The Financial Conduct Authority (FCA) has been urged to review how deposit replacement scheme products are being sold to tenants.

Deposit-free schemes have emerged as a way for letting agents to earn referral fees and cut costs for renters.

The idea is that tenants are given the option to pay a small fee, rather than a traditional deposit, to purchase a product that covers the landlord for varying levels of arrears or damages.

But Jon Notley, former Zoopla commercial director and founder of the Zero Deposit scheme, is warning that various commission levels, business models and types of regulation in the sector could create a payment protection insurance-style mis-selling scandal.

In particular, he is urging the FCA to monitor where firms are claiming to sell an insurance product but may not be regulated themselves or could have the paperwork written in a way that it isn’t clear who the policy covers.

He warns that if a firm isn’t fully regulated by the FCA, they could be selling products that appear regulated without meeting the necessary requirements on pricing and transparency.

Tenants could also end up losing cover they thought they had paid for and get pursued by a landlord if a firm went bust, he added.

In contrast, if a tenant uses a firm fully regulated by the FCA, they could complain about issues to the Financial Ombudsman Service and have losses covered by the Financial Services Compensation Scheme if a business collapsed.

Notley said: “We have always believed that taking the fully FCA regulated route is best for customers. The FCA’s system of regulation provides an external yardstick by which firms can be measured and a shield for consumers when needed.

“Customers must be given sufficient information to understand the value of the products they are purchasing and given a safety net when they don’t.

“Non-regulated firms have the freedom to offer higher commissions and inferior products without sufficient controls and safeguards in place, which could expose a large number of tenants and landlords to serious harm.”

Dan Wilson Craw, director at Generation Rent, said: “No deposit schemes are relatively new, but we’ve already heard from tenants who have made extra monthly payments only to be hit with spurious damage claims upon moving out, and with no confidence in the process of challenging them.

“If these schemes are to be an option for tenants, they must be regulated properly so that tenants have somewhere to turn if they feel they’ve been mistreated.”

Deposit replacement schemes have already gained negative coverage.

Last month, This Is Money reported on a case of a Leaders Romans Group tenant who had opted for the agent’s ‘no deposit option’ but had mistakenly believed it was an insurance policy so was shocked to receive a £1,318 bill at the end of her tenancy.

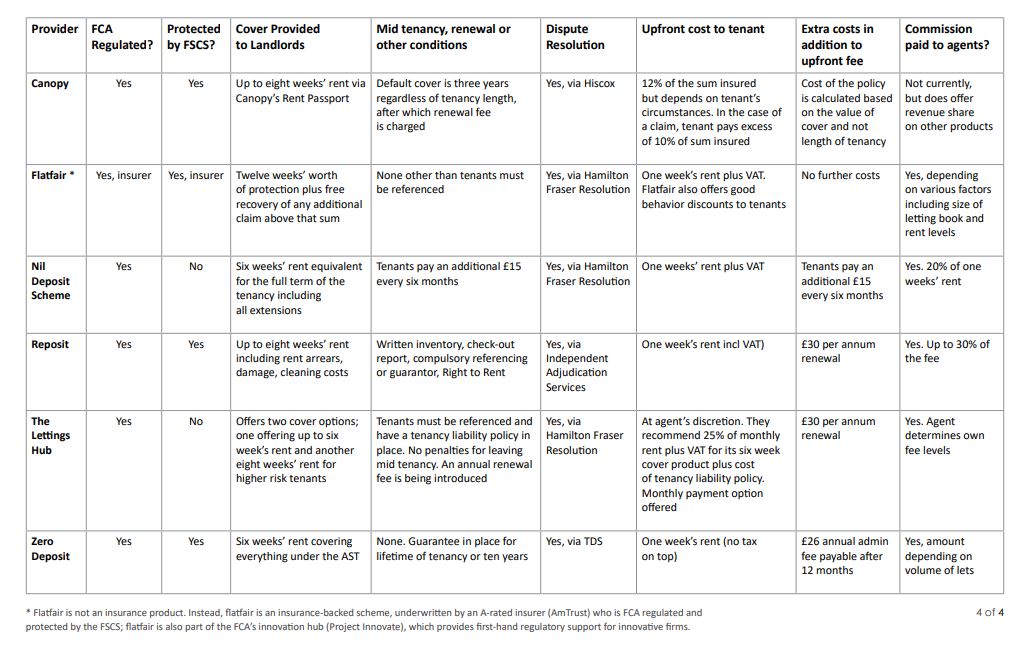

ARLA Propertymark has also warned agents to do their due diligence on these schemes and has produced the table below that shows the various business models and levels of regulation among some of the main providers.

Major agent taken to task over ‘no deposit’ scheme that is not an insurance policy

A few questions & comments for Jon;

What is the difference between fully regulated and regulated by the FCA?

PPI mis-selling was transacted by banks and they are regulated

Zero Deposits offers ‘various commission levels’

What cover are tenants purchasing? At the end of the tenancy, tenants are still required to meet the full costs of their obligations under the tenancy agreement

Under the Zero Deposit scheme, the tenant pays an ‘insurance premium’. Is it fair to suggest that the tenant might believe that they are insured?

For me the debate is not just about the regulatory status of the replacement deposit market, it is more about whether the various schemes will perform well enough to stay the course. I believe that the stand-alone schemes are much more at risk than those integrated with quality tenant referencing, rent guarantee and tenants liability insurance. Time will tell……..

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Is it not the case that the agents do not ‘sell’ or ‘give advice’ on these products. The tenants also have to be given the choice of paying 5 weeks rent or choosing one of the above products.

As they apply to the Deposit Replacement Scheme directly, I am not sure how agents or Landlords could be at risk of a mis-selling scandal as they have not ‘sold’ or ‘advised’ on a product.

Simply referring someone to one of these schemes surely cannot make them liable or am I looking at this too simplistically ?

I have reviewed a few of these schemes, and providing the firms do not go bust, it appears to be a fantastic solution to reducing up front costs. Maybe if the industry had supported this product a few years ago, we may not have the Tenant Fee Ban today ?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

As I understand it you can refer someone to ‘deposit replacement schemes’ in general, but where you refer them to an actual product [be that Reposit, Canopy, FlatFair etc.] it becomes a ‘regulated activity’. Regulated activities includes ‘suggesting or recommending a certain [i.e. named] insurance product’. Where an agent suggests, or refers a tenant to the scheme they offer [they’re not likely to suggest/recommend another scheme?], they will be undertaking a regulated activity.

I’m happy to be corrected if this is wrong … 🙂

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

What I don’t get is how they can offer deposit cover of 6 – 12 weeks when cash deposits are now capped at 5. Surely they can only make any tenant liable for deductions for up to 5 weeks as would be the case with a cash deposit not taking in to account any rent arrears of course.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

Hi Simon, the tenant is exposed to unlimited liability, regardless of the deposit or replacement deposit scheme. If the tenant is liable for £50k of damage, then they can be pursued for every penny. Cheers. Andy

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

and it for that very reason why I believe these schemes will end up as the next PPI style scandal. If I but house insurance and my house burns down my insurance company rebuilds and replaces my possessions. I buy a tenant replacement ‘insurance’ which isn’t an insurance although markets as such by some, they pay out and I’m still liable. Yeah really good for the tenant, not.

i gave my thoughts on this in a previous PIE article and have since seen these being rubbished by the 0 deposit industry on other sites.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

That’s an interesting point Simonr6608 🙂

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

I do have a feeling that this is going to be a problem for us in the future.

Something is going to come up where some unscrupulous Lettings agency is going to try and increase their revenue following the fees ban by telling all their prospective tenants about this wonderful scheme where for the equivalent of 1 weeks rent, they will be “insured” for 6-8 weeks work of “deposit”. They will omit the fact that the tenant will still owe the funds. There will be shouts of misselling much like the PPI issues. You only need to look there as to what will happen. Look at how many people signed up to PPI and signed a document agreeing to what it was, yet it was still determined that it was missold and people would get refunds.

We also have these tenants who cannot afford a deposit, not a good sign in itself, who may own money at the end of a tenancy. The deposit replacement scheme pays out to the landlord and chases the tenant, who has no funds to repay the scheme. The deposit replacement scheme starts losing money as they cant claw back the funds they are obligated to pay out. They go under, landlords lose their security and lose out more.

I see a lot more problems being caused by this than it solves.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

These zero deposits are useless its an insurance policy and we all know insurance companies do not like to pay out so both landlords and tenants are going to be screwed.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

** I will rephrase as my last comment was deleted, so much for freedom of speech.

Jon’s comments directly contradict the ARLA document on this matter. Which to me doesn’t reflect well on him.

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register

stay well clear IMHO (of all the schemes)

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register