Doubts have been expressed by investment website The Motley Fool over the valuation of Purplebricks.

The online agent, which launched in April of last year, floated on Thursday with a valuation of more than £240m.

Shares started at 100p but slid on the first day of trading, and finished on Friday at 95.5p.

The Motley Fool says: “At first glance, Purplebricks looks like it has the potential to shake up the real estate market but the figures don’t seem to add up.

“Indeed, Purplebricks floated at a hefty valuation of £240m, which would imply that the group is racking up at least £11m per annum in sales.”

However, The Motley Fool says that with 4,300 properties for sale, that should net the business fees of just over £4.6m.

It goes on: “That being said, figures put together for a private fundraising by the company a year-and-a-half ago predicted a net profit of £17.6m in the year to 31 July 2015, and £24.9m profit the year after.

“The online estate agent was also promising 30,596 instructions during 2015 and 39,660 instructions for 2016.

“So, without any concrete figures, it’s difficult to place a value on Purplebricks’ shares.

“Purplebricks might be a revolutionary new idea and low-cost way of selling property, but as yet it’s not clear if the company’s business model is sustainable.”

Writer Rupert Hargreaves does not criticise Purplebricks backer Neil Woodford, but cautions: “Woodford may have access to information that’s not yet available to the wider market.

“With this being the case, investors need to ask if they know enough about Purplebricks themselves before making an investment decision.

“Unfortunately, as of yet there are no City forecasts for Purplebricks, and the company is yet to publish a set of results as a public company.

“The company will report its first official set of figures as a public company on January 27.

“So if you’re looking to invest it might be wise to wait for these numbers before taking a position.”

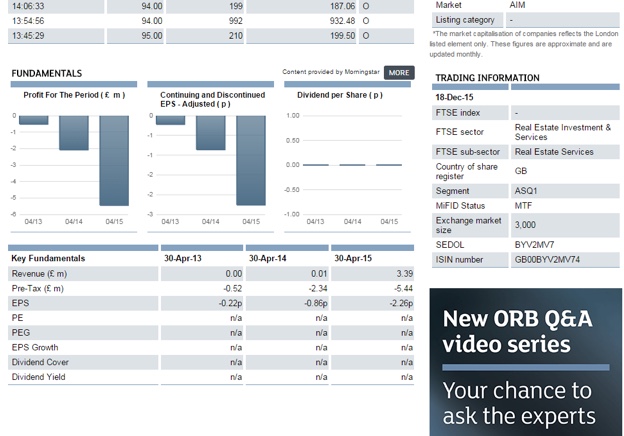

The “fundamentals”, which show revenue to April 30 this year at £3.39m, with a pre-tax loss of £5.44m, are in the screengrab below.

Separately, Bloomberg has reported that in the five months since April, Purplebricks’s sales “jumped to £5.7m”.

It adds: “Purplebricks has online competitors too, like eMoov and Tepilo, which have struggled to make headway. They all face the obstacle of who shows the prospective buyer around the house if the agent won’t do it.

“Sellers may not have time or want to take the personal risk of inviting strangers around their homes.”

However, Bloomberg concludes: “Concern remains [whether] buyers and sellers will try to cut their costs, especially as the vast quantity of house price data now available to the public online undermines the traditional role of agents in helping clients value their property…

“Low cost, online upstarts have disrupted a whole raft of traditional business models – just ask a London cabbie about Uber’s impact.

“Even if Purplebricks falls short of achieving that level of success, incumbent real estate agents need to be wary of the upstart on their doorstep.”

Don’t seem to add up! By my calculation they are over £300 short of breaking even per listing and about £1400 short of making normal profits.

When listing volumes hit the floor as they have done this year so does the turnover of pay per listing listers. Volumes are down 40% for 2015 which means that there is an almighty extra barrier to achievement that wasn’t envisaged in 2014 when profits of £25,000,000 for 2016 were predicted.

It is simply farcical to invest in a low margin, volume dependent, business in an industry where no-one has control over volume.

It is utter stupidity to invest in a firm that is listing so many properties yet is by their own figures losing money on every listing.

I’m not big on stocks and shares, does the £250,000,000 valuation represent how much has got to be invested to keep the stock value up at £1?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Isn’t it about time the bubble had a reality check. It is very difficult to see how anyone, even Call Centre Only Agents, can expect to make a profit with fees as low as they are. Their sums DO NOT add up and someone soon will put things straight. I can see a good market for CCAs but only on a small scale. I guess PPs valuation could be in the region of a million or two but how could they ever really get over £10m? You can see how a pipeline of over 4,000 instructions can be worth something but what are their costs? Better to have 100 sales with costs at 90 than 4,300 with costs at 10,000!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Sorry PB, not PP.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

4300 somethings are great, even as loss leaders but if the verticals (horizontals) the leaders are designed to introduce aren’t happening then loss leaders are simply loses.

Like a balloon with a ***** ( or two) in it, COAR is a bubble that won’t inflate, it can’t and those that try will pour a heap of their own cash in, add a high profile investor and attempt to sucker hapless investors into a scheme that is being widely publicised in the media.

I really, really hope this explodes in their faces and seriously hurts their pocket and reputation but that is tinged with concern for the ‘sheep investors’ they audaciously boasted about luring in with their HPI.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

In the context of a balloon a ‘pr!ck’ isn’t a rude word (Is it?)

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

the forcast 30,000 instructions in 2015 / 4000 real instructions = purple bricks is at least 7.5x over priced just on this figure = worth £33million really.

this doesnt take into account the property that is at least 1 year old and completed and still being advertised.

I think the industry needs to jump on the pont motley did about security and service,,an advert on tv from NAEA would help….

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

PB

PB are another DOTCOM boom disaster waiting to happen. In a shrinking market are sellers really going to do their own selling instead of employing someone who can? I think the founder is a wealthy and smart guy, I think investors will lose a lot of money!!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Prime contender for the ‘No 5h!t, Sherlock Realisation of the Century Award’, methinks!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I’d just like to know which utter numpty keeps buying up two lumps of 140,600 shares at a time, at 95.19p and 100.19p, when the few other buyers seem to get them for between 5 and 10 percent less?

Doesn’t seem like good business sense to me. Terrible negotiation skills and all that.

Perhaps it’s because it’s being done online…

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I suspect it’s the spread – the market makers have an offer and buy price – so if you want to sell it’s 95p or buy its £1 – the share price is the mid point 97.5p –

Any deals at the lower price will be selling – Higher price will be buying.

It’s just like a currency exchange rates.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

If PB’s figures look so horrendous, just try to imagine how the little guys like Emu must be feeling about trying to present themselves!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

“Woodford may have access to information that’s not yet available to the wider market”.

Or not or it is nothing more than a con? which beggars where are the regulators considering just about every walk of like these days is regulated but not this it would seem or they need to start packing for a long holiday at HMP

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I’ve hit on a great money making scheme….

Buy all of PB’s shares at actual current market prices and then, sell them back to whoever is determined to pay way over market figures for them. Who’s in?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Woodford is a highly respected investment manager with a good track record, thus Hagreaves states he may have insider information. Dont buy it myself. This is one bit of stock picking he should have swerved!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

The pied piper plays an alluring tune!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Latest customer numbers for the past 6 months for PB show they have increased by just 2.9%. Not exactly inspiring growth given their investor projections

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register