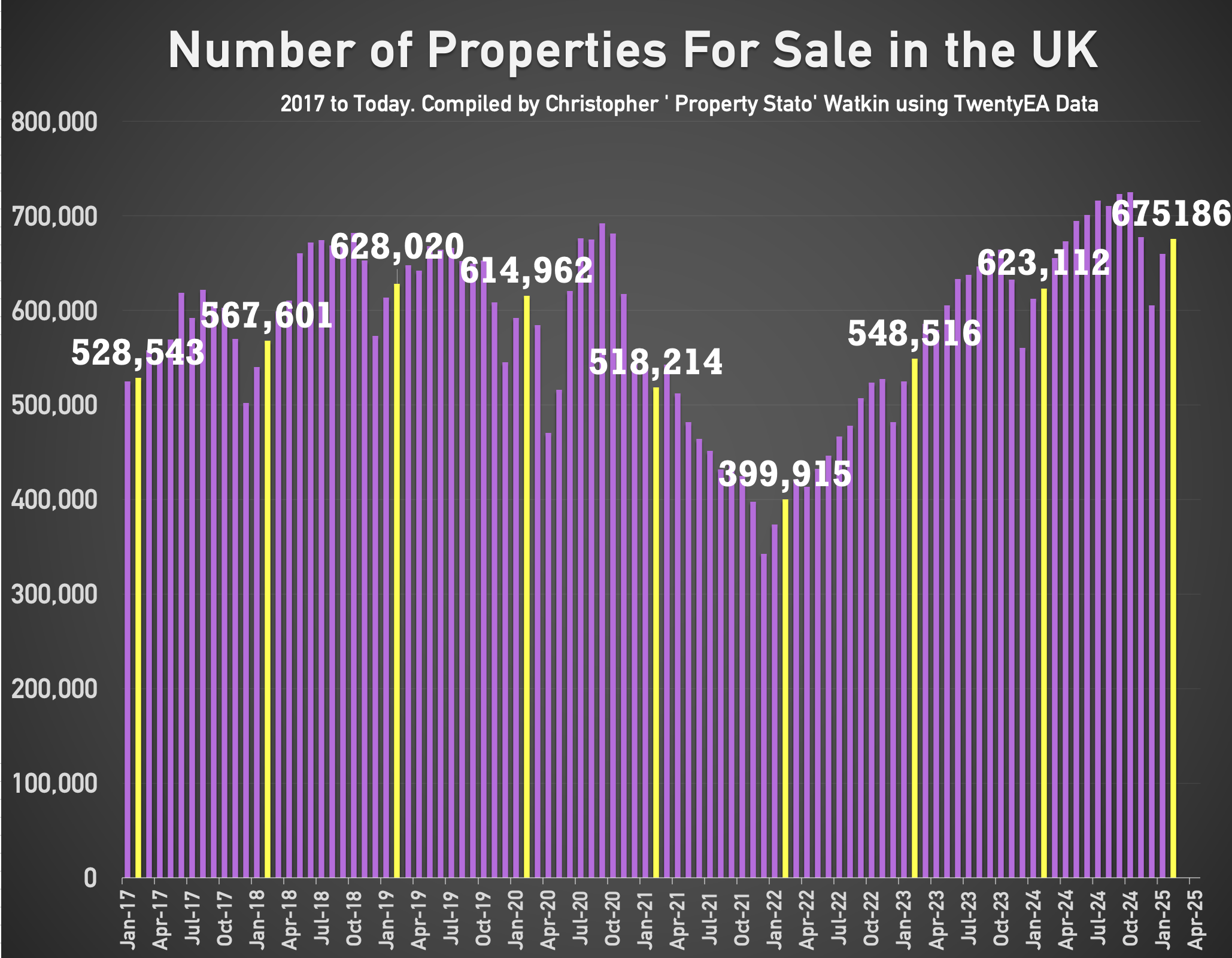

✅ Residential Sales Stock on the Market

675k properties on the market on the 1st March 2025 (monthly stat taken on the first day of the month).

Historical comparison for 1st march :

2024: 623k

2023: 548k

2022: 399k

2021: 518k

2020: 614k

2019: 628k

2018: 567k

2017: 528k.

✅ Residential Sales Sold STC Pipeline

451k sales agreed in Estate Agents Sales Pipeline (ie sold stc but not yet completed) as at the 1st March 2025 (monthly figure)

Historical comparison for 1st March :

2024: 376k

2023: 349k

2022: 464k

2021: 446k

2020: 334k

2019: 303k

2018: 291k

2017: 282k.

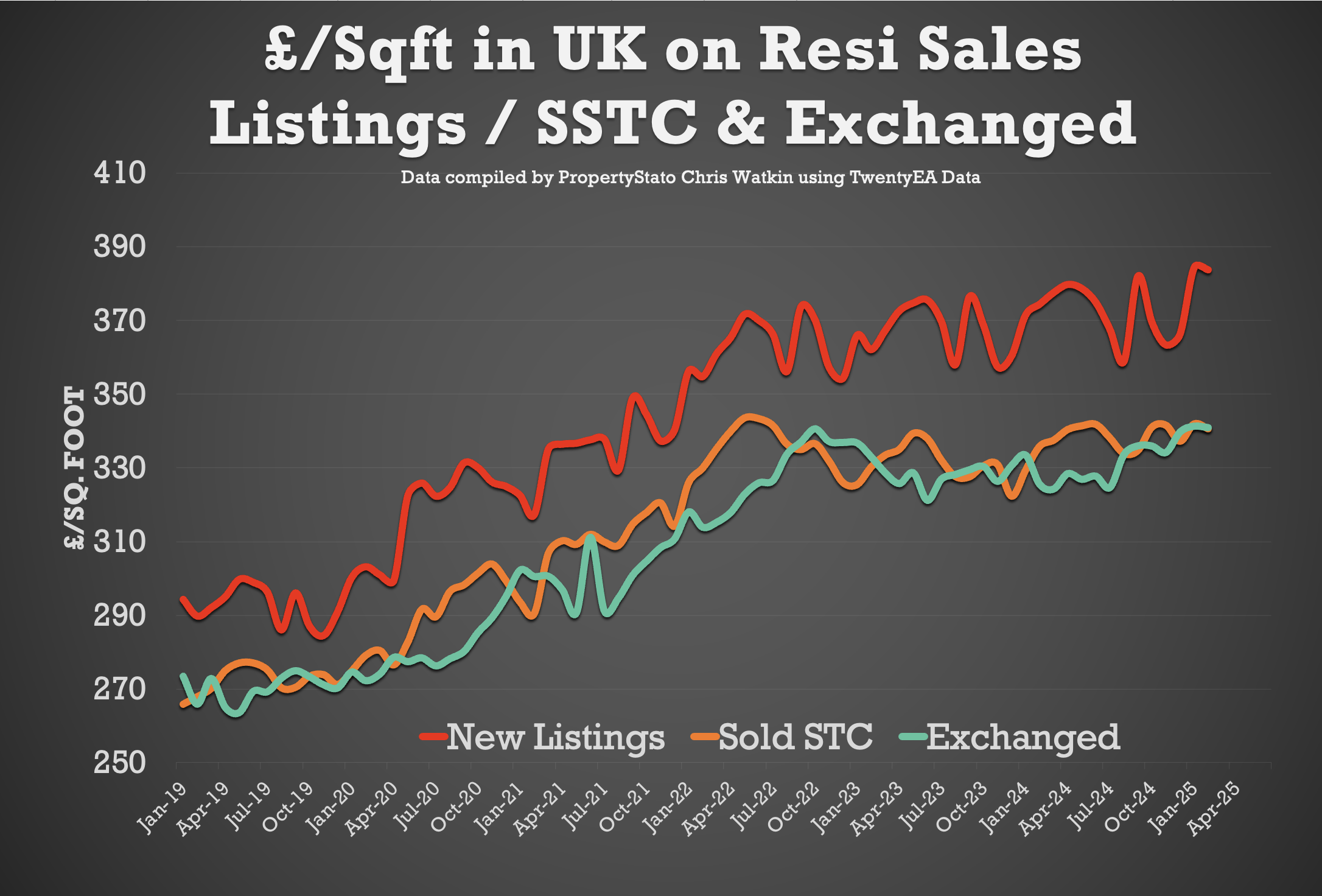

✅ UK House Prices (£/sq.ft)

As always, the £/sq.ft metric predicts Land Registry figures 5 months in advance with 92% accuracy (the orange line of the graph).

February’s final figure: £340/sq.ft.

January ’25 : £342/sq.ft

December ’24 : £339/sq.ft

August ’24: £334/sq.ft

February ’24: £335/sq.ft

This means UK house prices achieved in Feb ’25 were 0.39% lower than Jan 25, yet 1.64% higher than a year ago (Feb 24).

Local Focus this week – King’s Lynn

Always find this update very interesting-is this all UK sales or just secondhand i.e. excludes or includes new home sales?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

It excludes new homes.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Great piece on the market overall, Chris – and particularly insightful regarding the King’s Lynn area, which I’m involved in through Russen & Turner. I’ll definitely be taking a closer look at the Twenty EA software; it looks very impressive. It’s a pity the platform doesn’t reveal the fees agents are charging, though. I won’t go into too much detail on local fees here, but I’m aware that one of the agents mentioned operates on an upfront fee model, which can appear cheaper. That said, it’s reassuring to see that a more traditional ‘No Sale, No Fee’ approach delivers a higher sale price for the seller, making it a much stronger, more cost-effective and safer option overall.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Mark, your statistics with regard to your suitability rate was certainly very impressive as per what we said in the show.

I wouldn’t worry too much about these because I’m sure you know what your competitors are charging and it doesn’t take too much to work out what they’re turning over from the rest of the statistics That I mentioned in the show

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I’m particularly curious to see how things will evolve in the rental market. With more people struggling to get the property ladder, demand for rental properties is high, leading to increased rents in certain areas.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Interestingly, the number of first time buyers have asked three or four years has been increasing even with the increase in interest rates. But you’re right Wentworth that things could change going forward. Only time will tell.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register