![]() Investors are being urged to keep a close eye on Foxtons’ share price, which is being tipped for growth this year.

Investors are being urged to keep a close eye on Foxtons’ share price, which is being tipped for growth this year.

City brokers, Panmure Liberum’s and Zeus, have identified Foxtons as a good bet thanks to its existing model. Both companies have named the estate agency as one of their key stock picks for 2025.

Foxtons’ under offer sales pipeline is currently at its highest level since the EU referendum in 2016, with plenty more room for further improvements in 2025, according to the agency’s CEO, Guy Gittins.

He said: “I reflect a positive outlook on the year ahead, particularly when you look at the sales and lettings markets still recovering from what happened with the Covid shock and the budget of 2022 the market, we know for sure the sales market will be considerably better in 2025 than it was in 2024.

“Each time we see even a small interest rate reduction, it brings with it a wave of new buyers being able to come back into the market so we start at the start of this year with great momentum.

“We’ve seen our under offer sales pipeline – that’s the number of sales that we’ve placed into solicitors hands – the value and the volume of that pipeline is actually at its highest rate since the EU referendum.”

Top stock pick for 2025;

Zeus’ view: Foxtons continues to grow its recurring lettings division revenue, both organically and bolt-on M&A. In 2024, Foxtons’ Sales revenue has stepped up, reflecting increased market share of a recovering market. Recovery in Foxtons’ sales revenue significantly improves contribution to overheads. After allocating overheads, we expect this division’s operating margin to have improved from (27)% in 2023 to (13)%. Increasing market share and normalising market volumes are turning Foxtons’ Sales operating margin positive. Cuts to new mortgage rates would be beneficial. Foxtons’ operational performance reflects both its leadership and investment in Foxtons’ intangible assets (e.g. Brand, data, BOS platform, client relationships). We see these factors as providing competitive advantage in a valuable but highly fragmented market.

The estate agency’s share price is currently at 67.7p but Panmure Liberum has named it as a ‘buy’ with a target price of 103p.

Panmure Liberum identified Foxtons’ ‘significant market share gains’, supported by its ‘systematic sales approach, unique technology platform and strong brand’, as offering huge opportunity for investors.

“Meanwhile, regulation creep is favouring the larger agency networks [such as Foxtons], adding further scale benefits,” said Panmure Liberum’s chief economist Simon French. “The business is well placed to materially expand its market share in lettings [through organic growth and M&A] and to deliver improved earnings within sales.”

“Even without any M&A, we see scope for a 16.3% earnings per share CAGR [seven-year view], he added. “Solid progression was demonstrated by the third quarter trading update, which highlighted that revenue trends remain firm in both lettings and sales.”

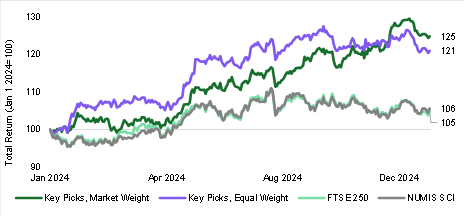

Panmure Liberum: Our Key Picks 2024 portfolio had a stellar year. The equal weight portfolio returned 21% and the market-weight portfolio returned 25%. This performance compared to UK mid-cap and smaller company indices returning 5% and 6% respectively. Our larger, post-merger, coverage universe allows us to enlarge the selection of companies for 2025 and – following client feedback – we include each sector analysts’ most preferred and least preferred selection. There is of course plenty of anxiety surrounding UK equities following another year of outflows from UK strategies, a darkening economic picture since July’s general election, and a stubborn valuation discount. However, there are reasons for enthusiasm. The interim report of the Pensions Review has acknowledged the damaging impact of UK de-equitisation on saver returns and investment. Policy solutions to reinstate a natural buyer of UK equity/ level the playing field with international equity are being actively considered. And whilst the economic outlook remains uncertain, we have passed peak refinancing stress for UK consumer lending, and additional public spending in 2025 will act to offset recent private sector weakness. Our Key Picks document provides our preferred way to navigate this backdrop with our latest research for these companies provided below.

Key Picks 2024: Total Return

Source: Panmure Liberum

| Our Selections | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

*Corporate Broking Client of Panmure Liberum |

But surely this pipeline needs to be discounted to reflect shorter timescales, and lower fall through rates that were prevalent at the time?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register