High mortgage rates are leading to a surge in cash purchases of buy-to-let properties in Great Britain, according to data from Hamptons.

High mortgage rates are leading to a surge in cash purchases of buy-to-let properties in Great Britain, according to data from Hamptons.

The shift towards cash purchases is particularly pronounced in Southern areas of the country, where yields tend to be lower. So far this year, 61% of investor purchases in the four Southern regions (London, South East, South West and East of England) were made in cash, up from 47% in 2022.

In contrast, cash purchases have fallen year-on-year in the North of England, from 62% in 2022 to 60% in 2023.

Higher interest rates are making it harder for buy-to-let sums to stack up, particularly in low-yielding areas of the country that generate smaller rental returns. This means that more investors are turning to cash to fund their purchases, as they may find it difficult to pass a lender’s stress test.

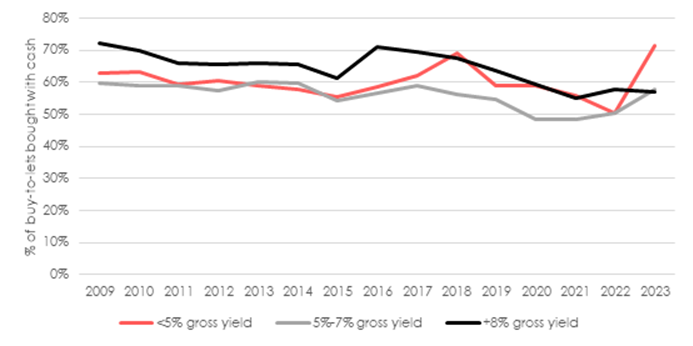

The average landlord who bought a buy-to-let in the South of England during the last 12 months achieved a 5.4% gross yield, lower than some mortgage rates, compared to 7.5% for those who bought in the North.

In London, which has the lowest yields in the country, the share of buy-to-lets bought with cash has risen to a record 67% so far this year, up from 43% in 2022. However, the average budget for investors has shrunk, with the average investor spending £341,000 on their new buy-to-let in the capital this year, down from £450,000 in 2022.

Hamptons estimates that this shift towards cash ownership will save new landlords across Great Britain around £61.9m in mortgage interest payments this year. However, it’s likely that new investors using a mortgage will pay around £405m in mortgage interest payments in 2023 if they were to buy using a 75% loan-to-value mortgage at an average rate of 5.27%. This is up from £347m in 2022 when mortgage rates were lower and there were more new buy-to-let purchases.

Aneisha Beveridge, head of research at Hamptons, commented: “The recent rise in cash purchases brings a close to landlords’ ability to access competitive mortgage deals. Sub 2% mortgage rates – available over the last few years – meant landlords who were able to buy homes outright chose instead to make the most of record low rates.

“Many investors spread their cash as far as it could go by topping it up with low borrowing costs to maximise their returns. However, today, investors are having to dig deeper into their savings to ensure the sums stack up on any new buy-to-lets.”

Comments are closed.