The way in which tenants are referenced in the UK is broken, according to the boss of a start-up offering “tenants’ passports”.

Peter Ramsey, founder of Movem, claimed that the public was unaware of how the system is broken “or don’t care that the result of the existing process is worthless”.

He also highlighted how the cost of reference checks was inflated first by reference companies, who can produce them at a cost of “pence” and then letting agents as they both upsold them.

He asserted that reference checks were often flimsy because companies aren’t incentivised to make them “bullet-proof”.

In an article in Medium, he said: “Referencing companies wouldn’t want a 100% success rate of filtering out bad tenants, or they’d never sell their insurance.”

He added: “You need to know that a tenant reference, right now, isn’t a ‘complete know your tenant’ check at all.

“It’s more of a ‘yeah, based on these factors they haven’t screwed up so far, but really we have no idea what they’ll be like, so buy our insurance just in case’ check.”

And he cited examples of how flawed the checks were, how companies often just took the information provided to them at face value, and how easily it could be manipulated using computer software.

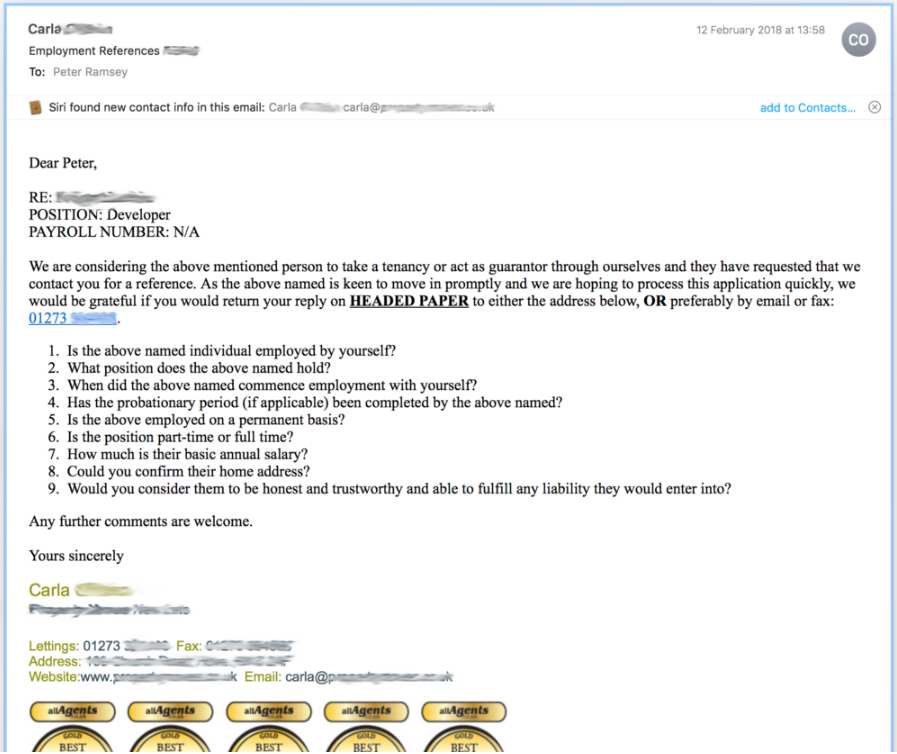

Ramsey used, among others, the example of a reference request from an unnamed, award-winning letting agency he received in relation to one of his own employers.

It asked questions about whether or not he employed the individual, when they started employment, requested details of their salary, and asked if they were honest and trustworthy.

Ramsey said he replied but added that his replies were effectively worthless.

He said: “As far as they’re concerned, they’ve verified that Paul is employed. But they haven’t, have they? All they’ve done is get a response from the email account Paul said was his employer.

“Whilst at university I knew somebody who gave his own mobile number as his employer, said he was on £40k a year, replied to the email himself posing as his employer, and passed.”

Of course, Ramsey has his own service to promote and suggested that Movem could help fix the system he claims is broken.

He said: “At Movem, we’ve created the first instant tenant reference that verifies income and previous rental payments directly with the applicant’s bank, using data provided by Open Banking.

“I have no doubt that in five years the vast majority of tenants will be referenced in this way, and rental decisions will be made based on the access and interpretation of raw data.

“The call centres will be empty.”

Mr Ramsey needs to spend the day in our operation, sit with a processor and see what they do and how they do it. Clearly clueless and has no understanding of the tenant vetting industry.

Open banking is a good idea, although it’s not the panacea to tenant screening-just another piece of software that assist the people who do the hard work behind the scenes. Relying on Open Banking is dangerous and promoting this as a complete screening service is very ridiculous.

A thin article, pluggy at best and designed to promote his own services.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Hello UKTenantData,

Although I’m unsurprised that your opinion is strongly in favour of the current system, and I’m unlikely to ever change that, I have spent nearly two years obsessively learning about tenant referencing, from some of the largest referencing companies in the UK. I’ve sat and watched over their shoulders as they conduct references. I’ve used their internal software, and talked to everyone from those who phone employers, to the CEO.

You may not agree with me, but it’s not true to say I don’t understand the industry. Plus, industries change. Someone who understood how credit lending companies worked in the 70s may not understand how complex machine-driven lending decisions are made today.

If you think I’m wrong, then please, respond to the points I highlight in that article. I think it’d make great reading, and hey, you might prove me wrong.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Peter

Good morning, a couple of questions if I may:

1. How does your system work with Non UK applicants who don’t have a UK Bank Account?

2. Open Banking I believe is all dependent on an applicant giving you consent to access their bank account. What happens if you do not obtain this consent?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Morning Fudge, Of course, let’s get into this:_____1. You can use Non UK banks in exactly the same way you use UK banks.2. Of course, it’s dependent on tenants authorising access. If they do not wish to do this, they can upload bank statements / payslips in the traditional fashion. We strongly advise against this, for the reasons I highlight in that article, and we make it clear to the agency that it’s less safe._____Best regards

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

You idiots at UKtenantdata don’t even know how to read bank statements properly, FYI when you see ‘FX’ on the bank statement, this is a foreign currency transaction lol…

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I was using (what I believe) was the very first referencing product to arrive in the lettings arena, back in 1991. MARAS launched by Graham Sandley and his father was based on a US model of credit scoring. Up until that point agents and landlords could expect to lose 5% of rent through arrears, because all we had was a written employers reference (or pay slips) and a letter from the bank (can anyone else remember writing to local bank branches for references?). MARAS dropped our default rate to 2% overnight. As referencing processes have become ever more sophisticated the default rate has fallen much further – below 1% ten years ago and with modern referencing companies such as The Lettings Hub, the default rate is vanishingly small, probably around 0.2%. That is why you see Rent Guarantee products with nil excess, 6-months rent and full legal expenses for around an annual fee of £120 incl. IPT. These products represent phenomenal value, and its made possible because (not in spite of) the quality of credit checking available in the market.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Hi ChumpExecutive,

This is genuinely a great anecdote, and a brilliant example of how technology changes archaic systems. Even when people thought those systems worked well in the first place.

To clarify, my point isn’t that referencing isn’t better now than it was in 1991, but we now have new tools at our disposal to make that 0.2%, 0.1%, and so forth.

I’m not suggesting credit checking is sub-standard either. We (Movem) plug into credit reference agencies, like any referencing company. Specifically, the bit we’re replacing is human labour with machine-learning.

To put it another way: even if you’re not interested in an increase of accuracy, say 0.2% going to 0.1%, you’d be interested in reaching 0.2% cheaper and faster, right? What cost £120 and took 2 days could cost £80 and take 60 seconds.

And in 2 years time there will be some new company claiming they’ve found a way to bring that down to £70, and 45 seconds. When that happens I hope somebody screenshots this and posts it.

Happy to chat about this more. If you disagree with any of my points in that article, please, call me out.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Peter Ramsey you are clueless and your article is disingenuous. You have not spent any time with me or my team. We have 136 team members serving some 2000 professional letting agents. Let Alliance guarantees annual rents in excess of £500,000.00. This would be impossible without top quality, investigative tenant referencing. Fraud is on the increase, our role is to identify fraudulent applicants on behalf of our letting agent partners. From time to time we make mistakes, we have a 100% track record of fixing them, our customers are never left out of pocket. We use Open Banking, it does help, it is not the total answer, many banks do not have this facility available. Come back when you have grown up and have some experience and knowledge, it will be a while.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Hi Andy,

Thank you for your kind words, whilst I’m sure it’d be a pleasure to meet, I never suggested we had – so I’m unsure where that claim came from.

I’m also sure your team is quality, you’ve built a profitable business and I have to take my hat off to you. And I’m not highlighting LetAlliance as having any greater flaws than anybody else in this industry. My point is that the whole process is broken, everybody included.

Obviously, I expected the traditional referencing companies to come to this article to put it down, and I wouldn’t have posted it unless I was interested in a healthy debate.

So, let’s talk. Please, go through my article and point out where I’m wrong. I’m sure there are hundreds of agencies interested to see this play out, so let’s have an honest conversation here, for all to see.

Best regards

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I don’t have the time or inclination to talk to you.

Here are just a couple of points, playing back your comments and assertions;

I have spent nearly two years obsessively learning about tenant referencing, from some of the largest referencing companies in the UK. I’ve sat and watched over their shoulders as they conduct references. I’ve used their internal software, and talked to everyone from those who phone employers, to the CEO. Name them

He also highlighted how the cost of reference checks was inflated first by reference companies, who can produce them at a cost of “pence”. Produce your analysis and evidence of the cost of completing a comprehensive reference

He asserted that reference checks were often flimsy because companies aren’t incentivised to make them “bullet-proof”. Produce your analysis and evidence along with your understanding of how rent guarantee & legal expenses is underwritten Or……… just go away.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Hi Andy,

Have you actually read my original article, or just skimmed this PropertyIndustryEye article? I ask because all 3 of your points are about what’s on this page, and you’ve ignored the rest in it’s entireity.

You’re clearly passionate about defending the status quo – as expected. I mean, you’ve built a whole business on it.

Please, it’s only a 12 minute read, take the time to read the full thing and show me where I’m actually wrong. I show how easy it is to fraudlently reference yourself with traditional methods – point out how LetAlliance are different.

______

As for your questions:

– You know I can’t name who I’ve spoken to, come on.

– If you read my original article, you’ll see that my comment about it costing pence was for the credit check, where further work can’t be done (i.e students who earn no money). You will know how much your CRA lookup is, and if it’s anywhere near what you charge for your “Express Referencing” product, I’ll be amazed.

– I talk about this in the article. It’s a huge point that one could write a book on, and I haven’t. My point is this; if your tenant referencing was so accurate that nobody ever rented to a tenant that didn’t pay rent, would anybody buy your insurance products? Now, clearly it’s a fabricated scenario and you’d never achieve 100%, but let’s assume there was a 1/100,000 risk of it happening, would people bother buying your insurancre? Maybe. How about 1/1,000,000? Maybe not.

_____

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

OK, now go away, as I thought, you are clueless.

With regards to why professional letting agents advise their landlords to take up the protection of rent guarantee and legal, following the completion of a professional reference; perfectly good tenants get ill, have accidents and can’t work, get divorced, I could go on. Perhaps you have also mastered the art of referencing for future, unexpected life events…..

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

There’s a good point in there somewhere: insurance is for unforeseeable events, such as accidents.

You’re right, absolutely. But if that’s what insurance is for, and these events are completley unexpected, why bother referencing in the first place as a condition of insurance? Or do you offer rental insurance without first being referenced?

That’s like saying “you can buy flood insurance to protect yourself against unforeseeable flooding, but before you do that you have to pass this key stage 3 maths exam” – the two aren’t connected. Or are they?

If on the other hand, referencing can be used to minimise the risk of ‘bad tenants’, then we’re back to my original point, about how it’s not in your interest to make referencing a 100% filter.

If referencing was a 100% filter you’d no longer get the commision on your insurance policies.

Did you read my original article?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I would like to offer a more considered approach than Andy, who I can only think is suffering from Monday morning blues.

We have all received the Open Banking ‘pitch’ from our respective Credit Reference Agencies and it is not without it’s benefits , but not in my opinion as a complete alternative to the traditional referencing model.

My first question to you Peter would be – What will be your USP when we all decide to offer Open Banking as an alternative or compliment to our existing service?

In addition to the obvious gaps in the banking organisations who are currently represented mentioned by another poster, I would like to highlight the following:

1. Peter, you seem to be under the impression that we currently ask applicants to provide bank statements in order to prove their income. We only do this on very rare occasions.

2. The majority of Agents on behalf of their Landlords wish to know an Applicants position, start date and most importantly permanency of employment. How do you justify accepting an applicant based on historical salary details who lost their job a week ago.

3. Our statistics bear out that applicants who fail for a bad landlord reference do so because of behavioural or damage issues just as much as payment problems. How do you combat this? Serial sub letters and Cannabis growers all pay their rent on time.

4. A good percentage of the rental market is made up of graduates entering first time employment within the next month of them applying. Bank statements do not deal with this issue.

5. What do you do if an applicant flatly refuses you access to their bank statements whether it be through Open Banking or by sending them manually?

I don’t see any FCA authorisation and I thought this was a pre – requisite of using Open Banking.

Your whole Insurance argument has me a little baffled especially as you have an Endsleigh Logo on your Homepage and are making the claim that your referencing is sufficient for their Rental Guarantee products.

If referencing was a 100% filter then there would be no need for the following disclaimer on your website:

In particular, when referencing a tenant through Movem, Movem will not be liable to you for any direct, indirect or consequential damage whatsoever that may arise from a breach of contract, misrepresentation, negligence that may have occurred as a result of using our referencing Services. We can not, and do not give any warranties as to the accuracy, completeness or truthfulness of the information provided.

Movem cannot, and does not, ensure the validity, legality or accuracy of the Content contained in properties, listings, reviews, Passports, references, questions, answers and blogs.

Nevertheless I wish you well and welcome the competition it is after all what keeps us all moving forward.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Good afternoon,

Great points. Thank you for being professional here. I want a real debate, and happy to disagree.

To start with, our product is different to what the CRAs are offering, or at least what they’ve told me they’re offering. They’re working on many things, but their original product is that CRAs want to buy and sell data accumulated through Open Banking integrations.

For example, let’s say a company called MyMoneySpending helps users manage their spending. They might take data from users to provide a service (like suggest how to spend less on groceries), then sell it to CRAs, who in turn accumulate this data and sell it to referencing companies alongside a traditional check.

We’ve gone the other route – protecting user’s privacy and never selling their data to third parties. Our applicants authorise access once, and then it’s gone. Movem doesn’t store all their transactions, only the ones that are relevant (income and rent). We don’t have ongoing access to your account, like MyMoneySpending may.

Anyway, let me move onto your other points:

_____

1. My point isn’t that you always ask for bank statements – rather when you do, it’s entirely useless. As I’ve shown in my article, it’s easy to forge a bank statement, so why ask at all? Even when Movem accepts bank statements it comes with an obvious “we can’t verify this, this could be photoshopped and entirely false, use at your own risk”.

It’s not as safe as the OBD approach, and people need to be aware of the risks. What are the circumstances you ask for a bank statement? How do you verify that bank statement is legit?

_____

2. Again, my point isn’t that it’s worthless having that information. It’s incredibly valuable knowing their start date and employment status. I wish we could do that. Unfortunately, as I’ve discussed, there’s no way for you to verify it.

Verifying an employer is one of those things referencing companies are good at selling, but bad at executing. As we would be, and everybody else. Some letting agencies genuinely believe that referencing companies can do this – verifying an employer – but they can’t.

I’d love a direct response to my issue of ’email spoofing’ and giving wrong phone numbers.

If you can solve the issue of “who is the person at the end of this phone/email”, then there would be literally thousands of other applications of that technology.

The truth is, you (one, not you specifically) have absolutely no idea how often this happens, because people get away with it. You know the ones you find, but that might be the tip of the iceberg. I’m making up a percentage here, but it could be that 25% of all your applicants are giving false employer info. How would you know?

____

3. You’re right about the landlord character reference providing more than just paying rent on time. And the drug grower is a good example. This is one of the weaker applications of this technology, and an area for improvement.

Is it worth £20 and waiting 24 hours for confirmation that they didn’t grow drugs? I don’t think so. If yes, then there’s still a valid reason to use humans and phone calls. That is, if you can even prove you’re speaking to the landlord. How do you know you’re speaking to the landlord, and not their drug growing friend?

As for the sub-letting, this is a perfect example of the benefits of OBD. Through machine-learning, we will be able to detect subletting by just looking at historic transactions. It’s not possible today, as it’s early stages for us. But this is one of the many areas we’re working on now.

Getting data is step 1, and easy. I know that many referencing companies are copying us now, and I expect everyone to have a product of some sort out within 12 months. The hard bit, and where most of our time has been, is in the interpretation of that data. This is where many referencing companies will fail.

Let me give you a few more examples:

– Using bank data to detect large loan repayments and risky lifestyles

– Using bank data to determine deposit returns or home renovation

– Using bank data to confirm lifestyles (such as being a student)

(There are hundreds more)

Now I use ‘confirm’ loosely. We’re talking big picture stuff here, and we’ll get there one day.

___

4. Yeah, it’s difficult for people with no income, no previous rental payments and no credit of any sort. But what use is a traditional reference here either? Currently agencies will charge them £120 to do what? Get back a proof of address? That can be obtained through CRAs for pence.

^ This was actually my point in the article, about charging twice for referencing when they need a guarantor.

I think we need to accept there are some circumstances where a reference isn’t valid at all. The benefit of Movem is that we will pick up any part time jobs, such as Deliveroo. Or perhaps they work irregular shifts in hospitals.

___

5. Yeah, again this is a great point. Open Banking is very new at the moment, and we won’t get 100% adoption rate. That will rise over time, and in the long term it will be widely adopted.

The first few applications will struggle, and then sooner or later it will become the norm.

That’s why in the meantime we accept bank statements, but do so with plenty of warning.

Resistance to change is normal. Both on the agency side, and the tenant side. But the speed and price will almost be irresistible in the long term.

___

Also, as for FCA regulation, we do not need to be FCA regulated as we use third parties to handle all of the banking credentials and transactions. All of our partners are regulated by the FCA.

As I said earlier, the key isn’t getting the data, it’s the interpretation of that data.

Good point though, and we’ll add this to our marketing to make it clearer – thanks.

___

As for that statement about our terms and conditions, referencing is clearly not a 100% filter right now. That’s why we need that statement. Nor will it ever be. But, as I’ve stated above, I don’t think it’s even in the referencing companies’ / insurance companies’ interest to reach 99.9%.

There will always be unpredictability, and rental insurance is a needed product. My point is that the technology is there to make this system better, and we need to move towards that change.

These referencing agencies who are owned by insurance companies have mixed objectives: to sell more referencing, and to sell more insurance products.

They’re optimising for both, at the detriment to the former.

___

Thanks for taking the time to comment.

Genuinely, add me on LinkedIn and I’d love to chat some more. You’re right, competition is good and we need more companies coming forward and pushing for this kind of change.

Best regards

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Hi KeysafeTenantVetting No Monday blues here, just don’t like the so called disrupters when they have nothing to talk about other than disrupting. This guy is a waste of time. Read his article, it suggests that letting agents are marking up referencing costs unnecessarily. The vast majority of agents that we work with charge an inclusive administration fee, it includes much more than a reference. He is off to a great start, disenfranchising agents will take him to where he deserves to be…..

I don’t usually respond to these types, however on this occasion the utter nonsense was worthy of a comment. Over and out.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

“The trouble with having an open mind, of course, is that people will insist on coming along and trying to put things in it.”

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

You’ve really misunderstood that point Andy. So I’ll try again.

I’m not saying that agencies are marking up costs unnecessarily. I’m saying that when a tenant has a thin history; say a student with no regular income, who lives with their parents, and has no credit score, the referencing companies can’t phone an employer, or a landlord, but they still charge £120.

In those instances, the only check the agency/referencing agency is doing is a CRA check, which costs pence. But do all agencies charge less for this limited service? No. In fact some charge again £120 for a guarantor.

You can disagree with me that the industry is moving this way, but you can’t argue that this doesn’t happen. Not all the time, but it does happen.

That was my point – a few sentences out of a really long article explaining why traditional referencing is broken. I’m still convinced you haven’t bothered reading it. You’ve skimmed it and just reaffirmed your own opinions.

I also think you underestimate letting agencies Mr Halstead. The agencies that’ve approached me after reading this aren’t offended, they’re happy someone spoke out. We’re offering an alternative, not forcing one, and hard-working agencies appreciate a fresh and transparent approach.

Times are changing sir.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I’m all for innovation and new ideas for example penicillin, however this idea is really quite silly.

If there was viable way to remove the human resource from the tenant vetting process don’t you not think that myself and my competitors would have done this by now!

Out of curiosity with respect to your statement “I have spent nearly two years obsessively learning about tenant referencing, from some of the largest referencing companies in the UK” would you care to publish their name as it clearly isn’t us, LA or Keysafe and that doesn’t really leave many left?

I suggest you take this product down, it’s flawed, thin and exposes both agencies and landlords due to your lack of due diligence.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I replied to your next comment.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Sorry I just can leave this one alone!

The paragraph below has been extracted from the Movem website PDF sample report.

Before you read it the meaning of Heuristic used in their get out of jail paragraph below means “stimulating interest as a means of furthering investigation”. The problem with this is that Movem don’t undertake any further investigations!

The Extract

“The information on and data contained in this report should only be used as part of a heuristic approach to evaluating tenants. Movem is provided information from trusted third parties and therefore cannot be liable for any inaccuracy or incompleteness of any information appearing in this report”.

The problem with the Heuristic approach is that it is limited to set parameters within an algorithm, this can be tweaked to give better results for sure; but relies on “Trial & Error” and doesn’t deal with the more complex variables. For example, Open Banking brings back the applicants banking information and you can clearly see regular debits and regular credits that relate to income and outbound payments, but this doesn’t establish whether an individual is about to lose his job, or his company is about to go bust!

All in all Open Banking is a useful tool, but thats all it is-nothing more and cannot be used as a standalone means of successfuly validating a prospective applicants suitability as a tenant. Traditional referencing agencies are charged protecting the the agents against dilapidations and financial loss caused by woefully thin reporting, so back to the drawing board with this one!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

UKTenantData,

Whilst I appreciate the effort you’re putting in here, I think you’re unwillingly proving my point. So thank you.

I’m not suggesting Movem is the ‘one-check-required’, I never said that. What I’ve said is that traditional referencing – the checks you’re charging for – aren’t sufficient. 20 years ago mass-photoshop wasn’t a problem, and email spoofing wasn’t as widely known about. It is now, so it’s time to move on.

On your site you claim to check “how secure their employment is”, how? Seriously, how? Really what you’re doing is ‘phoning somebody to ask about employment’. Or do you go into their workplace and watch them? How do you know that the person you’re speaking to is the employer? This is your chance to prove me wrong.

I’m so confident I could fraudulently pass a reference with you, I’ll make a public wager. We’ll film the whole thing, and the loser donates money to charity?

At least Movem is transparent about what it does. We don’t pretend to do things we can’t, and this makes the cost dramatically cheaper for everyone involved. Why wait 4 days, and pay £30, to get something you could have in a few seconds. If quality is important, why don’t people pay £500 for a tenant reference and you can hire a personal investigator to look into every case? Because people want convenience.

Here’s a thought. Endsleigh, the insurance company, currently provide rental guarantee insurance at the same price for Movem references, as traditional references. i.e, they’ve looked into what we do, our checks and process, and deemed right now, the risk of a Movem reference is equal to that of a traditional reference.

And we’re in year 1, imagine how much smaller the risk will be in year 3? Technology is scary right?

Let’s make the wager happen. We’ll donate to charity so it’s all in good fun.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

How refreshing to have a swinging-handbags session on here that does not have any posting from the Dom & Ducky Show. Pure, unadulterated joy…!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register