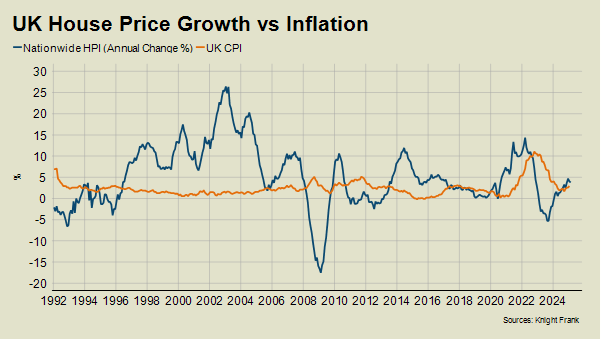

Knight Frank has released its latest analysis on the UK residential property market, reflecting on the impact that UK inflation, which exceeded the annual rate of house price growth between September 2022 and June 2024, has had on the sector.

The change in the Consumer Price Index (CPI) peaked at 11.1% in October 2022, while the Nationwide and Halifax indices were largely flat or falling during the 20-month period, bottoming out at -5.3% and -4.3%, respectively, in Q3 2023.

Buyers and sellers are unlikely to experience similar choppy waters in 2025, but they are certainly swimming against a gentle and unpredictable current, according to Knight Frank’s Tom Bill.

UK inflation rose unexpectedly to 3% this month, while house prices are edging in the opposite direction. The Halifax index narrowed from 4.7% in November to 3% in January, while the Nationwide recorded a 3.9% increase last Friday, down from 4.7% in December.

Bill, Knight Frank’s head of UK residential research at Knight Frank, said: “When you consider that demand is being temporarily supported by April’s stamp duty increase, it wouldn’t be a surprise to see the two lines on the chart below cross over again.

“Not that inflation exceeding house price growth is necessarily a bad sign. However, in addition to the post-Covid period, it happened during the global financial crisis, a period that was marked by austerity and the eurozone crisis in the first half of the last decade and during the UK recession of the early 1990s.

“Dramatic movements are unlikely this time, with the housing market showing signs of strength after the rise in mortgage rates that followed October’s Budget.

“Furthermore, transactions and mortgage approvals in December were only marginally below the five-year average.”

Bill points to the fact that the early-January jitters ahead of Donald Trump’s inauguration due to the inflationary risks of tariffs have also subsided, “though not disappeared”. Indeed, global financial markets generally spent February in risk-averse mode, as the price of safe-haven assets like gold rose strongly.

He explained: “The five-year SONIA swap rate, which is used to price fixed-rate mortgages of the same length, fell to 4.1% last Thursday from close to 4.4% in mid-January. The two-year rate has fallen below 4% over the same period, leading to the appearance of more mortgage rates starting with a ‘3’.

“Overall, supply has been stronger than demand so far in 2025 due to a similar risk-averse attitude among some buyers. However, the current sweet spot is equity-rich, needs-driven buyers.

“The question now is whether the spring market will blossom in the normal way.

“On the one hand, inflationary pressures that include higher employer national insurance contributions and minimum wage costs are on the horizon.

“On the other, the Bank of England appears increasingly comfortable with going beyond its primary remit of containing inflation to support economic growth.”

Last week, the government re-appointed Swati Dhingra as an external member of the monetary policy committee, who has previously advocated for more substantial rate cuts.

Bill believes that is good news for homebuyers provided inflation also stays relatively close to the Bank’s 2% target.

He added: “The uncertain outlook means the spring statement on 26 March will be a key opportunity for the Chancellor to set the tone for 2025.

“Creating more financial headroom will alleviate the upwards pressure on borrowing costs, which will be good for housing demand. Provided it’s not done by raising taxes that simultaneously dampen buyer appetite.

“House price growth and CPI are not expected to be very far apart at the end of the year. The latest ONS inflation forecast (which may rise alongside this month’s spring statement) is an average of 2.6% during 2025, while we expect UK house prices to increase by 2.5%.

“If both figures started with a ‘2’ at the end of the year, it would be reassuringly unexciting.”

Uk housing market is *****.

#balance

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Knight Frank’s analysis offers an interesting perspective on the UK housing market. Although inflation is a prominent topic, the housing market seems to be thriving, with mortgage approvals and transactions remaining consistent. The prevailing conditions benefit equity-rich, need-based buyers, but the true measure will be how the spring market unfolds. There’s potential for interest rate cuts to offer a lift, though still-high employer costs and inflationary pressures could weigh on gains. It’s good to see house price growth moving in line with inflation forecasts and paving the way to a more balanced market. How do you think government policies in the next spring statement will impact housing demand and affordability?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register