Savills and Knight Frank are reporting that prime central London (PCL) is back in demand with buyers and that there are early signs of overseas purchasers making a return to the capital.

The UK’s prime residential markets saw further price growth in the first quarter of 2022 underpinned by high levels of buyer demand and continued low levels of properties for sale, according to the latest analysis from property group Savills.

But while annual price growth in the country markets continued to be exceed that in the capital, the difference in price growth in the first three months narrowed considerably, fuelled by a gradual return to the office among domestic buyers and the beginnings of a return of international demand in central London.

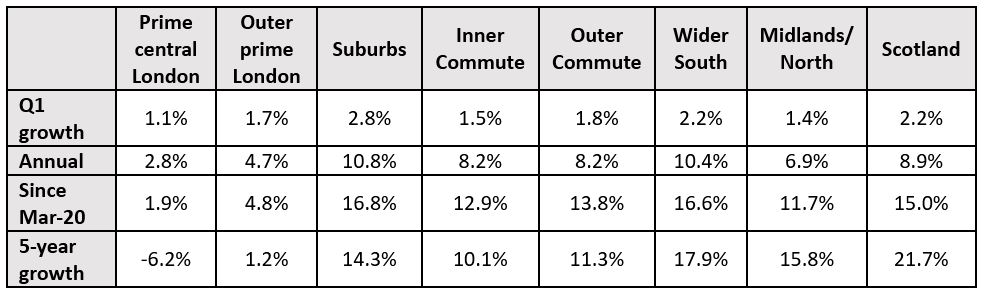

Prime central London recorded its strongest quarterly price growth in eight years as international buyers began to re-enter a stock-constrained market that has been largely dominated by domestic buyers over the past two years. Prices ticked up +1.1% in the quarter, leaving them +2.8% higher than a year ago. Though still outpaced by the country, this was the most robust performance since the stamp duty changes of 2014.

In a clear sign of back to work thinking, London’s prime flats and smaller houses began to see more significant price growth for the first time since the first lockdown and more urban locations such as Canary Wharf, Islington and Shoreditch outpaced leafier suburbs.

“While activity levels have slowed in the mainstream, there is still a strong core of unmet demand at the top end of the market that, for now, remains undeterred by higher costs of debt, rising costs of living and the geo-political uncertainty triggered by the war in Ukraine. Here, equity outweighs debt as a source of funding and much higher levels of disposable income mean buyers have been more insulated against macro-economic pressures,” says Frances Clacy, Savills research analyst.

“At the same time, supply remains well below normal levels in virtually all prime locations creating the conditions for continued price growth. However, we would expect to see increasing price sensitivity creep into the market over the remainder of the year given the economic backdrop.”

While international buyers began to return to prime central London over recent months, the story of the past year has been about domestic, UK domiciled demand. In central London, this has led to the strongest annual growth in locations such as Holland Park (+5.3%), Notting Hill (+4.7%) and Chelsea (+4.6%) popular for their traditional family housing stock.

More widely, the first quarter saw the capital begin to realign with the UK’s wider prime regional markets.

Here, space and greenery clearly remain a factor. The strongest annual price growth was recorded by homes with large gardens, up 9.0% annually, with leafy suburbs such as Richmond (+9.1%), Primrose Hill (+8.1%), Ealing (+8.1%), East Sheen (+7.7%), Fulham (+7.6%), Wimbledon (+7.6%) and Chiswick (+6.5%) the top performers.

But in the clearest signal yet of life returning to London’s most urban postcodes, in the first three months of the year price growth in these locations was outpaced by Shoreditch, Canary Wharf and Islington which saw quarterly price growth of +3.7%, +3.4% and +3.3% respectively as City workers started to return to their desks.

House prices across the UK’s prime town and country locations rose by +2.0% in the quarter and +9.0% year on year, suggesting the ‘race for space’ has not yet fully run its course, though proximity to London is starting to influence performance once again.

The strongest growth was recorded in high value suburban markets such as Esher, Rickmansworth and Weybridge with +2.8% quarterly growth and +10.8% annually “providing increasingly clear evidence of proximity to work being factored into decision making once again,” according to Clacy.

“More widely we’re seeing many regional towns and villages showing stronger quarterly price growth than the purely rural locations, suggesting proximity to local amenities are becoming a more pressing consideration. Cities as far apart as Bristol, Glasgow, Winchester and York are outperforming their surrounds.

“All this said, best in class country houses worth £2 million-plus are still highly sought after and values rose by +10.3% over the past 12 months, underpinned by a prolonged mismatch between supply and demand.”

Knight Frank concur with the view that overseas buyers are back in the prime Central London (PCL) markets but not yet at a meaningful and sustained level.

They say that compared to the wider London market and rest of the country, demand was notably stronger in the first quarter of this year inside zone 1.

The number of new prospective buyers in PCL was 84% higher than the five-year average and that compared to an increase of 71% across the whole of London and 42% in UK regional markets.

The number of offers accepted in PCL was 104% higher over the same period, which was greater than a figure of 83% in London and 43% in country markets.

As well as stronger demand and a bigger pipeline of sales, supply is also picking up more quickly. The number of market valuation appraisals was 20% higher than the five-year average in PCL, compared to 7% across London and 14% outside the capital.

While other UK property markets stole the headlines during the pandemic thanks to the much-publicised ‘race for space’, prime central London is now moving back into the spotlight. The fact prices have been falling for six years helps, says Knight Frank.

Average prices in PCL are 16% lower than they were at the start of 2016. That compares to a 9% decline in prime outer London and a 13% increase in country markets. Prices fell in PCL as it bore the brunt of tax changes and political uncertainty in the wake of the Brexit vote in June 2016.

“People have worked out that there are hotspots of good value in prime central London,” said Stuart Bailey, head of prime London sales at Knight Frank. “For example, you can buy a freehold house in Belgravia for less than £2,000 per square foot at the moment.”

The key question is when international buyers will return in meaningful numbers.

While overseas activity was strong in the final three months of last year after travel rules were relaxed in October, it has been more sporadic this year, initially due to the arrival of the Omicron variant at Christmas.

Given the extent of lockdowns in some parts of the world still, any return of overseas buyers is likely to be gradual rather than transformational.

“I’m not sure there will be a clear moment when international buyers return,” said Stuart. “Some sellers are waiting for it to happen but it’s proving to be a rather erratic process. By the time overseas demand picks up, interest rates will be higher and the cost-of-living squeeze will tighter anyway. Sellers in PCL may instead want to take advantage of the fact that supply is tight and large numbers of UK-based buyers are actively looking for property at the moment.”

Comments are closed.