Analysis by property group Savills shows that gifts and loans from the Bank of Mum & Dad (BOMAD) will hit a new high in 2021, supporting almost half of all first time home buyer transactions as rising house prices increase the pressure on those saving for a deposit.

Analysis by property group Savills shows that gifts and loans from the Bank of Mum & Dad (BOMAD) will hit a new high in 2021, supporting almost half of all first time home buyer transactions as rising house prices increase the pressure on those saving for a deposit.

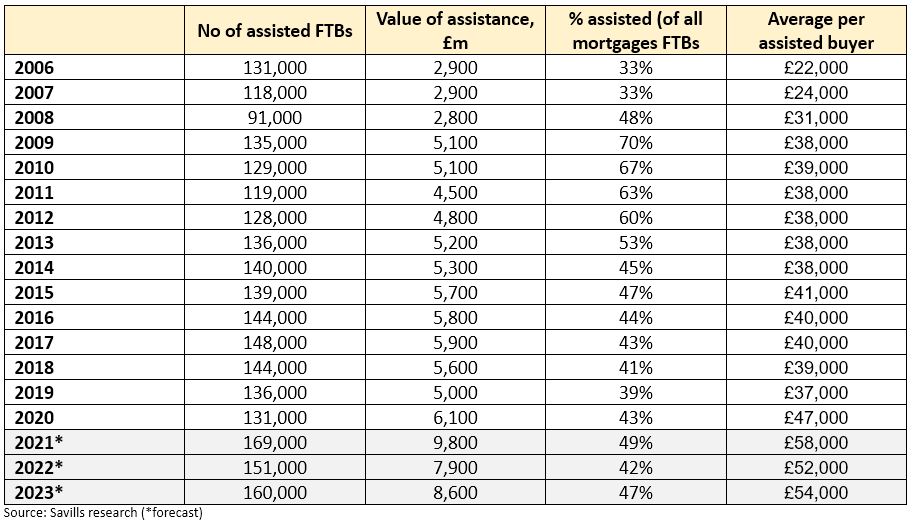

Total BOMAD contributions are expected to total £9.8 billion this year, Savills says, contributing more than three times the value of Help to Buy loans (£3.0bn) granted in 2020 and an average of £58,074 per supported purchase.

These funds will help 169,000 first time buyers onto the housing ladder, equivalent to 49% of all first time buyer transactions.

The number of first time buyers fell back in 2020, to 304,000, their lowest since 2015, as lockdown and employment uncertainty eroded activity. Still, BOMAD contributions totalled £6.1 billion, up from £5.0 billion in 2019, as tighter lending criteria put additional pressure on aspiring home owners.

Over the past 10 years, BOMAD has subsidised first time buyer activity to the tune of £53.9 billion, helping almost 1.4 million buyers access their first home.

Numbers of first time buyers receiving family assistance and amount of assistance given to get on the housing ladder

This year is expected to represent a peak of family support, with total contributions projected to fall slightly in 2022, as loan to value ratios begin to normalise. Savills has based its assumptions on loan to value ratios for first time buyers recovering to 76% by the end of 2021 and to 78% by the end of 2023, theoretically reducing deposit requirements.

But, as Help to Buy is withdrawn completely from March 2023 onwards, it is likely that increasing numbers of first time buyers will need assistance.

As such, while BOMAD lending is projected to slip back to £7.9 billion in 2022, supporting around 42% of purchases, it is then expected to bounce back to £8.6 billion and 47% of purchases in 2023.

“Despite strong levels of activity and price growth across the housing markets, lenders have tended to favour less risky, lower loan to value lending, making it harder for new buyers to access the market for the first time without assistance,” says Frances Clacy, Savills residential research analyst.

“While we expect lending at a higher loan to value ratio to continue to be available, slowly rising interest rates will act as a brake on affordability, while rising costs of living, increased national insurance and the prospect of a lower threshold for student loan repayments will make saving for a deposit all the more challenging.

“As such, for those fortunate enough to be able to access it, family support will continue to be a vital source of funding for first time buyers, particularly in a post Help to Buy environment.”

Comments are closed.