JLL has issued its latest report revealing that 2022 was a record-breaking year for prime central London (PCL), with buyers spending almost £5.2bn on homes, 9% higher than in 2021, already a strong year, and the highest amount spent for more than ten years.

JLL has issued its latest report revealing that 2022 was a record-breaking year for prime central London (PCL), with buyers spending almost £5.2bn on homes, 9% higher than in 2021, already a strong year, and the highest amount spent for more than ten years.

The amount spent on homes sold for £10m or more rose 16% on 2021 and was 81% higher than the total spend in 2019.

The research also shows that the number of properties on the market at the end of Q4 2022 fell this quarter, in line with usual seasonal activity. At the end of Q4 2022 there were 2,847 homes on the market in PCL, 3% higher than the same point a year ago and down 9% compared to the end of Q3.

Overall, the JLL prime central London index recorded a 3.5% quarterly fall in Q4 2022, with prices ending 2.4% lower than in Q4 2021.

Marcus Dixon, director of UK residential research at JLL, said: “Prime central London has not been immune to political and economic uncertainty that has overshadowed the UK market in recent months. On one hand there is less reliance on debt in the prime market than in mainstream, meaning fluctuations in interest rates have less of an impact, however increased uncertainty, and a higher proportion of discretionary purchasers in PCL have resulted in prices falling back in Q4.”

As far as the rental market is concerned, figures from the 2021 Census show the prime boroughs of Kensington & Chelsea and City of Westminster proportionally have some of the highest volumes of privately rented homes in the country. With more than 40% of homes privately rented meaning it remains the dominant tenure in PCL.

Despite a high proportion of privately rented homes demand continued to outstrip supply in 2022. Rental stock levels across prime central London remain below historic levels, as more tenants renew, and fewer new rental properties reach the market.

The number of properties available to let at the end of Q4 2022 was 13% higher than at the same point in 2021, when stock levels bottomed out, but remain 45% lower than in 2019.

Rents are higher than they were a year ago. The JLL prime central London Index recorded a 6.1% annual increase in achieved rents in the fourth quarter. Meanwhile rents achieved in Q4 2022 were 8.2% higher than they were pre-pandemic in Q1 2020.

Marcus Dixon, director of UK residential research at JLL, said: “Rental values continue to increase across all price brackets, although rates of growth are falling back. The highest growth is still being recorded for properties commanding lower average rental values. Properties let at under £1,000 per week have seen rents rise by 8.1% annually while those with rental values over £3,000 per week increased by a more modest 2.2%.”

Market outlook

Political and economic uncertainty, exacerbated by the September ‘mini-budget’, impacted both the prime and mainstream markets in the fourth quarter. According to the Nationwide Index, nationally prices fell for the fourth consecutive month in December. Now 2.5% lower than they were in August.

Economically there has been much to contend with in recent months. Inflation remains far higher than the Bank of England’s 2% target, meaning the base rate rose eight times last year, ending 2022 at 3.5%.

Yet there are reasons to be optimistic. The latest inflation figures suggest that annual increases may have peaked, in line with forecast, and look set to fall back in 2023. Fixed rates have also become more competitive, suggesting base rate rises over and above those we have experienced to date had already been priced in.

For overseas buyers exchanges rates are not quite as attractive as they were in September, when Sterling and the US dollar reached near parity at a 37-year low. But for those buying homes in US dollars there are still significant savings to be made. With prices in Q4 2022 12.8% lower than they were a year ago in US dollars and 35.9% lower than at the peak in 2014.

Despite the JLL prime central London Index recording falls in Q4, we still expect the underlying fundamentals of the prime market will stand it in good stead over 2023. With high levels of equity and cash purchase alongside sustained levels of domestic and international demand.

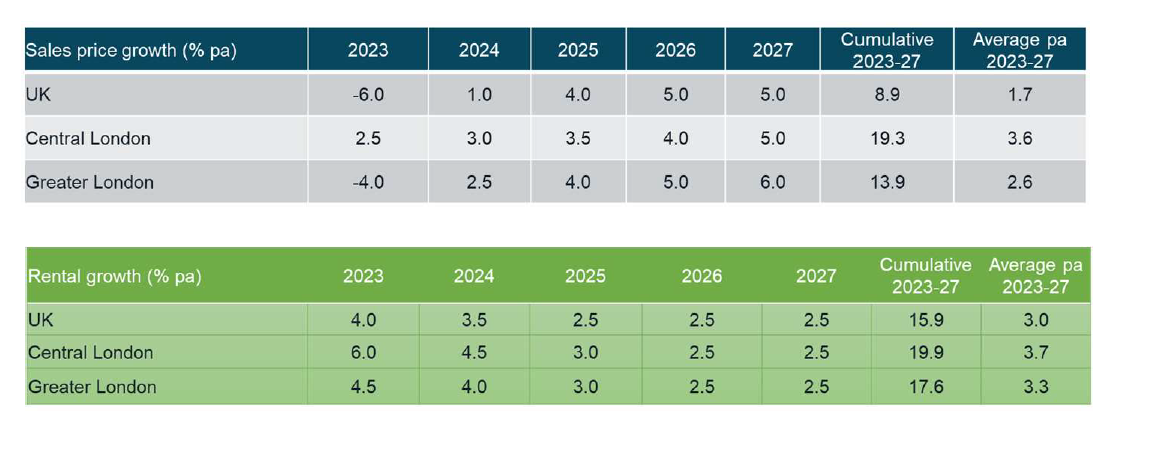

JLL expect central London will be our best performing market in 2023. Forecasting prices will rise 2.5% in 2023, with values 19% higher by 2027. Rents are expected to perform strongly too, underpinned by sustained stock constraints, with a 6% increase forecast in 2023 and growth of almost 20% by the end of 2027.

JLL residential market forecasts

Comments are closed.