Modest house price inflation, combined with strong wage growth, means buying a home is becoming more affordable relative to income, according to new research from Halifax.

The analysis – based on data from the Halifax House Price Index – compared typical house prices to average earnings across the UK.

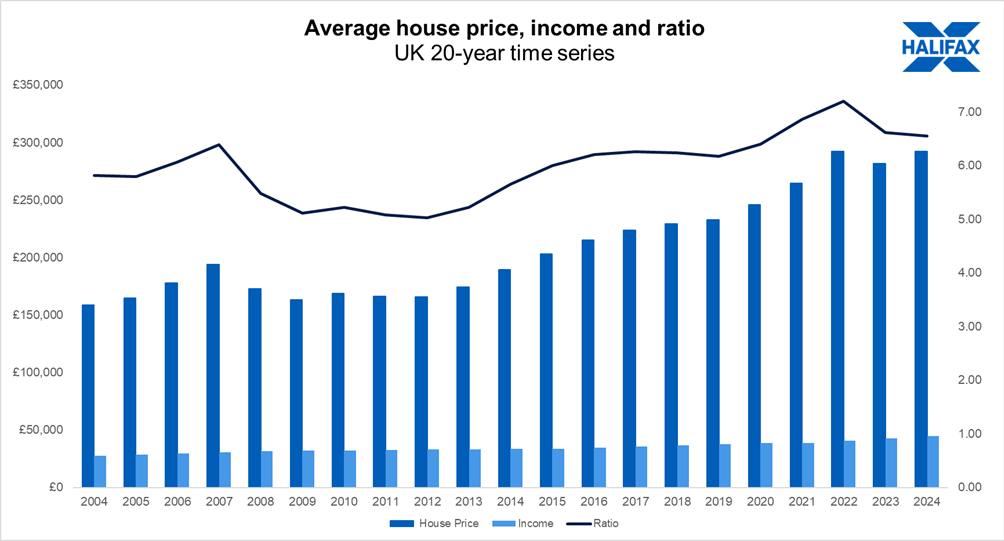

House prices have increased by +3.8% compared to a year ago, reaching an average of £292,508. Meanwhile, annual earnings for full-time workers climbed by +5% to an average of £44,667, over the same period.

This means wage growth outpaced house price inflation, putting the house price to income ratio at 6.55.

This is down from 6.62 last year, with the house price to earnings ratio gradually reducing since it reached a record high of 7.24 in the summer of 2022.

While market activity has been improving – the number of new mortgages agreed recently reached its highest level in two years – residential property purchases are down by around a third (-33%) compared to 2021, when interest rates were at a record low of 1.3% on average, compared to 4.1% in September this year.

A reduction in demand from buyers, from the highs of 2021, is one of the reasons house prices have remained flat for much of the last two years, with the average house price of £292,410 in 2022 compared to £292,508 in 2024.

Typical monthly new mortgage costs have fallen by about 9% over the last year, from £1,116 to £1,060. That’s based on the typical monthly cost of a five-year fixed rate mortgage, with a 30-year term and a 25% deposit (average interest rates of 5.2% and 4.1% respectively). Based on the average UK full-time income, that equates to mortgage costs as a percentage of income falling from 33% to 29%, its lowest level in over two years.

On the same basis, mortgage costs have fallen in each nation and region of the UK over the last year.

Amanda Bryden, head of Halifax Mortgages, said: “Housing affordability has improved over the past year, thanks to stabilising property prices, strong wage growth, and easing interest rates. That’s great news for first-time buyers and existing homeowners looking to remortgage or move up the property ladder.

“However, while homes are becoming more affordable, the progress has been gradual. Buying a property remains a significant challenge for many, with prices still near record highs and interest rates likely to stay higher than we’ve been used to over the past decade.”

| Mortgage costs as a % of income

Based on a 5-year fix, 25% deposit, 30-year term, average interest rates |

|||||

| Region | Mortgage cost Q3 2023 | Mortgage cost Q3 2024 | % change in cost | Cost as % of income Q3 2023 | Cost as % of income Q3 2024 |

| Eastern England | £1,347 | £1,207 | -10% | 40.1% | 34.6% |

| East Midlands | £971 | £877 | -10% | 30.7% | 26.0% |

| Greater London | £2,174 | £1,954 | -10% | 42.1% | 35.7% |

| Northern Ireland | £768 | £738 | -4% | 24.2% | 22.1% |

| North East | £692 | £621 | -10% | 22.6% | 19.0% |

| North West | £922 | £849 | -8% | 29.4% | 26.2% |

| Scotland | £834 | £746 | -11% | 25.4% | 22.1% |

| South East | £1,559 | £1,405 | -10% | 44.5% | 39.0% |

| South West | £1,217 | £1,101 | -10% | 38.0% | 32.7% |

| Wales | £888 | £812 | -9% | 28.8% | 24.5% |

| West Midlands | £1,021 | £925 | -9% | 30.1% | 24.8% |

| Yorkshire & Humber | £833 | £761 | -9% | 26.8% | 23.6% |

| United Kingdom | £1,166 | £1,060 | -9% | 32.9% | 28.5% |

At a local level, the North of England accounts for many of the most affordable areas.

Kingston upon Hull in East Yorkshire is crowned the most affordable area of the UK, with a house price to earnings ratio of 3.15. This is followed by Burnley and Blackpool in the North West, with ratios of 3.20 and 3.34 respectively.

Elmbridge in Surrey is the least affordable local area by some distance, with a house price to earnings ratio of 17.54. St Albans in Hertfordshire is in second place with a ratio of 13.96, followed by Kensington and Chelsea in London at 13.93.

However Elmbridge also saw the biggest improvement in affordability, falling from 19.46 in 2023. The biggest deterioration in affordability was recorded in Oxford in the South East, rising from 8.37 to 10.26.

Bryden said: “While national house price figures often grab the headlines, it’s crucial to remember that the property market varies significantly at a local level. The most sought-after areas tend to have the highest prices, and local developments, such as improved transport links or job opportunities, can all help to drive demand.

Is this data taken before Halifax put all their mortgage rates up?

You must be logged in to like or dislike this comments.

Click to login

Don't have an account? Click here to register