2024 was a year of minimal change for the prime London property market, with most measures at the end of December close to where they were 12 months earlier, according to LonRes.

2024 was a year of minimal change for the prime London property market, with most measures at the end of December close to where they were 12 months earlier, according to LonRes.

Data provided by the independent property analysts show that there were 7.6% fewer transactions in December compared to the same month last year, which was 17.1% lower than the 2017-2019 (pre-pandemic) December average.

Sales values across prime London have stabilised, ending the year 0.5% down on an annual basis (table 1), up from a (revised) -1.4% in November and the best figure since summer 2023. Looking longer-term, average values are 0.8% lower than their 2017-2019 (pre-pandemic) level (table 1), and 6.0% lower over the past decade.

Monthly Prime Data – December

| Prime Sales | Prime Lettings | |||

| Annual

Change |

Change vs. 2017-19 (pre-pandemic) | Annual

Change |

Change vs. 2017-19 (pre-pandemic) | |

| Achieved prices/rents | -0.5% | -0.8% | 2.5% | 31.9% |

| Properties sold/let | -7.6% | -17.1% | -18.9% | -55.5% |

| New instructions | 28.6% | 23.5% | -26.3% | -57.2% |

Source: LonRes

New instructions were well above typical levels for the time of year in December. They increased 28.6% compared to the same month last year and were 23.5% above the 2017-2019 December average. Vendors typically wait until the new year before going to market rather than listing before Christmas, but the looming stamp duty increase at the beginning of April may have necessitated an earlier start to marketing.

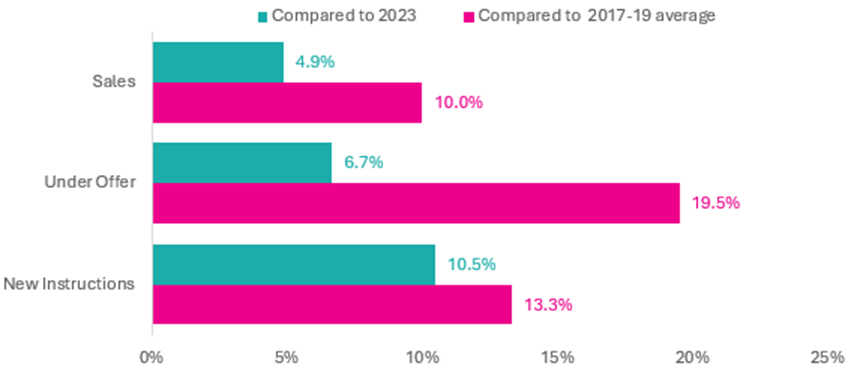

With the Budget at the end of October adding some volatility to the monthly figures in the latter half of 2024, looking back at the data over a full year offers a clearer picture of the direction of travel for the prime London sales market. For transactions, there was 4.9% growth in 2024 compared to 2023, driven by the record-breaking October figures. Over the longer-term, sales volumes in 2024 were 10.0% higher than the pre-pandemic (2017 to 2019) annual average. On that basis, 2024 looks relatively healthy, with under offers and new instructions also up on both 2023 and the 2017-2019 (pre-pandemic) average.

Sales Activity Measures in 2024, All Prime London

Source: LonRes

With new instructions growing faster than sales, available stock on the market has been rising over the past year. On 31 December 2024 there were 10.7% more homes for sale across prime London than a year earlier, and 39.4% more than at the end of 2019. This additional choice for buyers has been one of the factors limiting the potential for meaningful price growth.

Other indicators add to this mixed picture. The average discount fell to 8.5% in December, from 9.4% at the end of 2023. The number of price reductions increased again in December, taking the calendar year total 15% above 2023’s figure. The proportion of sold properties that were reduced prior to sale fell from 52% to 47% over the same period. Time on the market has been static over the course of the year, remaining around 7% higher than pre-pandemic levels.

Overall, the activity metrics and related measures suggest steadily improving demand, which is being balanced by increasing supply. Considered in the context of the domestic economy struggling for growth and 2024 seeing the first change of government in over a decade, this performance is perhaps better than might be expected. But prime London property values have been stubbornly refusing to grow and remain largely unchanged over the course of last year. Even with activity picking up, buyers are price sensitive due to interest rates remaining relatively high and increased taxes at the point of purchase. The SWAP rate expectations that feed into mortgage borrowing costs averaged around 4% in 2024, compared to close to zero at the start of 2024.

Financial market expectations for interest rates

Source: Bank of England

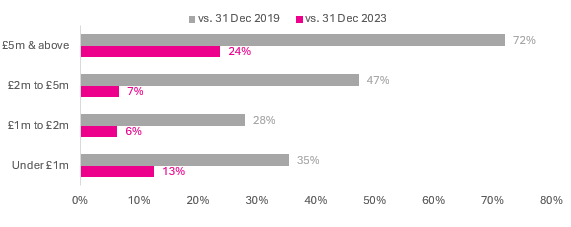

In 2024 the £5m-plus market, which had been the leading prime London price band, fell back. Sales volumes were 4.1% lower than 2023, although there were 36% more transactions compared to the 2017-19 average. New instructions in this market have been rising for many months, finishing the year 25.2% higher than 2023 and resulting in 23.8% more £5m-plus homes on the market over that same period.

Stock on the Market by Price Band Across Prime London (at 31 December 2024)

Source: LonRes

Lower price bands have seen a similar but less strong trend. The £1m to £5m bands have seen the smallest increase in stock, perhaps driven by relatively stronger demand from domestic buyers for family homes in less central areas.

Low steady price growth for London’s rental market over 2024

The prime London lettings market is typically quiet in December and 2024 was no different. Activity was low for the time of year, with agreed lets down by 18.9% compared to December 2023 and new instructions falling by 26.3% over the same period. For the full calendar year the picture is brighter; lets agreed in 2024 were 2.3% higher than 2023 and new instructions increased by 0.8%.

The recovery in stock on the market has stalled, with 12.3% fewer available rental properties across prime London at the end of the year compared to 12 months earlier. Split by rental value band, only at £2,000+ per week is the number of homes on the market rising.

Annual rental growth across prime London increased to 2.5% in December, but this continued last year’s pattern of low, steady growth. Average rents were 31.9% above their 2017-2019 (pre-pandemic) average.

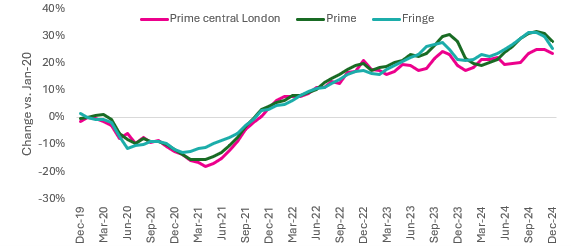

Broken down by sub-market, rents through 2024 followed an interesting path. Prime central London was underperforming prime and fringe for much of the year, but in the fourth quarter values picked up while outer areas saw a fall back. At the end of 2024 average rents across all prime London were 25.6% ahead of their January 2020 level. For prime central London this figure is 23.7% while for prime fringe it is 25.5%, whereas in August 2024 there was a nine percentage point gap between the areas.

Rental Growth Since January 2020 by Area

Source: LonRes

Nick Gregori, head of research at LonRes, said: “In short, the prime London sales market in 2024 saw values decrease and activity rise, but both of these changes have been small. For the full year, sales volumes increased by around 5% compared to 2023 and new instructions rose by approximately twice that over the same period. Values finished 2024 only 0.5% below where they started it.

“This performance is a result of confidence in the housing market and wider economy being relatively weak. The change in government and subsequent Budget announcements didn’t help sentiment but are now behind us and ‘priced in’. People who need to buy or sell are therefore continuing to do so but those in more discretionary markets remain in no rush, having seen little price movement for many months. The opportunity for a stamp duty saving before April may introduce an element of urgency, but in prime London the figures involved are small compared to purchase costs.

“The £5m-plus price point has been most impacted by tax changes and has fallen back from a strong performance in 2022 and 2023. Supply continues to rise in this market but demand has not kept pace as overseas (potential) buyers appear reticent on London as an investment destination. The longer-term context is that the top end of the market remains more active than it was pre-pandemic. Despite the slowdown, 2024 saw 36% more £5m-plus sales than the 2017-2019 average.

“The outlook for 2025 is unclear, with so many external factors potentially impacting the market. Donald Trump’s return to the White House – promising tariffs and tax cuts – could be inflationary for the global economy. In turn this could limit the scope for interest rate cuts here regardless of domestic economic growth. So the much-awaited fall in mortgage borrowing costs may be slower and smaller than hoped, dampening prospects for a stronger recovery.

“The prime London letting market had a quiet December, bringing a quiet year to a close. Activity for the full year was very much in line with 2023 as the post-pandemic recovery stalled, limited by shrinking available stock at all price points up to £2,000 per week. Rental growth of 2.5% is broadly in line with inflation.”

Comments are closed.