This week’s UK Property Market Stats Show, for the week ending Sunday 2nd June 2024, features James Forrester, and the headlines are as follows:

This week’s UK Property Market Stats Show, for the week ending Sunday 2nd June 2024, features James Forrester, and the headlines are as follows:

+ House prices are 5.1% higher than Dec 2023

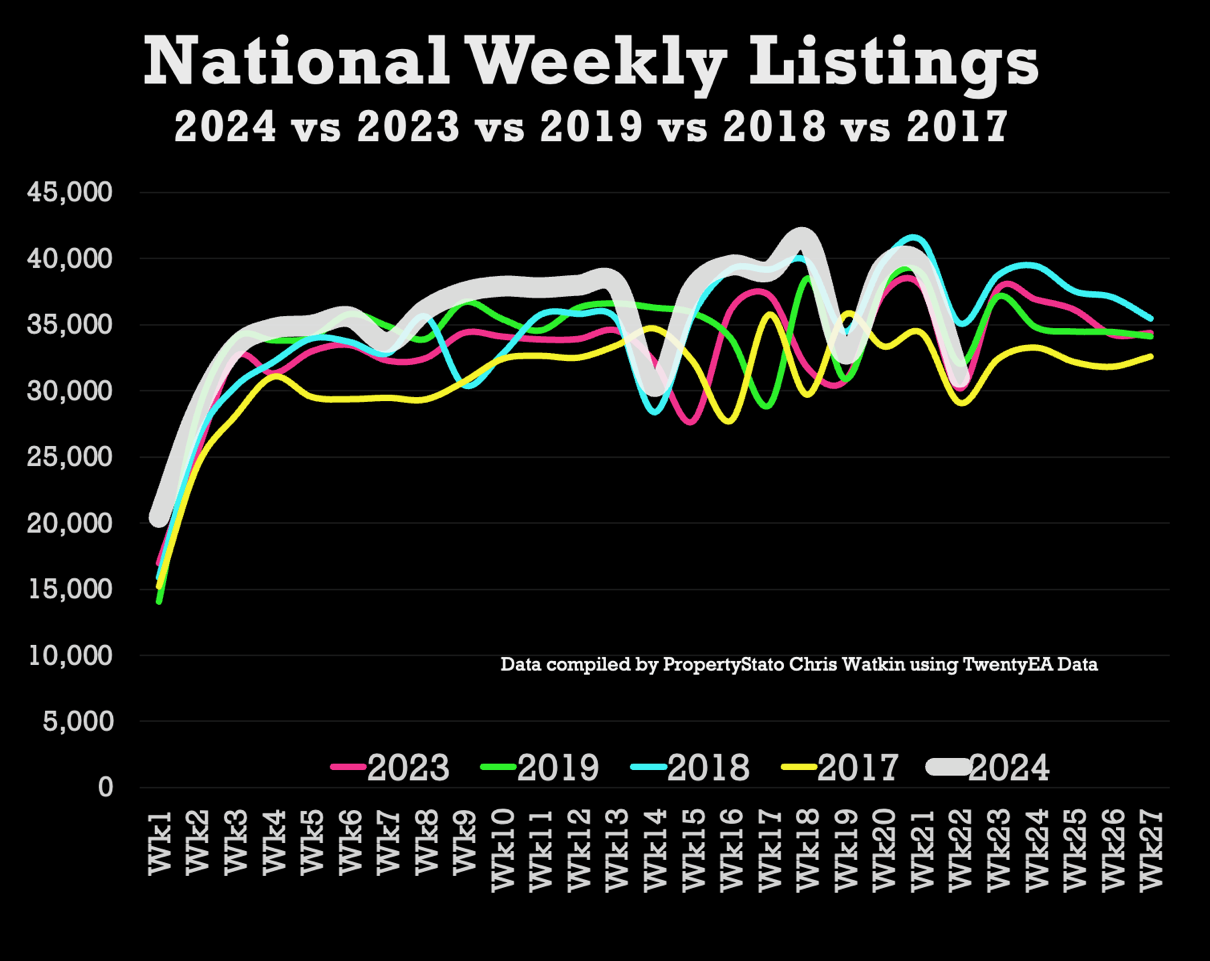

+ Listings – 21% lower than last week (as predicted) at 31k UK listings. YTD 9.6% higher than 2023 and 8% higher YTD than 2017/18/19

+ Total Gross Sales – 23,347 (21,417 same week in 2023). YTD Gross sales are 10.1% higher than 2023 YTD levels and 7.3% higher than 2017/18/19 levels.

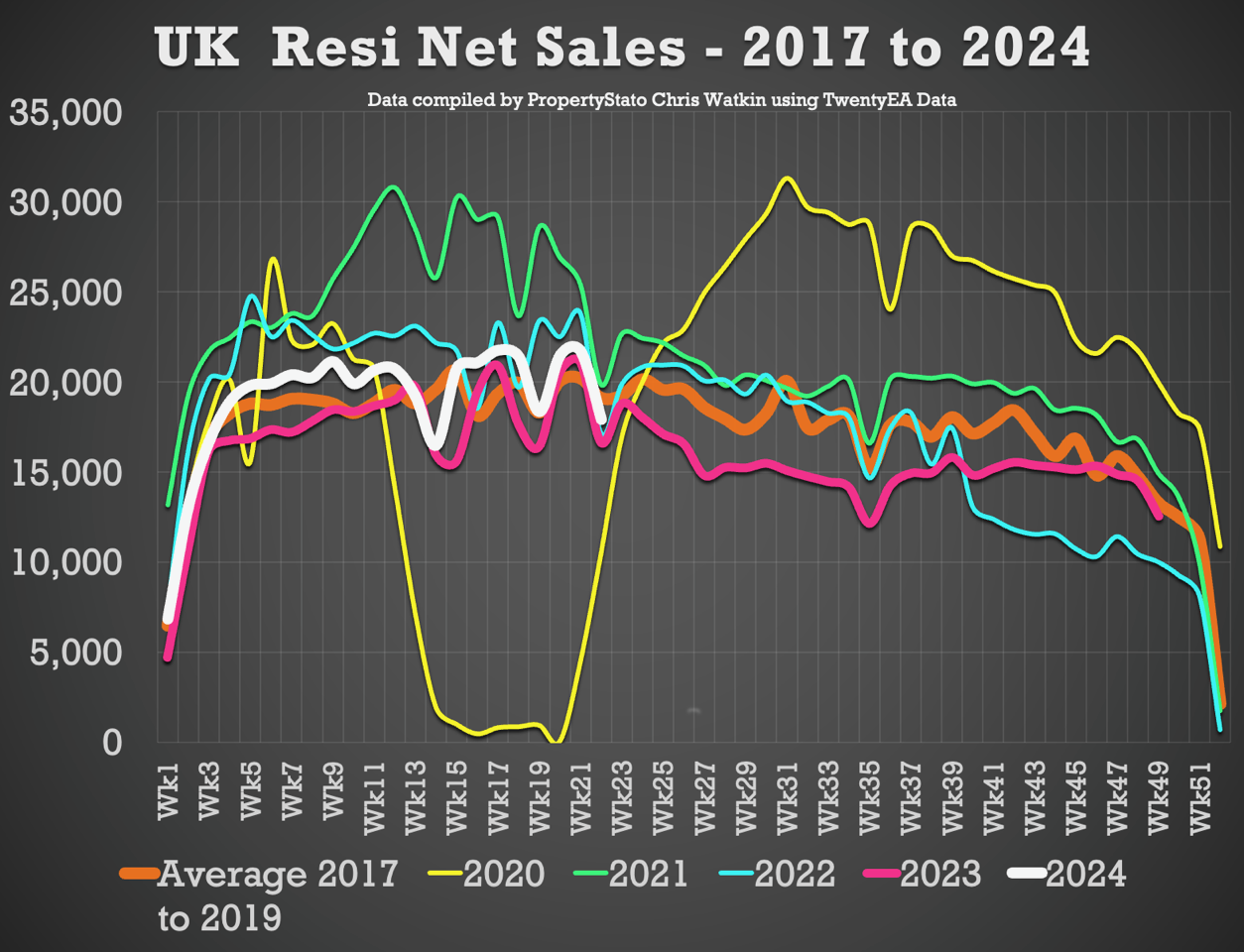

+ Net Sales – 17,927, a dip from last week because of the Bank Holiday. Average for 20/21/22/23 was 16,040, so not bad at all.

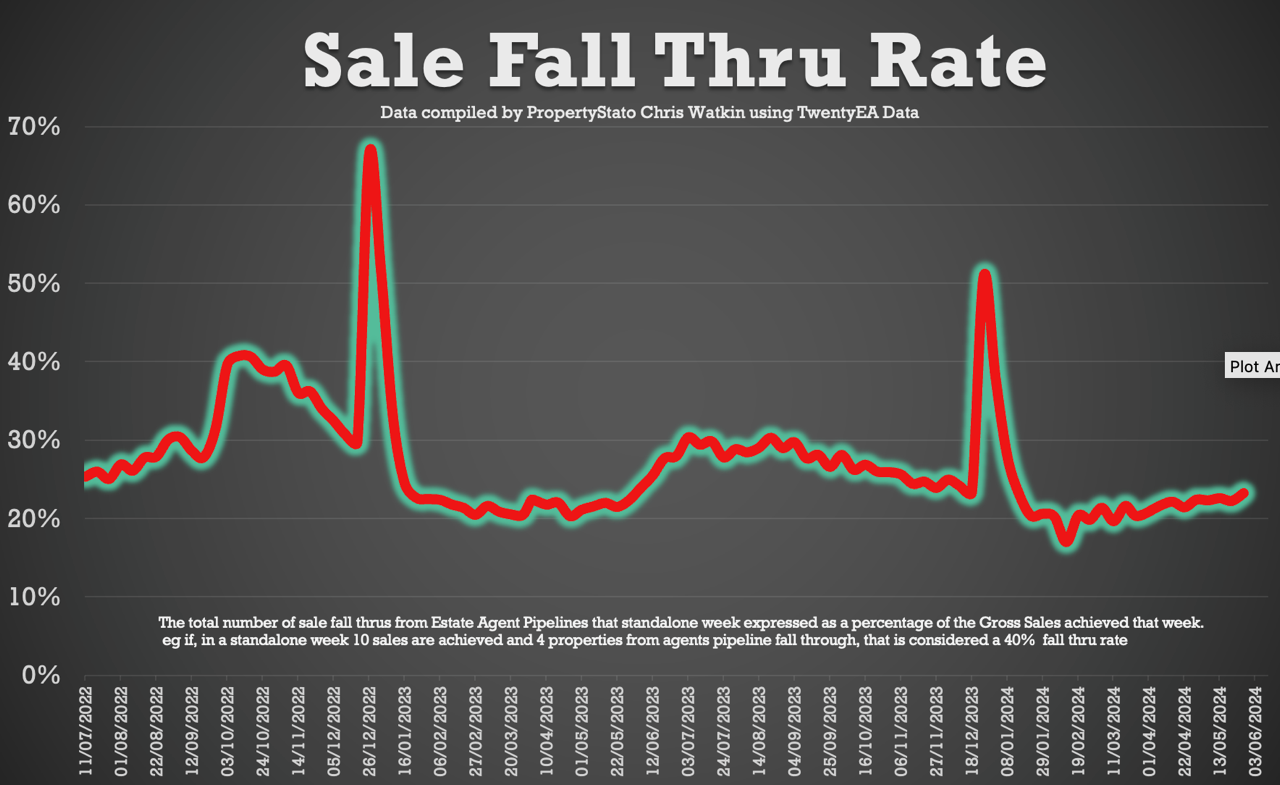

+ Sale fall-throughs remains steady at just over 1 in 5 sales.

Chris’s In-Depth Analysis (Week 22) :

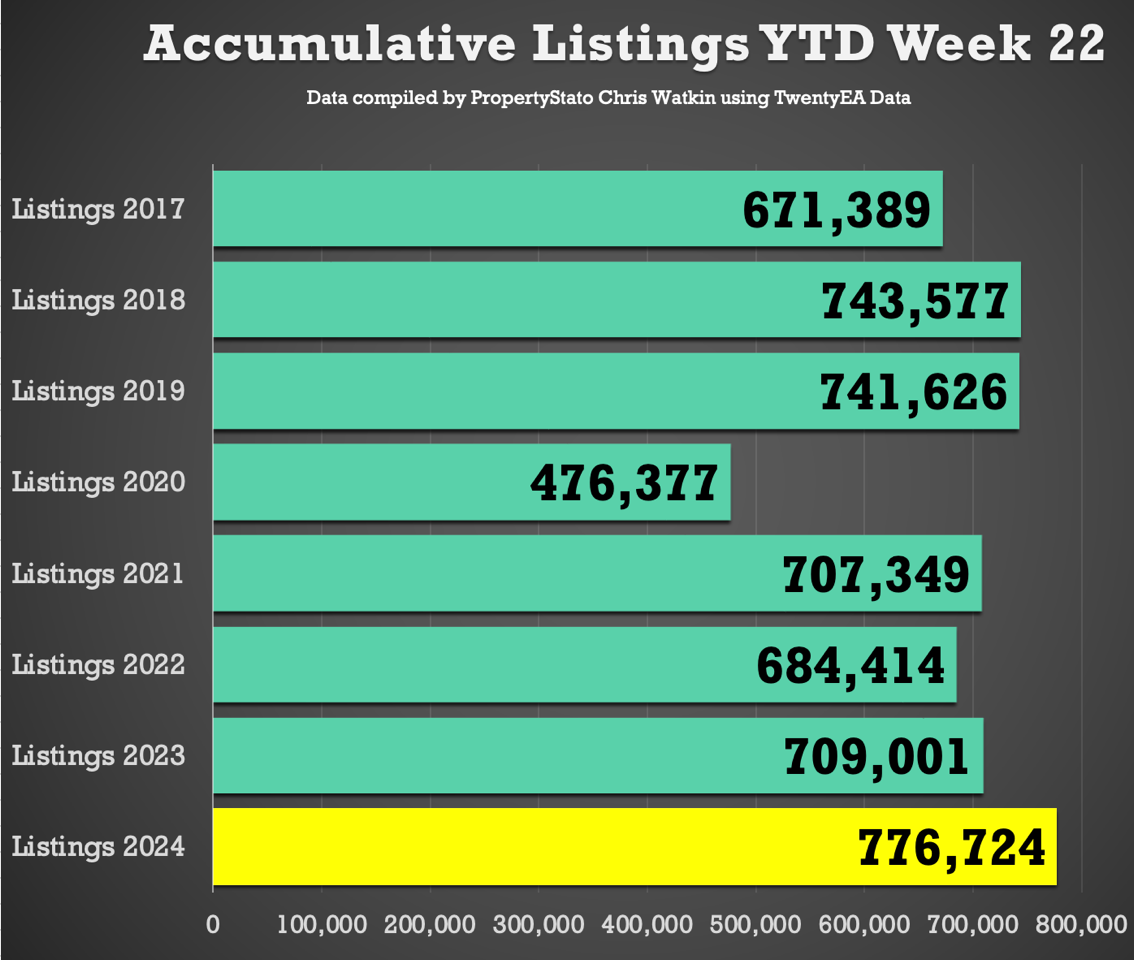

+ New Properties to Market: The UK saw 31,010 new listings. This year’s YTD listings stand at 776,724, 12.8% higher than the historical 8 year YTD average of 688,807, 8% higher than YTD 2017/18/19 and 9.6% higher YTD 2023. Graph 1 Graph 2

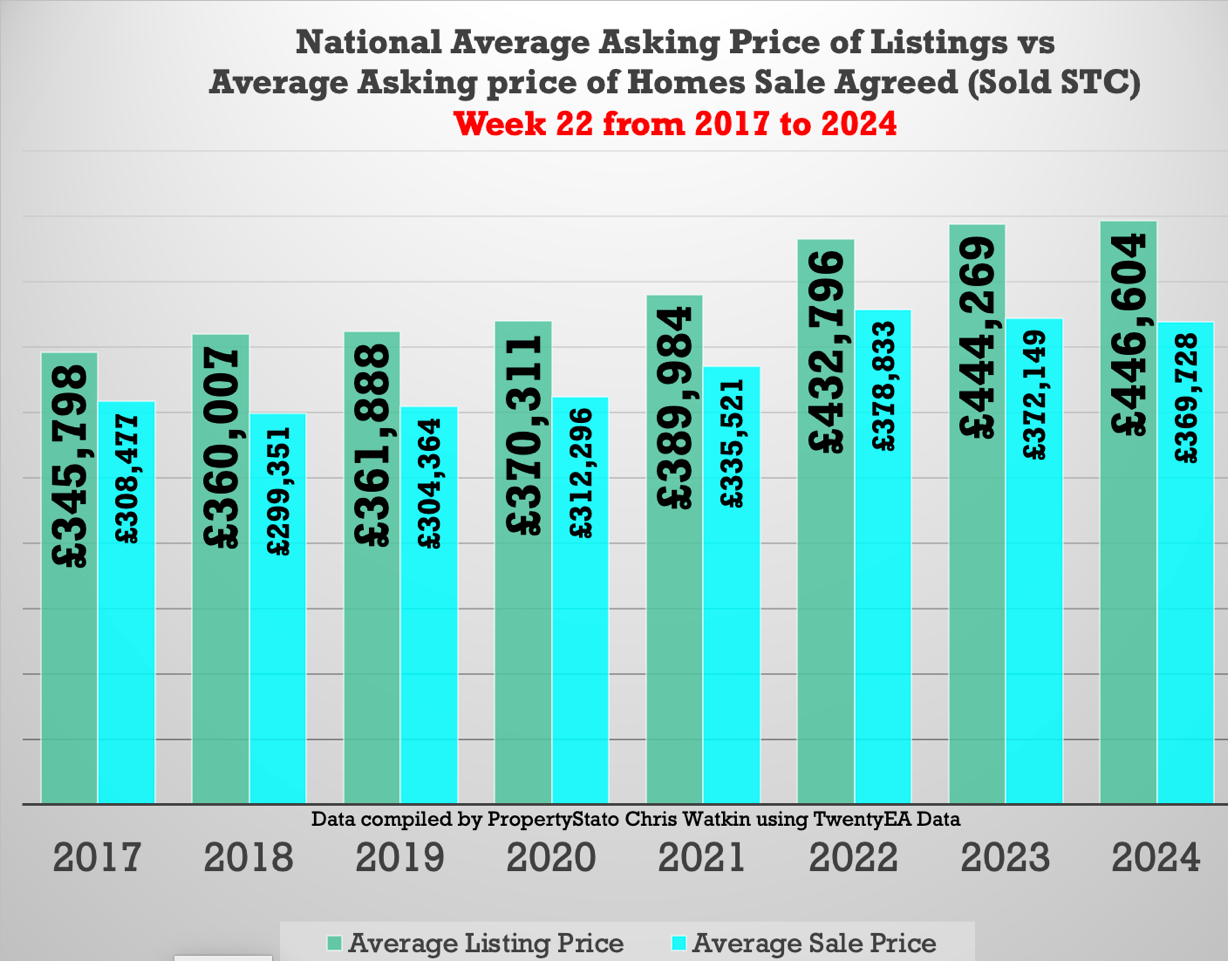

+ Average Listing Price: £446,604.

+ Average Asking Price of this week’s Listings vs Average Asking Price of the Properties that Sale Agreed this week: 20.8%. The long-term average is between 16% and 17%. Over valuing in the whole of the UK, higher valuing properties for sale (downsizing) and a lower propensity of London & SE properties to sell causing this.

+ Price Reductions: Last week, 18,791 properties saw price reductions, a significant number compared to the 8-year Week 18 average of 13,510. This means 1 in 7.89 properties each month are being reduced (Long term average 1 in 9.9 per month)

+ Average Asking Price for Reduced Properties: £407,521

+ Gross Sales: 23,347 properties were sold STC last week.

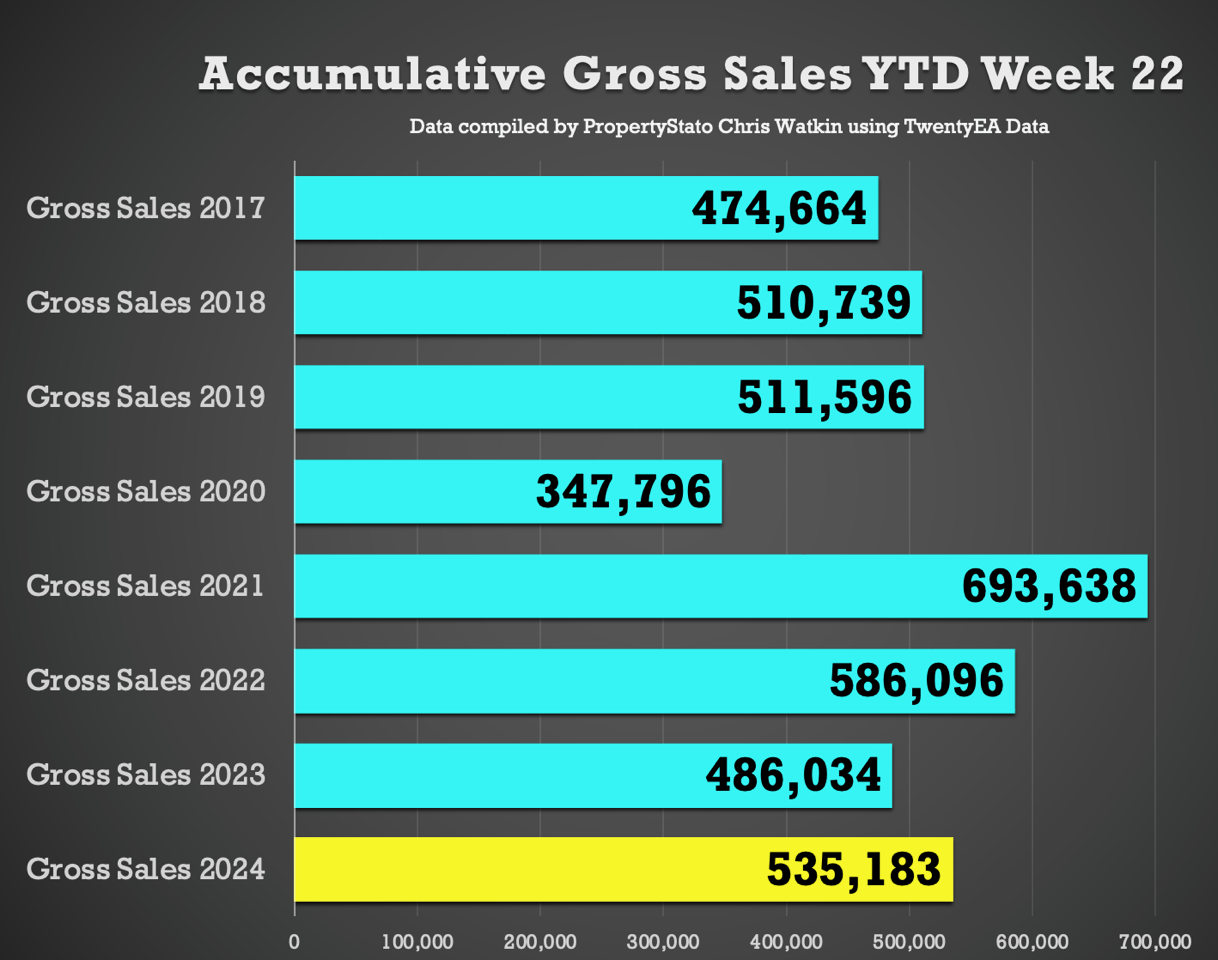

+ Accumulative Gross Sales YTD: The total stands at 535,183, exceeding the average of 499,001 from 17/18/19 and 486,034 in the same week 22 in 2023.

+ Average Asking Price of Sold STC Properties: Still staying in the mid £360/370k’s range at £369,728.

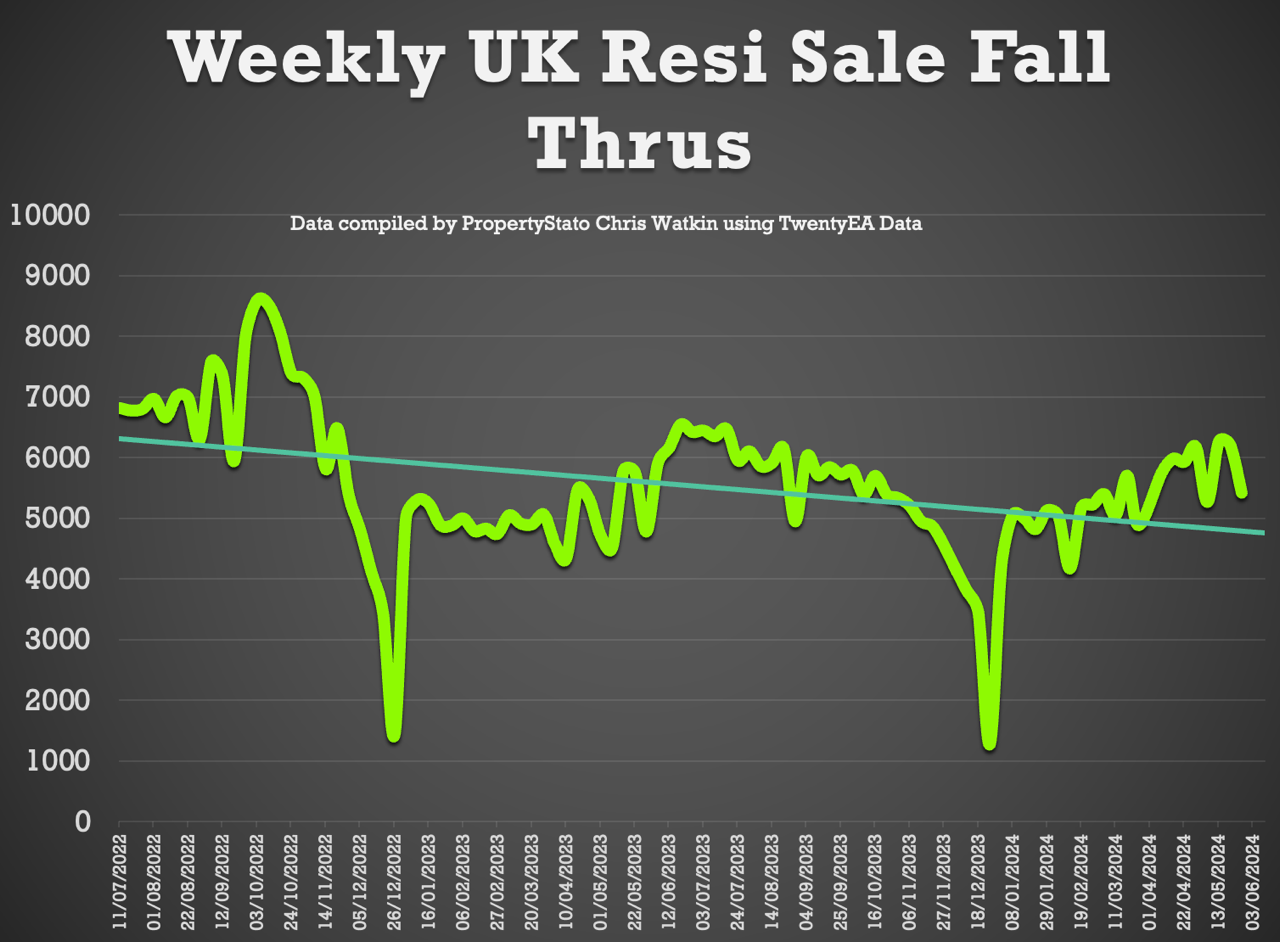

+ Sale Fall Throughs: Significant drop in fall throughs at 5,420 (yet that is because of the Bank Holiday). For comparison, 5,298 YTD ’24 average weekly figure (& 7,590 weekly sale fall throughs in two months after Truss Budget in Q4 2022)

+ Sale Fall Through Rate: Slight increase to figures seen in the last few months, to 23.2% for the week (Comparison – 21.76% for the last 3 months, whilst the long term 8 years average is 24.8% & it was 40%+ in Q4 2022).

+ Net Sales – at 17,927. YTD ’24 average 19,208.

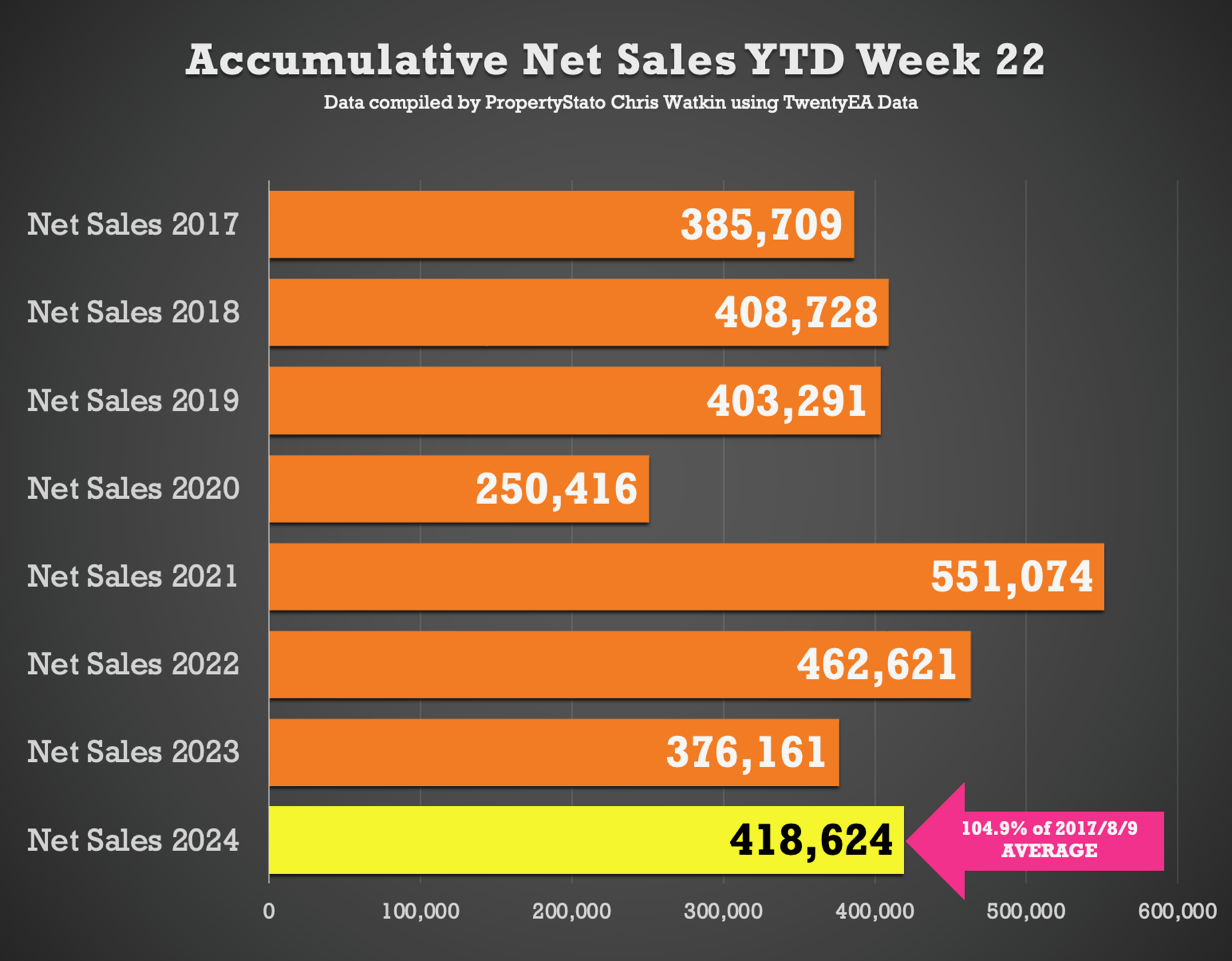

+ Accumulative Net Sales YTD: The total stands at 418,624, 4.9% higher the 17/18/19 YTD Net sales average (399,243) and 11.3% higher than the YTD figure for 2023 for Net Sales (2023 YTD : 376,161).

+ House Prices for the week achieved £347/sq.ft. Almost identical to £348/sq.ft in May ’24 (April ’24 – £344/sq.ft, March ’24 & Feb ’24 both at £339/sq.ft & Jan ’24 to £331/sq.ft). House prices are 5.1% higher than Dec 2023 (although some regional differences). Graph 24

This week’s local focus is on Islington (N1)

Comments are closed.