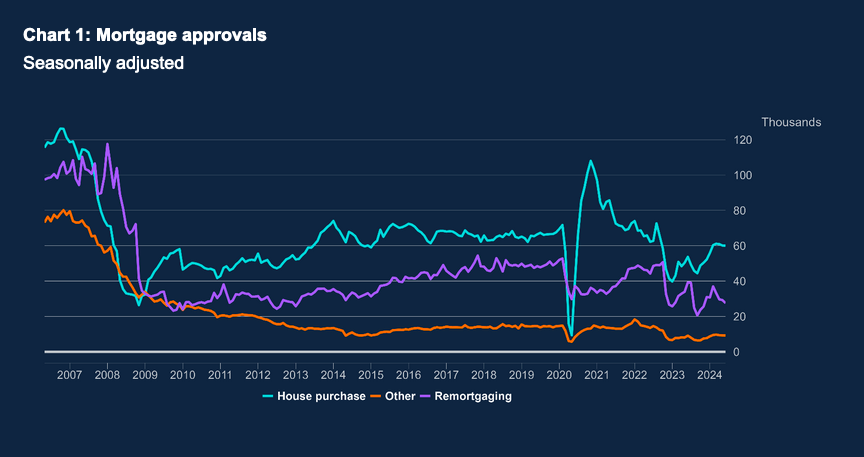

Net mortgage approvals for house purchases remained broadly stable at 60,000 in June, according to the latest Bank of England Money and Credit report.

On a net basis, individuals borrowed £2.7bn of mortgage debt in June, up from £1.3bn in May. Approvals for remortgaging decreased from 29,300 to 27,500 over the same period.

The annual growth rate for net mortgage lending rose to 0.5% in June, after a rise to 0.3% in May, continuing the trend seen in previous months. Gross lending decreased to £20.8bn in June, from £22.6bn in May, while gross repayments decreased by £1.6bn over the same period, to £18.7bn.

The ‘effective’ interest rate – the actual interest paid – on newly drawn mortgages saw a slight increase of 3 basis points, to 4.82% in June. Similarly, the rate on the outstanding stock of mortgages rose by 4 basis points to 3.65% in June, from 3.61% in May.

Nathan Emerson, CEO of Propertymark, commented: “The figures show that the general election did not damage people’s confidence in borrowing money to purchase their next home in the way many may have anticipated.

“Momentum has sustained itself. However, now we have a newly elected government that is ambitious about building new homes, we hope that confidence increases further in the housing market.

“In addition, Propertymark is keen to see further confidence boosts, with the Bank of England considering a cut in interest rates when they feel this is the right time to do so.”

More reaction:

‘Treading water’

Anthony Codling, managing director, equity research at RBC Capital Markets, said:

“Stability is good, but in our view, the UK housing market appears to be treading water, waiting for, hoping for the first bank rate cut.

“There is a small chance that cut could come on Thursday, but we believe the first cut is more likely in September. Once mortgage rates start to fall, we expect housing market activity to pick up.”

‘Steady recovery’

Simon Gammon, managing partner, Knight Frank Finance, said:

“Mortgage approvals continue to hover in the 60,000 range, down from about 66,000-a-month before the pandemic. Repeated false dawns in the battle against inflation have left the property market stuck in first gear, but it’s now very likely that we’ll have a busier second half of the year.

“The lenders have cut margins to the bone in the battle for market share, and this pattern should continue as the Bank of England offers some relief in the form of reductions to the base rate.

“The first Bank of England rate cut, whether it arrives on Thursday or perhaps in September, will provide a big boost to sentiment, which has improved for several months already. All the signals point to a slow and steady recovery as lenders introduce more fixed rate products starting with a 3.”

‘Confidence returning’

Emma Cox, MD of real estate at Shawbrook, said:

“Despite the added dynamic of the general election, mortgage approvals for house purchases have remained broadly stable as the market outlook becomes more positive, offering hope for landlords.

“Confidence appears to be returning to the market, which is adapting to higher interest. Professional landlords are keen to secure deals, expand their portfolios, and diversify their strategies. High-yield options, such as HMOs and semi-commercial properties, are particularly popular as these landlords aim to grow their businesses.”

‘Demand will rise’

Mark Hollands, head of sales & distribution, Bluestone Mortgages, said:

“Today’s mortgage approvals indicate that consumer confidence remained steady. This combined with major lenders cutting rates in anticipation of a base rate reduction should see demand for property rise in the second half of the year.”

Comments are closed.