Demand for property in London remains fragile, despite the Bank of England’s decision to pause its cycle of interest rate hikes in September.

While the number of new prospective buyers in London rose 12% between August and September as this year’s autumn market began, it was half the increase experienced in the previous two years. In calmer political times before 2016, the same jump exceeded 40%.

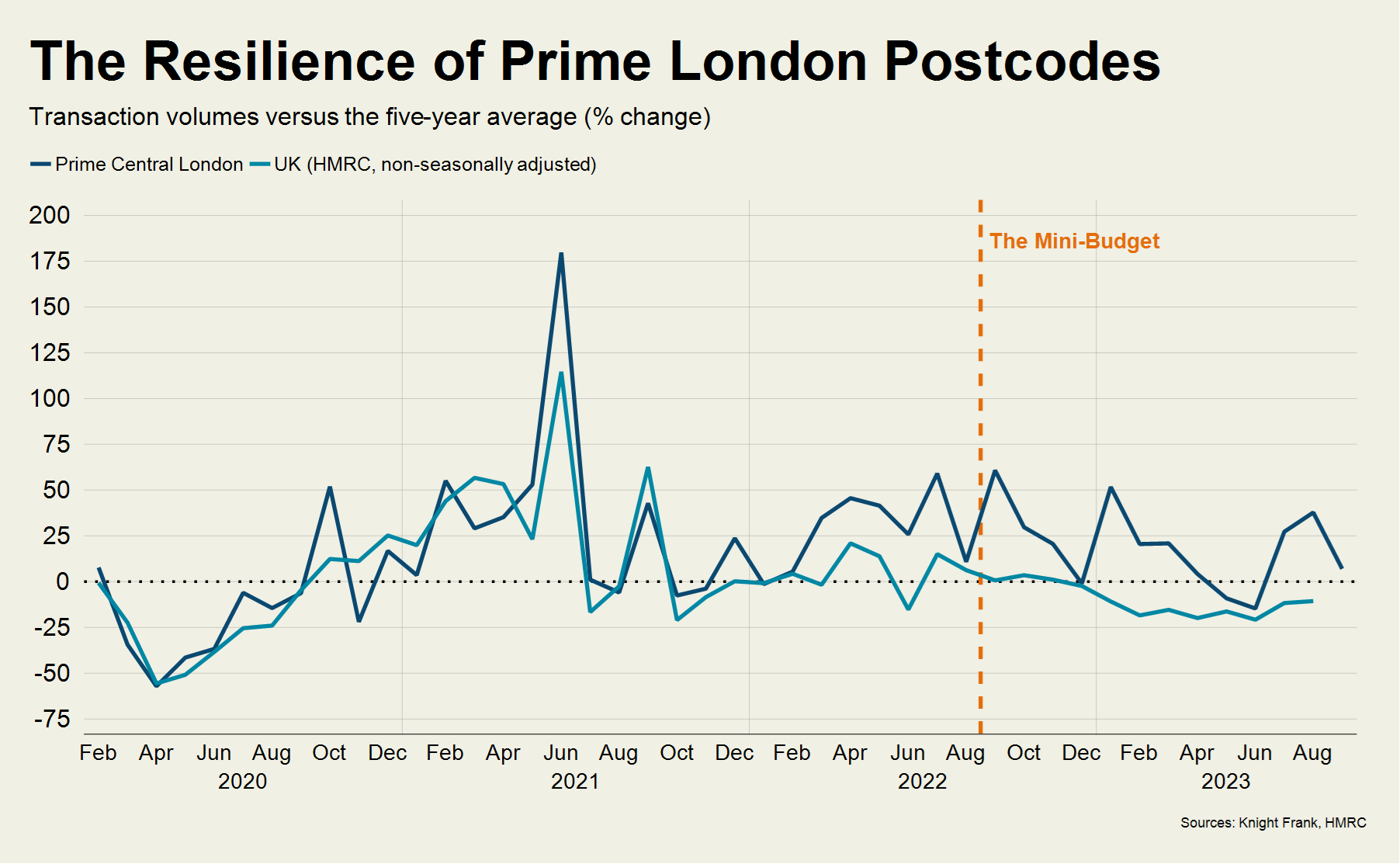

Essentially, the prime London property remains in a holding pattern, according to Tom Bill, head of UK residential research at Knight Frank.

He explained: “It [London] has not experienced the extent of price declines seen across the UK but neither have the capital’s more affluent postcodes been immune from the deteriorating economic sentiment.

“The Nationwide index recorded its second consecutive annual decline of 5.4% in September, while prime central London experienced a more modest 1.7% fall. In prime outer London, the decrease was 1.4%.

“Last month’s pause by the Bank of England added to a sense that we have gone through the eye of the storm.”

Indeed, Knight Frank has updated its forecasts to reflect the fact that the firm expects most of the decline in house prices across the UK will take place this year.

Bill continued: “We are forecasting a 3% decline in both prime central and outer London this year, as those markets continue to outperform the rest of the UK in terms of trading activity as well as price performance.

“The number of new prospective buyers across the UK was 11% down in the third quarter of this year compared to the five-year average, while the figure for London was up by 13%, Knight Frank data shows. Meanwhile there was a 14% increase in exchanges in the capital while sales volumes fell by 9% across the country.

“The primary reason for this resilience is the fact average prices are still 16% below their last peak in 2015 in prime central London. In prime outer London, they are still 8% down.

“Average prices are also 2% lower than they were before the pandemic in PCL, which helps explain why transaction volumes were 7% higher than the five-year average in September, as the chart shows.”

Meanwhile, across the UK, there was an equivalent 11% decline in August, non-seasonally adjusted figures from HMRC show.

Knight Frank is predicting a 7% decline in UK prices this year, which would still leave them more than 10% higher than before the pandemic.

In a departure from what took place after the global financial crisis, property prices in London have been far less volatile than the rest of the country during this latest period of economic turbulence.

Bill commented: “The downwards trajectory for annual rental value growth in prime London markets continued in September as supply increased and demand held steady.

“The number of new prospective tenants in prime London postcodes was flat compared to the five-year average in the third quarter of this year, Knight Frank data shows. Meanwhile, listings in PCL were only 12% down, according to Rightmove, a figure that compares to decline of 37% in the same quarter last year.

“Annual rental value growth in prime central London (PCL) was 11.2% in September, which was the lowest figure in two years. In prime outer London (POL), an increase of 10% means that next month we are likely to be back in single digits. It was also the smallest rise in two years.”

Bill highlights that supply has decreased in recent years as more owners have been put off buy-to-let ownership by a proliferation of taxes and red tape.

Meanwhile, demand has dipped over the summer for reasons that include the lower number of Chinese students choosing to attend university in the UK, as we explored last month.

In Knight Frank’s updated forecast for the rental market, the company think the downwards trajectory for growth will continue until the end of the year, reaching 8% in both markets.

Bill added: “As the imbalance between supply and demand continues to reduce, we think rental value growth will return to more normal levels from 2024.

“We expect 5% growth in PCL next year and 4.5% in prime outer London, which are both still high by historical standards. The last time before the pandemic that rental growth ended the year higher than 5% in PCL or POL was in 2011.

“Supply is picking up more quickly in higher-value markets, as the graph shows.

“The number of instructions for lettings properties valued above £1,000 per week in London was 45% higher in September than January 2022. Meanwhile, below that figure, there was an 18% decline.

“Owners of higher-value properties are often more discretionary, and some have chosen to let them out until the trajectory of prices in the sales market becomes clearer.

“As a result, annual rental value growth in PCL above £1,500 per week was 9.6% in September compared to 12.4% below that figure.

“I think the market is at a pivotal point,” said David Mumby, head of prime central London lettings at Knight Frank. “Below £1,000 per week, demand is still ferociously strong but in higher-value markets the time taking to rent is elongating as stock increases. I think we’ll see the rate of growth for prime stock come down further.”

Comments are closed.