Russell Quirk

Russell Quirk“The rate for a new two-year fixed rate mortgage surged from 5.98% to 6.01%” reported the Evening Standard this week on news that home loans have become more expensive due to the City’s outlook for the British economy, inflation and the likelihood of a further increase in the Bank of England base rate when their MPC meets this Thursday.

In recent days numerous similar headlines have shouted at us from the pages of the national media and from the TV and radio news.

Yet, as ever, these headlines are cheap, sensationalist attention grabbers designed to get us clicking and sharing and commenting thus bolstering the coffers of each publisher regardless of the merit of the statements being made. Tabloid exaggeration? Surely not.

Just take a look at the wording of the Evening Standard paragraph above and the fact that it uses the word ‘surge’ in a line that explains, actually, that fixed rate mortgages had just risen by 0.3%. Wow. This equates not to a hike of 10% or 5% or even 1% but an increase of half of one percent on the original rate. This would seem to me to be but a tiny ripple rather than a ‘surge’.

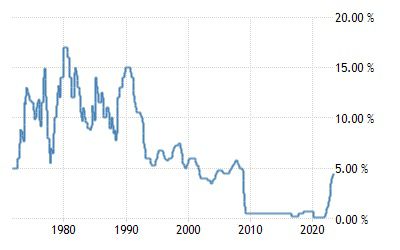

If you are 40 years of age or older you will remember what high interest rates really look like. In 1992 the Bank’s base rate reached 15% and until then the long term average was about 10%. That was what normal resembled. As rates reached 15% it was then that homeowners started to throw their keys back at banks and building societies due to their mortgages being truly unaffordable coupled with the knowledge that their homes had dropped in value by 20% or so in the previous 12 months and many people were therefore in negative equity. My maths says that 15% is a multiple of three times 5% – and I reckon that’s quite a difference.

Indeed in spite of the Telegraph speaking of the ‘…risk of the biggest house price crash on record’ and the Express citing a ‘…mortgage crunch and house price horror looming’, the fact is that this is not the same as 1992 or 2008 or anything like it.

Here’s a chart of interest rates to show the ‘exorbitant’ current base rate in comparison to previous decades. You’ll see that right now the cost of money remains low versus any other time in history except for the last 15 years or so when rates were actually wholly artificial and not least, as we know now, unsustainable.

Put it this way, context is everything.

Put it this way, context is everything.

News reports are quoting that the typical UK fixed rate mortgage will now cost £2900 more per year. That’s £241 per month. Remember that as from 2014 all mortgage applications were stress-tested to an interest rate of, yes, 5%. And so despite assertions that millions will not be able to afford their repayments, the fact is (for it is a fact) that this is simply not true in that borrowers had to be able to afford a much higher rate otherwise they would not have been lent the money in the first place.

Interestingly, again looking at bare facts (something that many property experts in the negative camp don’t bother to do) home repossession volumes were about the same in the early 2000’s as they are now when interest rates were about the same as now. In other words, history tells us that at a Bank rate of 5% people hold onto those keys and CAN afford to pay their way. House prices are approximately 20% higher now than they were in 2020 and negative equity isn’t a threat.

Wages are up too, by 7.2% year on year. This is now a far higher level than house price growth which has slipped into (barely) negative territory to the tune of just -1% annually, according to the UK’s most established index, the Halifax. And so whilst the cost of servicing a home loan may have increased by £200 a month or so to those not on a fixed rate deal, wages are up by nearly the same amount. Do note though that the percentage of people that own a home with a variable rate mortgage is only about 30% of all mortgage holders, the rest are on fixes. And another 30% of owners don’t have a mortgage at all.

Facts. They are sometimes very inconvenient for property market doomsayers and for newspaper bosses craving eyeballs.

In September last year after the Truss/Kwarteng Budget, every budding Nostradamus and their mate started talking the property market down. A ‘35% crash’. A ‘drop of 20% to 30%’. ‘Armageddon…’ etc. Yet, nine months on where is that crash? Where is it hiding? As the Doomsday Clock ticks on there’s certainly lots of egg on lots of red faces albeit that some of these ‘experts’ are now busy moving the goal-posts by stating that ‘I meant the 35% drop will happen at some time in the future’ – which is a bit like betting that you’ll one day play football for England. A wager that will only pay out to the winners once you’re dead.

In October 2022 I stated publicly that house prices would not be lower a year hence than then. I might not prove right that given stubbornly rampant inflation, an incompetent government, a more incompetent Bank of England and a war in Europe that many thought would have ended by now – but I’ll be a lot, lot closer to being right than the hysterical opinionators that called a crash in house prices that is so, so far away from what has actually transpired almost a whole year on.

And frankly those that have done everything they can to talk the market down in 2023 and to weaken sentiment just for their own political satisfaction or indeed in some cynical attempt at a personal PR grab, we see you – and we see your distinct lack of credibility too.

Russell Quirk is Co-founder of PropertyPR and a well-known media commentator on property and politics

Would it surprise you that since Christmas, UK house prices have risen by 3.66%?

But how can I say house prices are rising when the HMRC & Land Registry and other indices from the banks state they are falling?

The Land Registry figures published last month will be from sales COMPLETED (i.e., keys and monies handed over) in February 2023.

The HMRC data from sales COMPLETED in April 23.

The Nationwide from Mortgage OFFERS from April 23

Yet, as everyone knows, it takes on average, 19 weeks from agreeing on a sale to a completed sale in the UK,

So those Land Registry / HMRC house price figures are from house sales agreed upon in September or October 2022

…and Nationwide from Sales agreed in November /December (because a mortgage offer normally arrives a couple of weeks before exchange & completion)

So how can I say house prices are rising?

By measuring what houses sell for at the sale agreed date by their square footage.

Now, the measure of £/sq. ft is not a particular great way to judge the value of an individual property.

However, when looking at a national and regional level, its accuracy is excellent

The average price per square foot at sale agreed matches the Land Registry and Nationwide House Price Index to a very high tolerance/accuracy level (98% accurate on a national level),

… but here is the killer part …

…. that £/sqft data gets published in real time .. ie 7 or 8 months before the Land Registry/Nationwide publish their data.

So by tracking the £/sq. ft figures for the UK on SALE AGREEDS it will give us an excellent idea of what the indexes will be in 7 or 8 months time

The top of the UK property market on sale agreed was In June 2022 when the average £/sq. ft achieved for all UK house sales agreed was £346.85/sq. ft.

By December 2022, this had dropped to £332.14/sq. ft, a drop of 4.43% (for the UK homes sold stc in December ’22).

By this April, the average £/sq. ft achieved for all house sales agreed in the UK had risen by 3.66%to £344.76/sq. ft.

Thoughts anyone?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

‘Cheap, sensationalist attention grabber’ ….. the only thing missing is ‘failed online estate agency business’.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I can’t believe I am agreeing with the Quirk. Prices will not drop overall and unless Armageddon is unleashed.

Number of factors to consider:

1. For a price crash, all properties have to drop in price in relatively the same time. Not going to happen.

2. The financial crisis of 2008 (and previous scenario’s of property boom and bust) caused a hiccup and was being said by the pundits that the crash would be 25%. Never materialised. As I said back then, the market as a whole would be in negative equity and people would stop moving until times got better, many years later and not sell at a loss. Not forgetting negative equity issues of mortgage lenders effectively banning that idea. History has proven this to be the case.

3. Regrettably there will always be some who have to sell at a loss for a variety of personal reasons but overall will not drag the prices down for all. Shrewd buyers will sit and wait to pick them off.

4. History has proven that all that really happens is the market stagnate till it recovers. This will happen.

5. Simple test if you own your home. Would you sell at a loss if you don’t have to?

6. Armageddon would be unleashed by a political party that was horrendously reckless in its fiscal management of the country. However, no matter what you are promised, believe or see happening by vote hunting political rhetoric & parties, the likelihood with so many advisors etc behind closed doors, IMF and the like, not going to happen.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

The current property boom started in 1997 when the average house price was a little over 4x average earnings (there were some dips along the way). BOE Interest rate was 7% back then and falling. Money was relatively cheap, stable and easy to come by and property prices started to climb but earnings didn’t keep pace. Today, we see the average property price is 9x average earnings; debt levels had increased substantially but was affordable while interest rates were so low.

We have become used to 15 years of ultra low interest rates and our cloth has been cut to suit a low interest rate environment but that is changing along with a higher tax burden, inflation outstripping wage growth, energy bills that will not fall until the autumn (as energy use starts to increase again). 1.2m people about to be shocked with a significant rise in their mortgage payments by the end of the year as they come off their fixed rates, while the cost of everything is squeezing their finances.

15% interest rates in the past are not too dissimilar to 6% interest rates now, when it comes to disposable income.

Credit card debt will rise (with eye watering interest rates). There will be payment defaults. Try getting a new mortgage with a record of defaults and see what the rate will be then. The property market will stall but there will still be forced sellers; divorce, death, relocation; these people will have to accept less for their property and those buying another will expect to pay less. It’s a downward price spiral that will unravel over the next 18 months or so.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Give it time. If you ware not seeing the fast pullback on prices, you will very soon. If a ‘crash’ is 20% off prices from the latest peak then we are well on our way to that.

You only had to look at RM listings to see the reduced stock. This feels very like 2007 to me, the market stopped in 2007 in my neck of the woods, sooner than much of the country that felt the drag in 2008….Anyone saying the market is fine is either deluded or working in rentals.

Remember though, the climb back up from the drop will be greater than the previous peak, it always is. Will just be very painful for some to bear. sadly.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Can’t believe I have spent 3 minutes of my life signing up just to send this.

Nobody cares!

you look like the worst side of a bad potatoe and we are dying because you are that boring we all yawn and run out of oxygen.

Be somebody and make a difference instead of pointing out obvious things! You are a Vogon!

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register