This week’s UK Property Market Stats Show for week ending Sunday 23rd June 2024 features Alice Bullard, boss of Nested.

This week’s UK Property Market Stats Show for week ending Sunday 23rd June 2024 features Alice Bullard, boss of Nested.

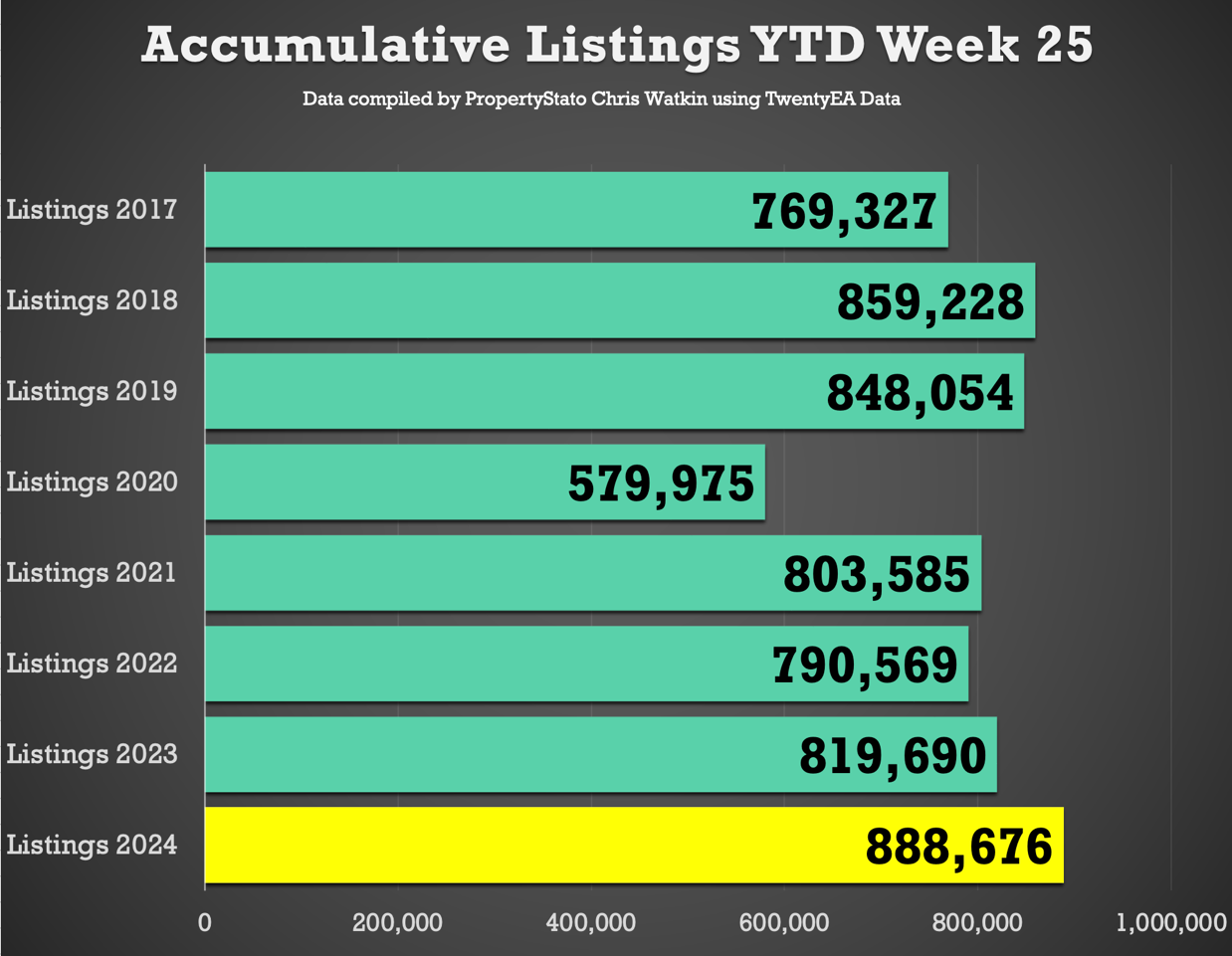

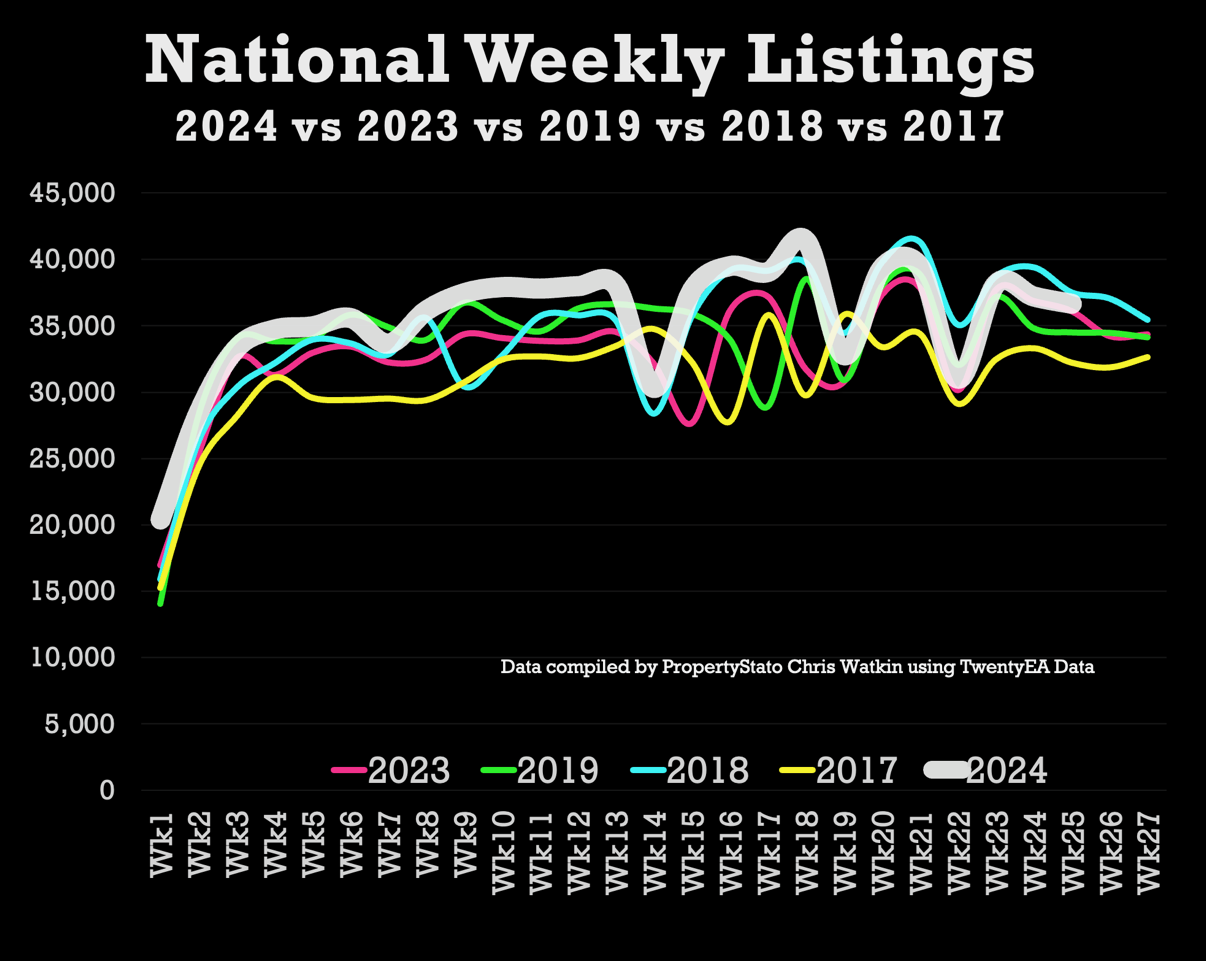

New Properties to Market: The UK saw 36,647 new listings. This year’s YTD listings stand at 888,676, 11.8% higher than the historical 8 year YTD average of 794,888, 7.6% higher than YTD 2017/18/19 and 8.4% higher YTD 2023. Weekly 2024 average : 35,547.

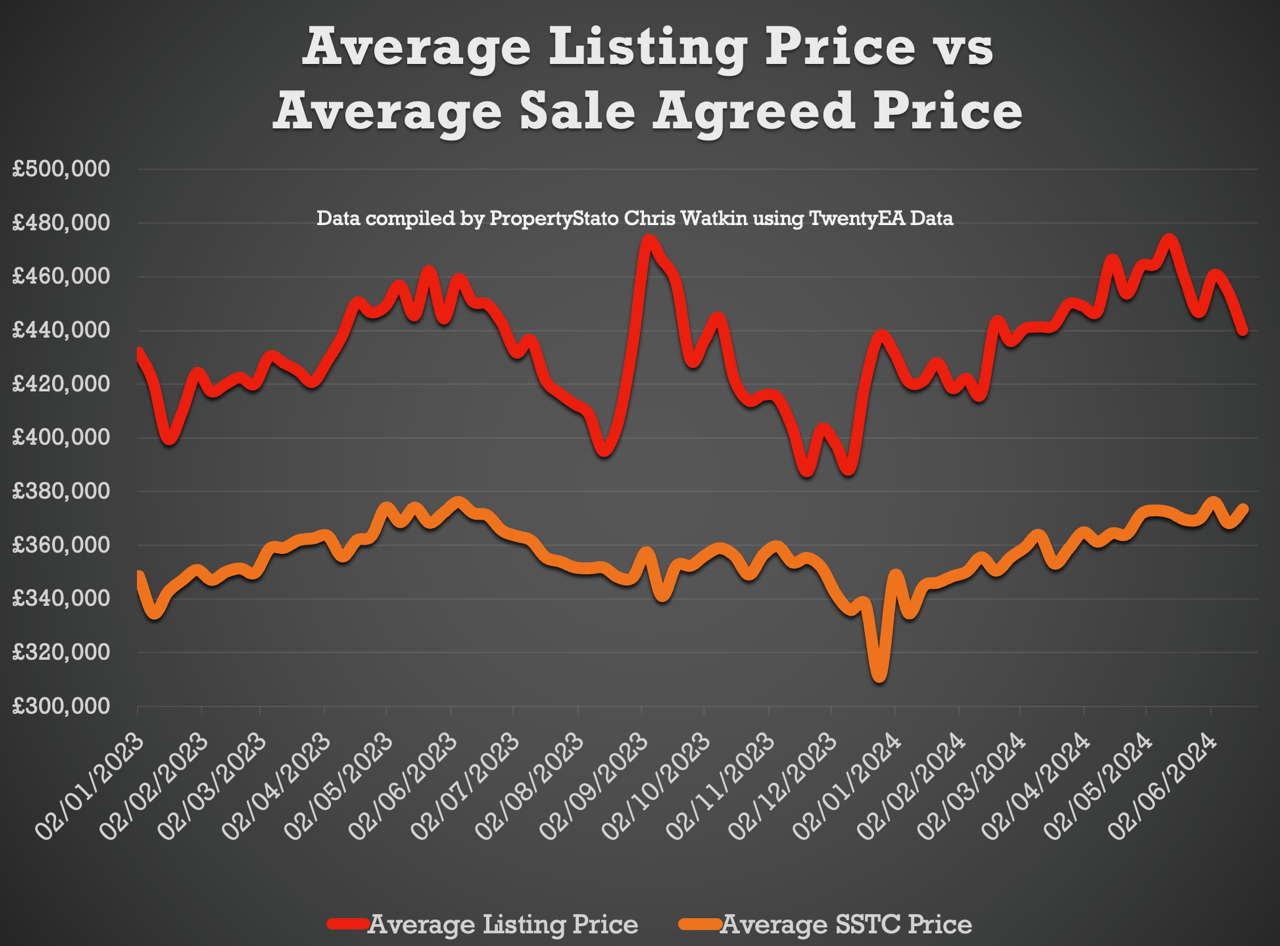

Average Listing Price: £439,996.

Average Asking Price of this week’s Listings vs Average Asking Price of the Properties that Sale Agreed this week: 17.9%. The long-term average is between 16% and 17%. It has been in the early mid/twenties in 2024. Let us hope this isn’t a blip.

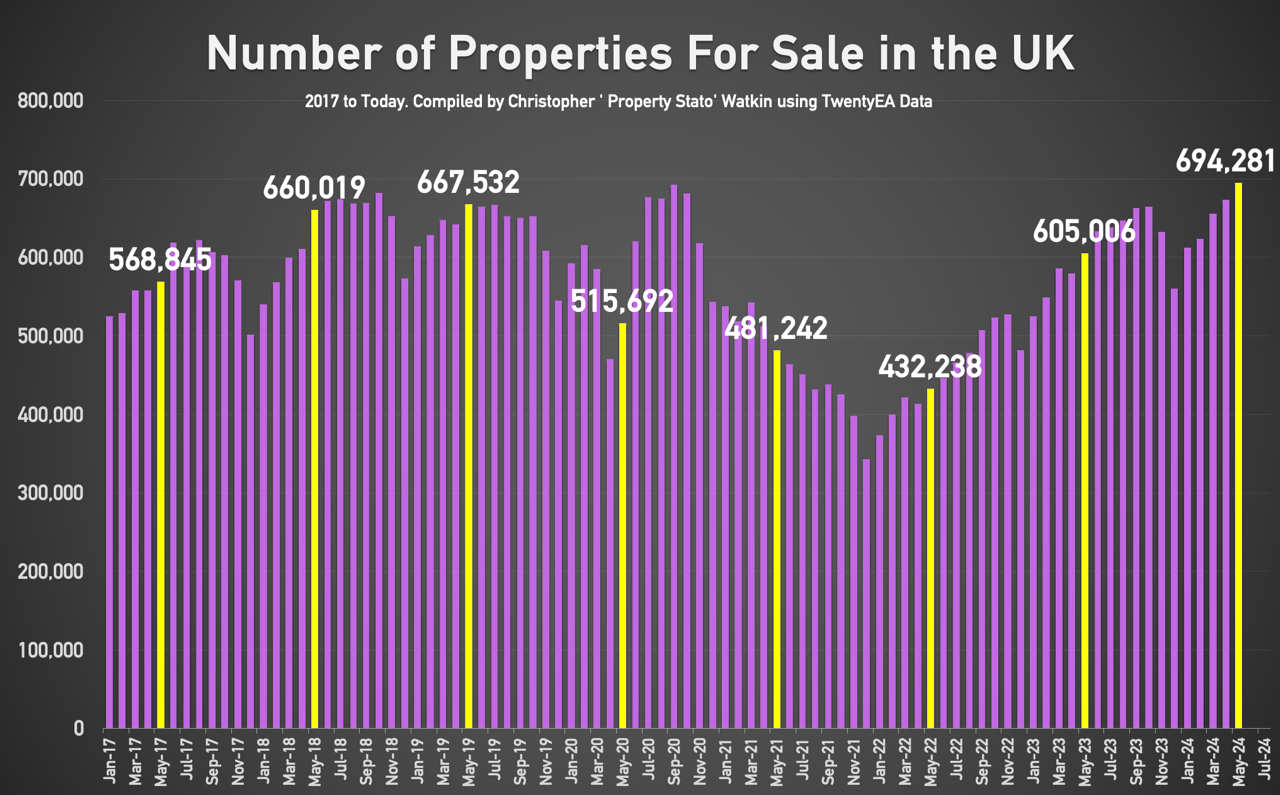

Price Reductions: Last week, 20,944 properties saw price reductions, higher compared to the 8-year Week 25 average of 18,142. Yet there is higher stock levels. Stock levels are at 694,281. This means 1 in 7.89 properties each month are being reduced.

Average Asking Price for Reduced Properties: £393,878.

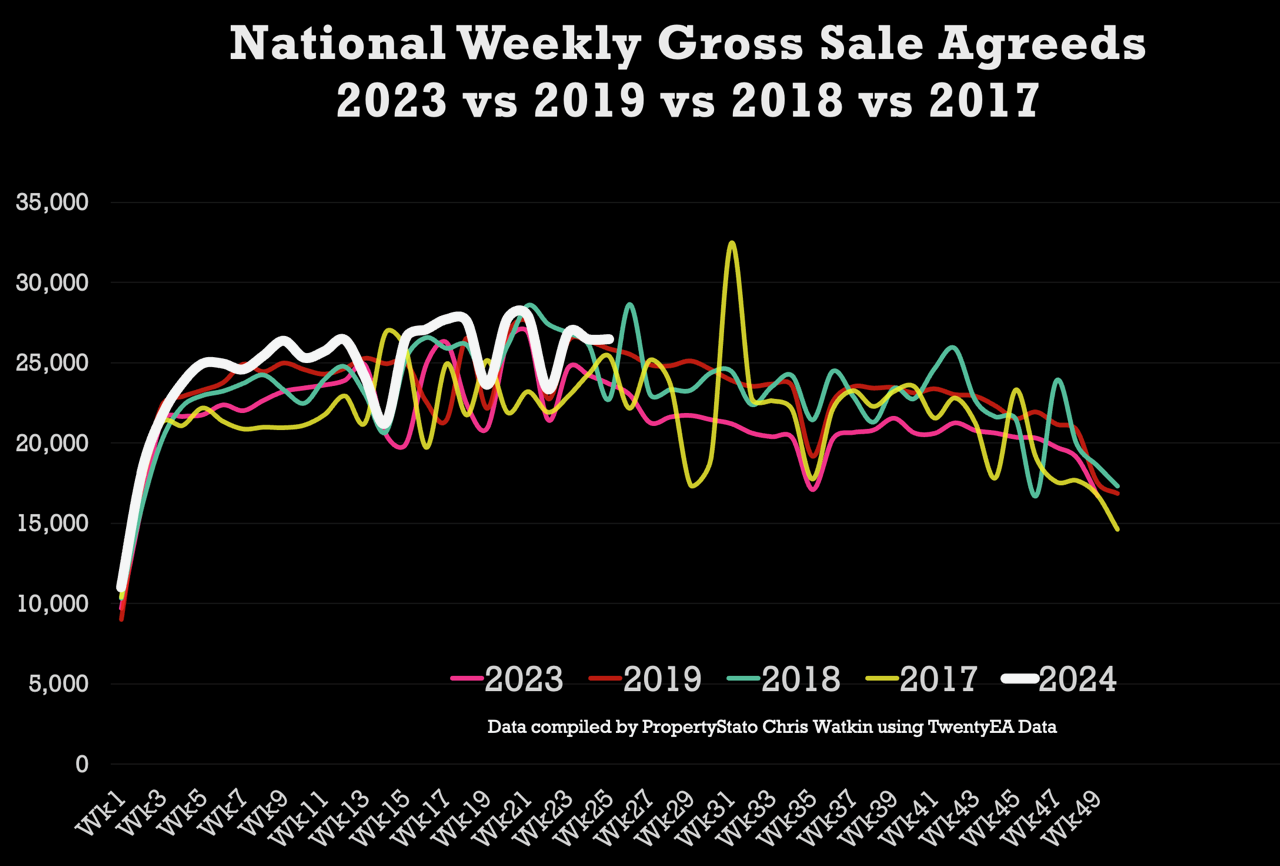

Gross Sales: 26,472 properties were sold stc last week (2024 weekly average : 24,600 Gross Sales).

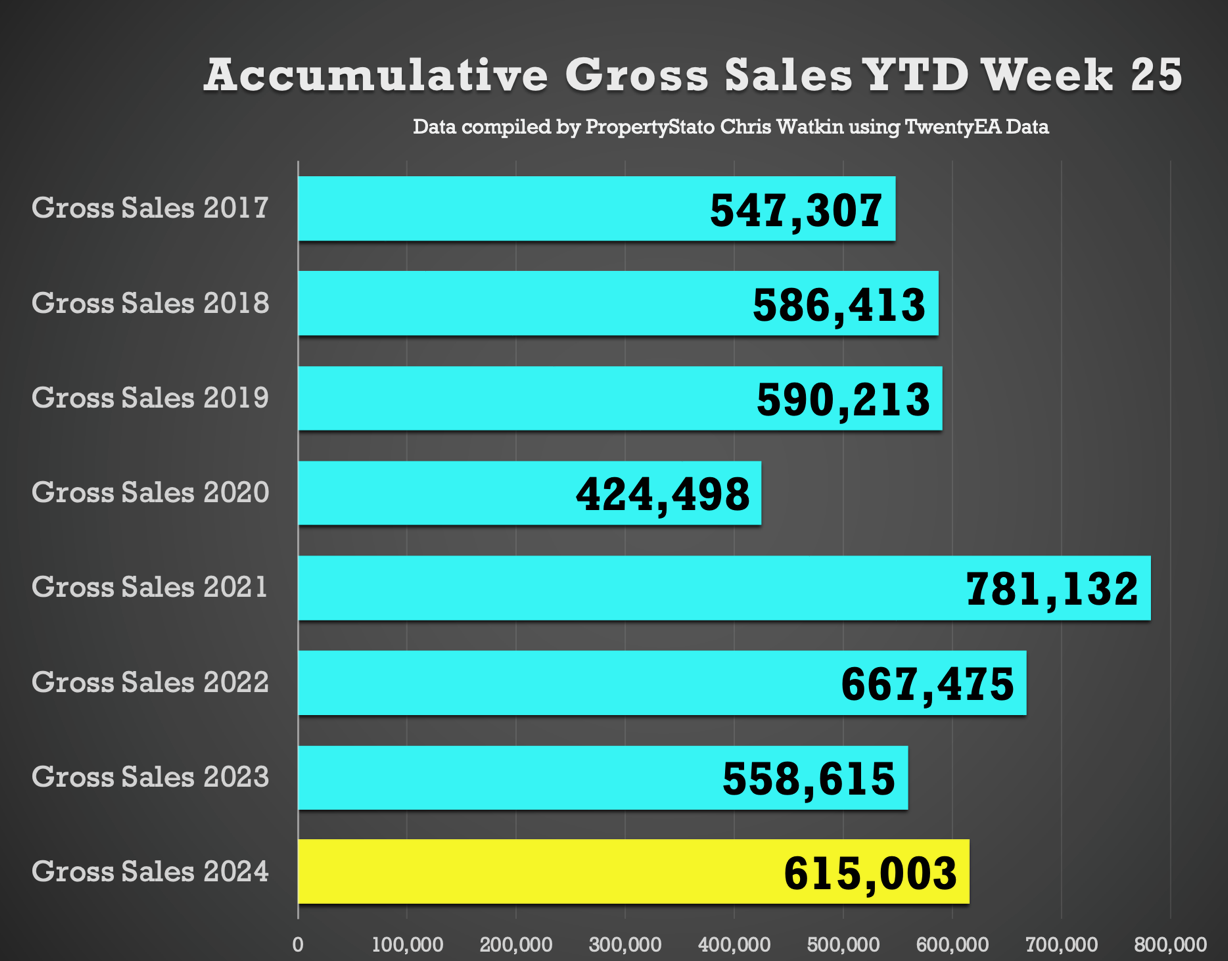

Accumulative Gross Sales YTD: The total YTD stands at 615,003, exceeding the average YTD Gross sales figure of 574,644 from 2017/18/19 and 558,615 in the same week 25 in 2023.

Average Asking Price of Sold STC Properties: Still staying in the mid £360/380k’s range (like has been for 2 years) at £373,313.

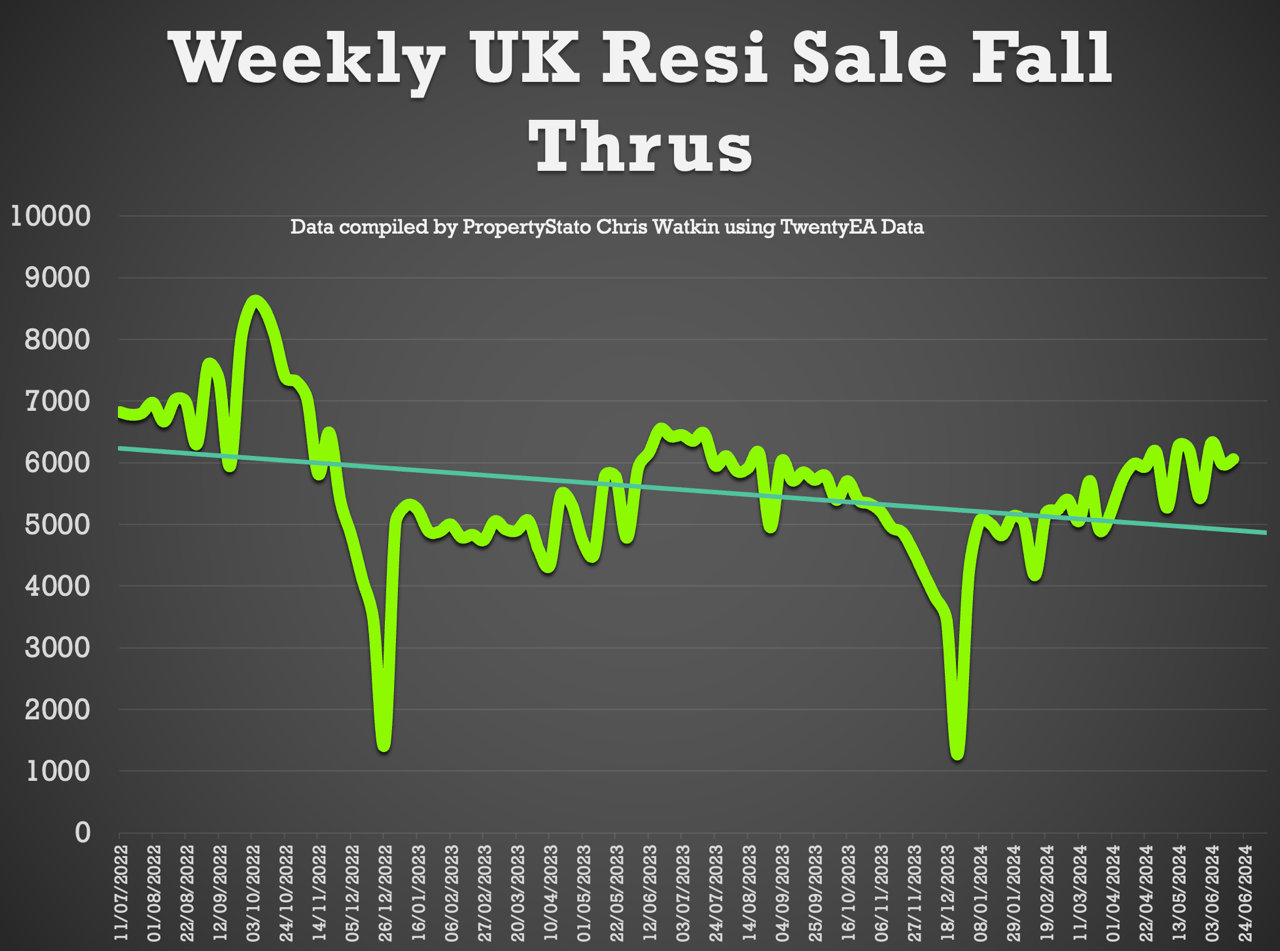

Sale Fall Throughs: Fall throughs this week at 6,055. Last 2 months weekly average 5,958.

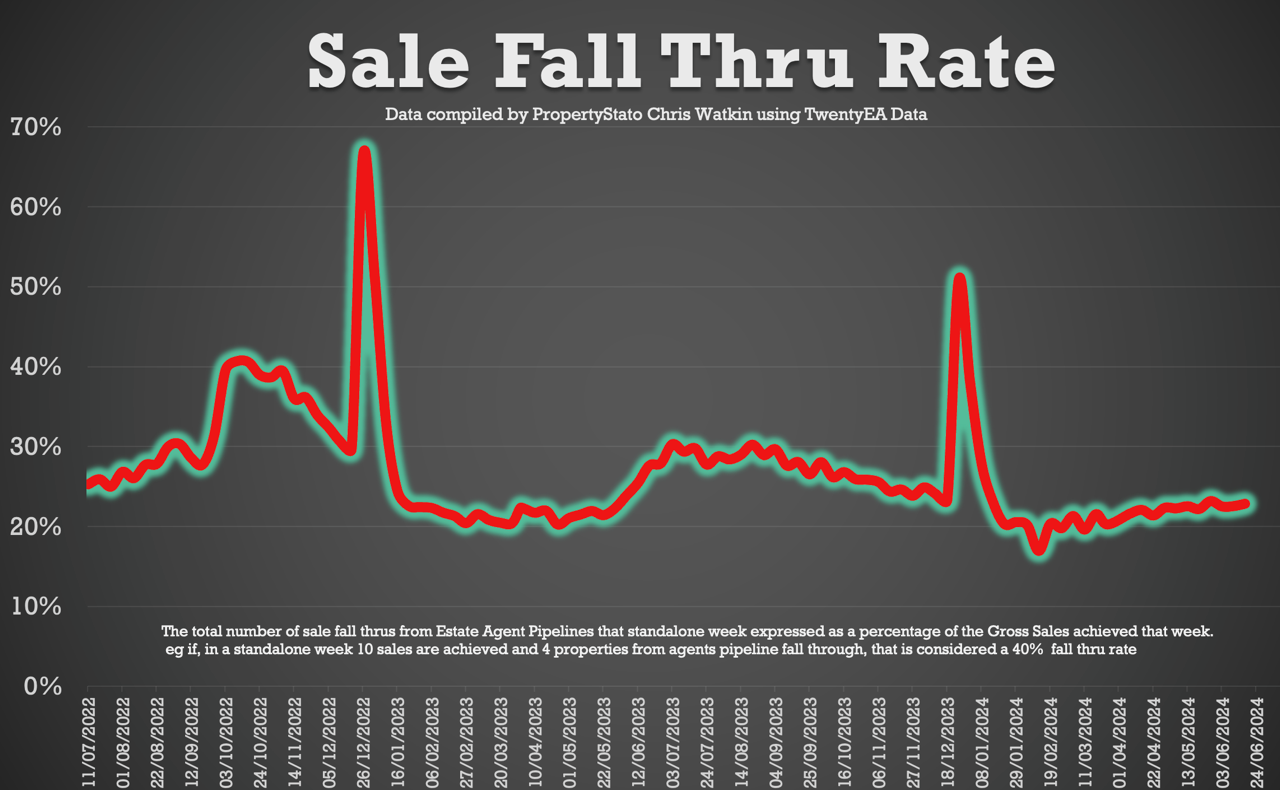

Sale Fall Through % Rate: Similar to last week at 22.9% for week 25. (Comparison – 22.6% for the last 2 months, whilst the long term 8 years average is 24.8% & it was 40%+ in Q4 2022 – the Truss budget!).

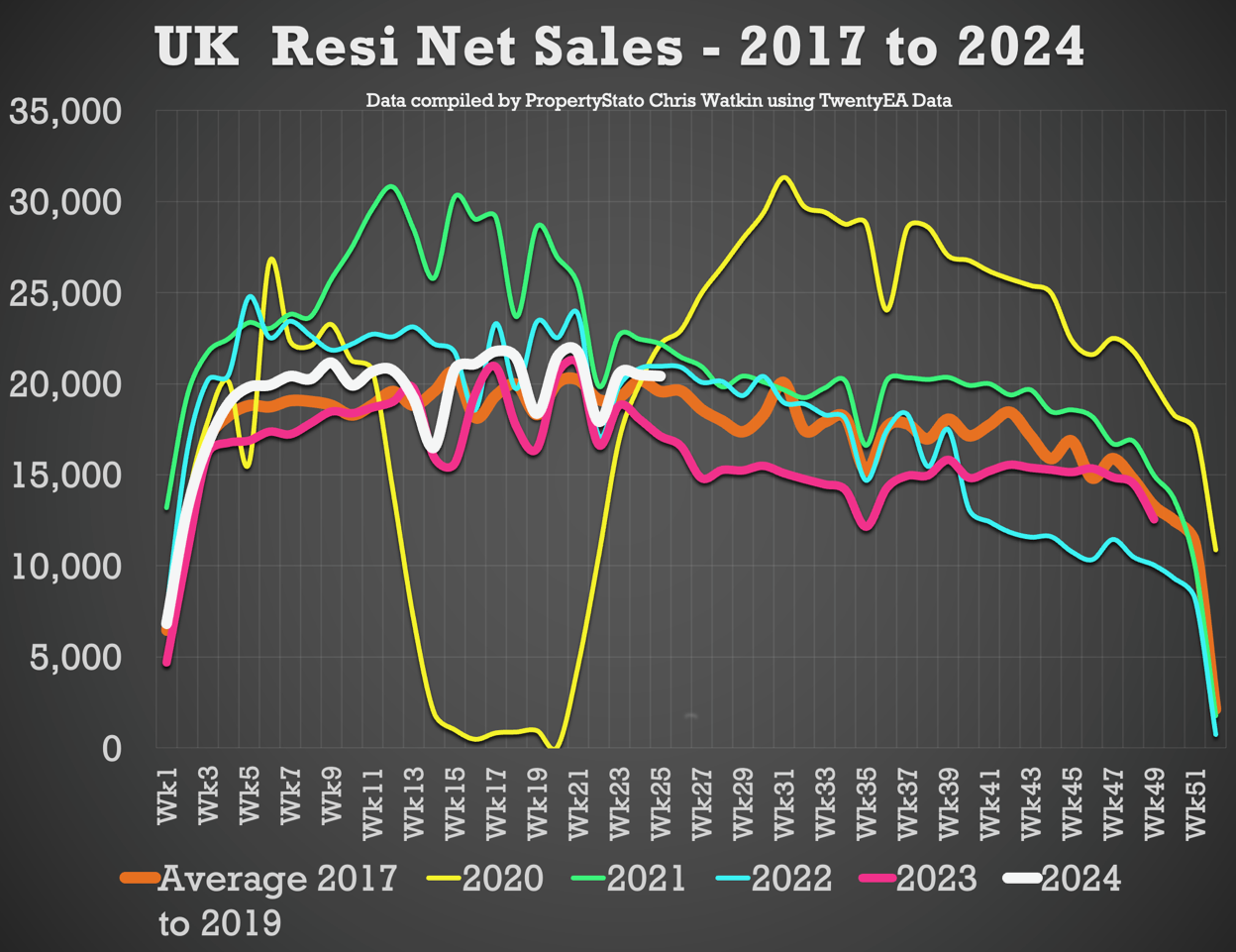

Net Sales – 20,417 – 6.3% higher than the 2024 weekly average of 19,204.

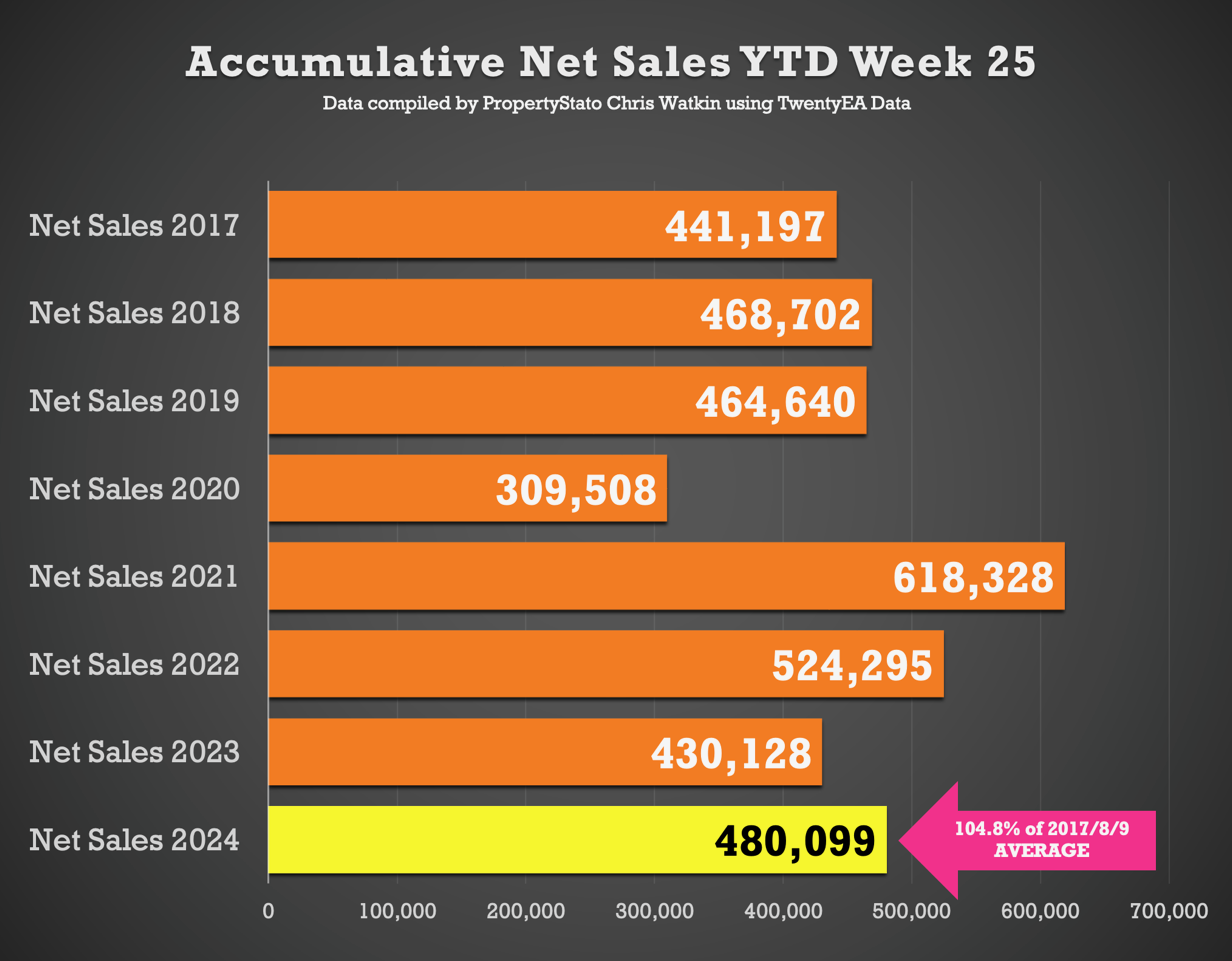

Accumulative Net Sales YTD: The total stands at 480,099, 4.8% higher the 17/18/19 YTD Net sales average (458,180) and 11.6% higher than the YTD figure for 2023 for Net Sales

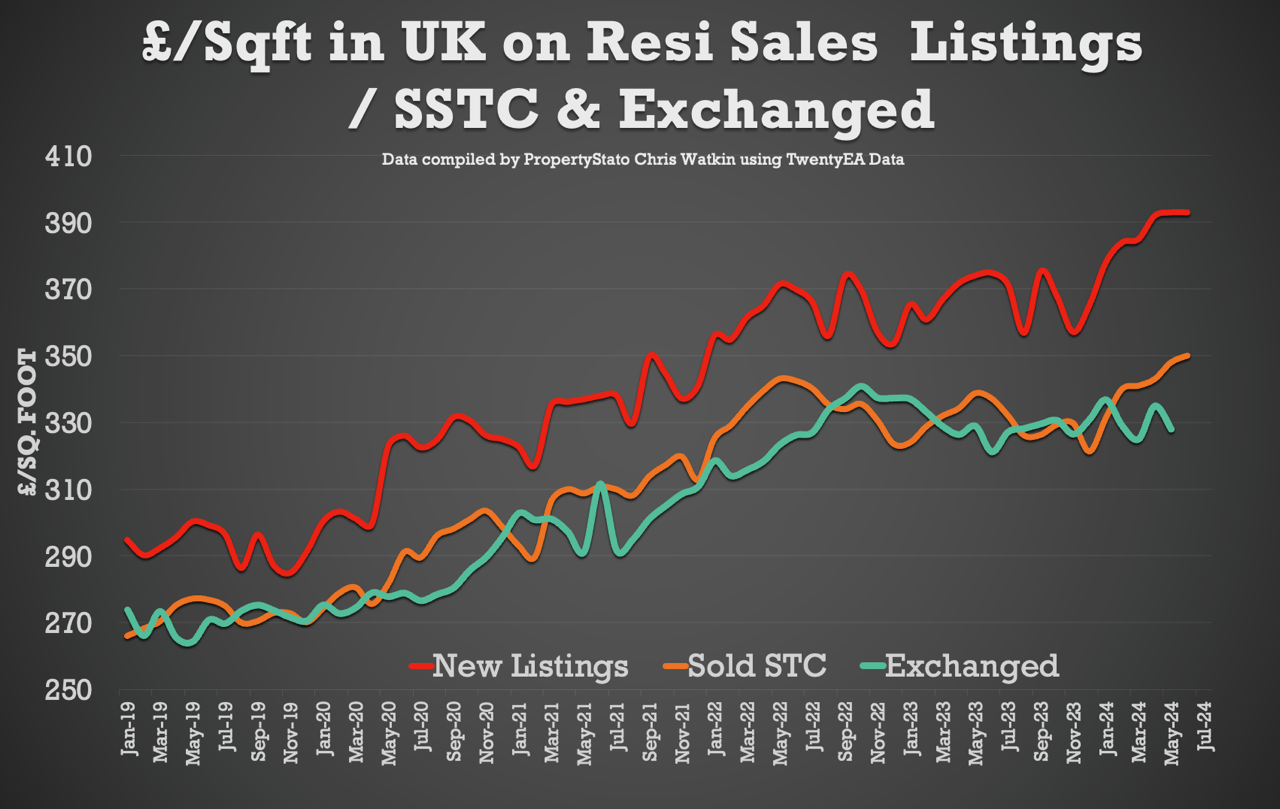

House Prices for June MTD are still at £350/sq.ft. For comparison – in May ’24 in £348/sq.ft, April ’24 – £344/sq.ft, March ’24 – £339/sq.ft, Feb ’24 -£339/sq.ft & Jan ’24 to £331/sq.ft).

Nationwide Real Values today versus Q2 2022- the average UK home is 14.52% cheaper in real terms today than Q2 2022 – Figures from the Nationwide Building Society

Resi Sales Stock Levels – 694,281 properties for sale at the end of May 2024.

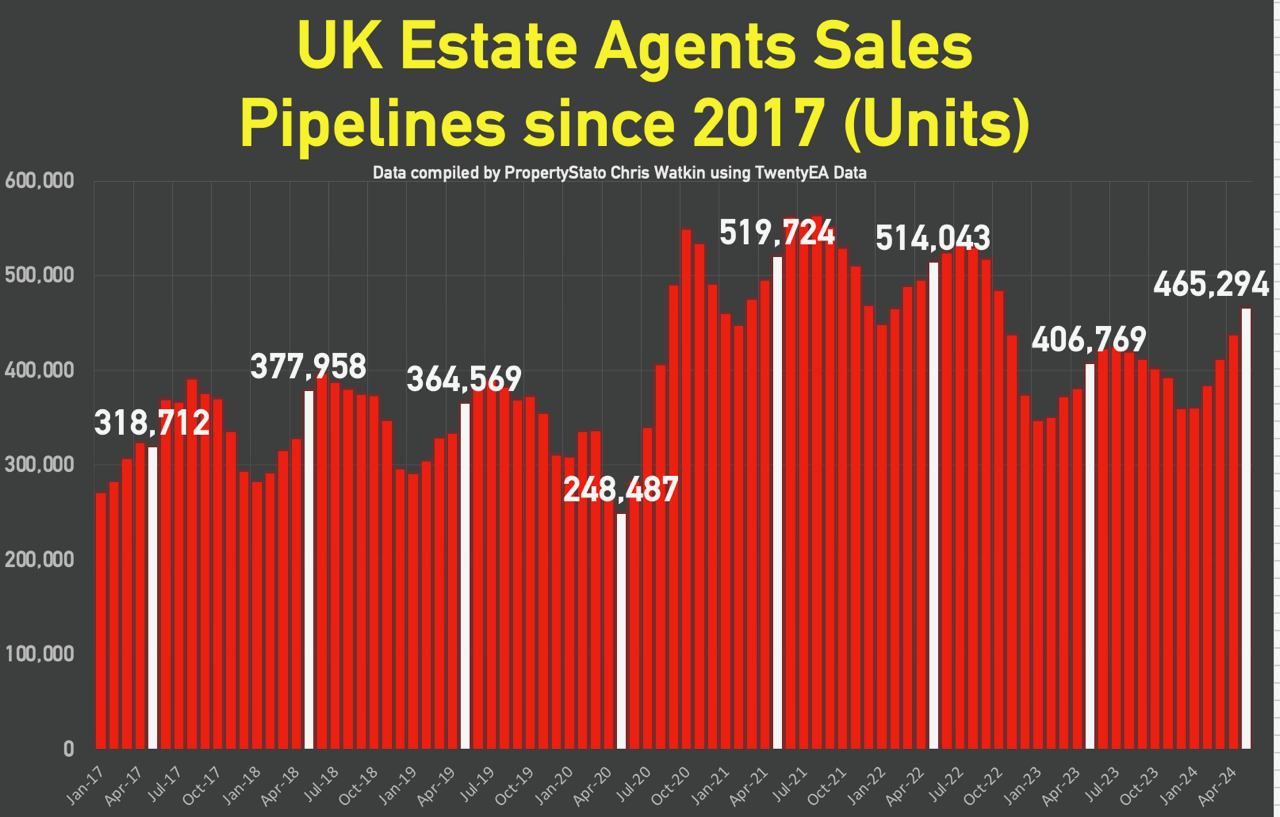

Resi sales in Sales Pipelines – 465,294 properties in Agent’s Sales pipelines at the end of May 2024.

This week’s local focus is on Hatfield.

Comments are closed.